Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

The basic answer is YES - and this is our lack of a Universal Health Care system.

Yeah, that's a simple answer...but, bottom line, if we completely reformed health care this country would see economic (or happiness) growth we can only imagine. But we won't because money is more important than human beings here.

That's a great speech but almost certainly untrue. Virtually all countries with socialized medicine have proportionally smaller and generally lower performing economies than The US.

That's a great speech but almost certainly untrue. Virtually all countries with socialized medicine have proportionally smaller and generally lower performing economies than The US.

And that's because the more you subsidize people's lives, the less hard they are going to work on average. The less people work hard, the lower functioning the economy is.

Catastrophe sells. plain and simple. if I left it to suzy orman and the other guy I would never retire because health care cost will wipe me out, inflation will wipe me out, the next recession is going to have us all jump off of the ledge of our buildings.

So I am having a hard time understanding/processing all of the information we read out there relating to salaries, house prices, student loan debt, food costs, transportation, etc. Is almost everyone living on a financial edge? If you simply take the median household income of $61k, how are people paying for housing wherein the median price in the U.S. is around $300k? Hell, even if that median household income was $80k its still not enough!

After you had your mortgage, and some basic living expenses like food and gas for your car there is not much left over. How are you then paying student load debt, spending on other consumer products (e.g., consumer spending is at all-time highs), paying your car note (the car debt is at an all time high as well - over a trillion dollars), where the average car transaction sale is around $30k per KBB. Ohh and dont forget to save for retirement as well.

Curious to hear what other people think. I know the numbers above are not perfect, however, I would say they are accurate enough for this discussion.

Based on books like Jean Chatzky's The Difference, which was written in late 2008, early 2009, about 69% of the populace is living payday to payday or going further in debt. As she noted in the book, a pretty large minority of high earners also live on the financial edge. She called them "high income paycheck to paychecks". I don't think the statistics have changed much since that time.

So I am having a hard time understanding/processing all of the information we read out there relating to salaries, house prices, student loan debt, food costs, transportation, etc. Is almost everyone living on a financial edge? If you simply take the median household income of $61k, how are people paying for housing wherein the median price in the U.S. is around $300k? Hell, even if that median household income was $80k its still not enough!

After you had your mortgage, and some basic living expenses like food and gas for your car there is not much left over. How are you then paying student load debt, spending on other consumer products (e.g., consumer spending is at all-time highs), paying your car note (the car debt is at an all time high as well - over a trillion dollars), where the average car transaction sale is around $30k per KBB. Ohh and dont forget to save for retirement as well.

Curious to hear what other people think. I know the numbers above are not perfect, however, I would say they are accurate enough for this discussion.

Many of those people bought their home decades ago. If they've moved, they've had equity as part of the deal, so they're not taking a $300k mortgage, or even a $240k mortgage + down payment. That would never work on $60k.

These ratios can still be indicators of a city's accessibility to new entrants (from lower COL areas). San Francisco has 1:10 income:home value, while some Atlanta metro cities are closer to 1:2. Needless to say, I'd much rather live in ATL on $90k than SFO on $150k. Because in the latter example, it's no different than making $10/hour wondering how you're going to afford a $200k house.

... about 69% of the populace is living payday to payday or going further in debt.

... a pretty large minority of high earners also live on the financial edge.

And the largest common denominator among the various divisions of that 69%

is paying far too much of their income on their housing expenses (rent or buy).

As shown earlier in the thread... the old 3:1 (or less) ratio has been allowed to increase

and both incomes have become required to still pay too much of their total.

This has all occurred at the same time that first and second income gaps have eroded:

Ward and June are putting in far more hours than ever and getting less for them than ever.

