Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Try using real returns. And play around with different timelines. I wouldn't bank on a real return of >5% for the next 40 years at this point.

I simply responded to what you posted here:

Quote:

If someone squirreled away 10% of their income into the stock market for 40 years, they could expect to have 10-15 years of that income saved up at the end.

What you described above is a simple accumulation problem, properly addressed by nominal, not real returns. And the nominal return for the S&P 500 from 1/1/1977 - 12/31/2017 is 12.64% (including dividends, which is appropriate give the simple accumulation problem that you described).

I agree that using real returns completely changes the analysis, but that isn’t what you originally described, nor what I responded to.

Real returns are inflation adjusted .but even nominal returns you are so wrong .

From 1977 to dec 2017 real returns were 7.48% and nominal were 8.78.including dividends.

Um, no. Go back to money chimp and run it again. Your 8.78 number is inflation adjusted, which as I explained earlier, is not appropriate for the situation described by ruff.

Quote:

I have no idea where you are getting 12% but it is quite wrong even for nominal returns .

I think it was more a shot from the hip as to what you thought rather than facts.

you can verify it on the money chimp s&p calculator which is spot on

Shot from the hip? Not hardly. You can check it for yourself and report back. I’m spot on.

What you described above is a simple accumulation problem, properly addressed by nominal, not real returns. And the nominal return for the S&P 500 from 1/1/1977 - 12/31/2017 is 12.64% (including dividends, which is appropriate give the simple accumulation problem that you described).

I agree that using real returns completely changes the analysis, but that isn’t what you originally described, nor what I responded to.

What?!

Real returns are the only thing that makes sense. If you assume a constant real wage, and you save x%, and get y% real returns for z years the analysis is easy.

Still waiting for you to supply your alternative analysis.....

Real returns are the only thing that makes sense. If you assume a constant real wage, and you save x%, and get y% real returns for z years the analysis is easy.

Still waiting for you to supply your alternative analysis.....

Not sure why you’re confused. This is what you said:

Quote:

If someone squirreled away 10% of their income into the stock market for 40 years, they could expect to have 10-15 years of that income saved up at the end.

That has NOTHING to do with real returns, just nominal. Accumulating the “10-15 years of that income” has nothing to do with the effects of inflation.

Accumulating the “10-15 years of that income” has nothing to do with the effects of inflation.

The point is, that we're implicitly assuming that one's income is constant throughout the accumulation-period, and that costs (or in other words, what that income buys) are likewise constant. Otherwise we submerge ourselves into a debate about the ravages of inflation, the stagnation of income and so forth... all interesting and important points, but peripheral to the discussion.

I go further to assume that returns are after-tax (or tax-free), to equalize the comparison between a poorer person struggling to save, but presumably paying lower taxes, and a wealthier person with plenty of discretionary income, but much higher tax-rates. Besides, when we hear about tax-favored savings-vehicles such as 401K's, we often disregard, that all funds in those accounts will eventually be taxed as income (instead of as long-term capital gains); so, the true returns of relevance, are after-inflation and after-tax. But by the same token, when we calculate ratio of portfolio to annual income, the latter should be after-tax.

To return to the theme of this thread: I, evidently unlike most others, am surprised that stock-ownership in America is so broad. I am surprised because I would have surmised that most people wouldn't bother, and would instead consume nearly the totality of their income, perhaps staying out debt, but saving next to nothing. Instead, people do save, and when they save, they do bother to invest, and when they invest, they do manage to include stocks/mutual-funds as part of their investments. So it's not all doom-and-gloom.

The point is, that we're implicitly assuming that one's income is constant throughout the accumulation-period, and that costs (or in other words, what that income buys) are likewise constant. Otherwise we submerge ourselves into a debate about the ravages of inflation, the stagnation of income and so forth... all interesting and important points, but peripheral to the discussion.

<<SNIP>>

All well and good. However, I won't presume to know what rruff meant in his post that I responded to, I simply responded to what he wrote. If he meant to say something different, he should have used different words.

In a discussion about finance, accuracy is important. Taking a post as written is reasonable. Expecting readers to assume that a poster in fact meant something different than what they actually posted is unreasonable.

If someone squirreled away 10% of their income into the stock market for 40 years, they could expect to have 10-15 years of that income saved up at the end. Not exactly "rich". If you saved 25% of your gross you'd have 25-35 years of that income, which is starting to look like a good retirement. But it's also a hefty cost to delayed gratification. Especially for the 50% of the population who's been experiencing declining real incomes and is already near the poverty line.

I agree that putting 25% of gross into stocks is a serious cramp on lifestyle, but it is certainly possible for many people to put 25%+ of gross income into appreciating assets. Maybe 15% into equities for retirement, 10% into the principle of a house, and 5% into a savings account that is used to make improvements on the house every 5-10 years. Many middle class people (such as my parents and their many siblings) followed an approach similar to this and now as they are approaching retirement they have a high 6 to low 7 figure retirement account, a paid off house that is worth a significant multiple of what they paid for it, significant social security benefits, and enough cash cushion to live for several years. They will not be buying mansions or Bentleys or anything, but they can afford to take trips, eat out frequently, pay cash for vehicles or home repairs, and spoil their grandchildren.

That has NOTHING to do with real returns, just nominal. Accumulating the “10-15 years of that income” has nothing to do with the effects of inflation.

Of course it does. Your real salary is worth x$ and your real savings is a worth 10-15x$.

You pretty much always have to work with real numbers if you want them to make sense.

As an example, say I put 10k into the stock market (one time) and got a nominal return of 10% for 40 years, so it's $450k then. How much is it actually worth in today's money?

If inflation is zero it's worth $450k. If inflation is 10%, it's worth $10k. If inflation is 15% it's worth $1.7k. Big range.

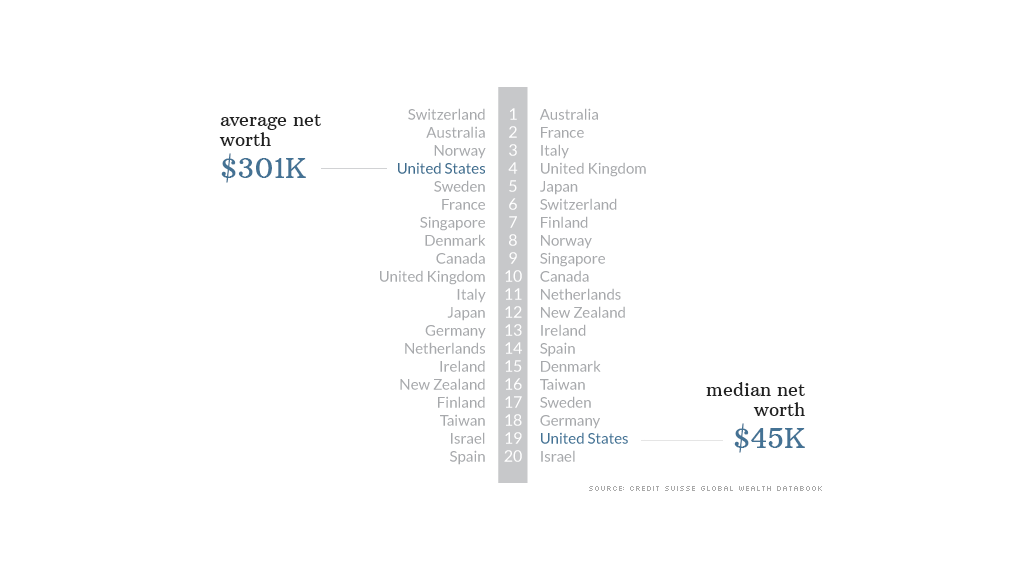

is this stat even valid? This seems ridiculously skewed to me. I thought 50% of Americans owned some stocks and the average balance was about $100k

No way 1 out of 2 own stocks. Plus the average can mean some own $100 million in stocks and some own $100, but I doubt the average investor even owns even $25K in stocks.

Instead, people do save, and when they save, they do bother to invest, and when they invest, they do manage to include stocks/mutual-funds as part of their investments. So it's not all doom-and-gloom.

I think you got the wrong impression:

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.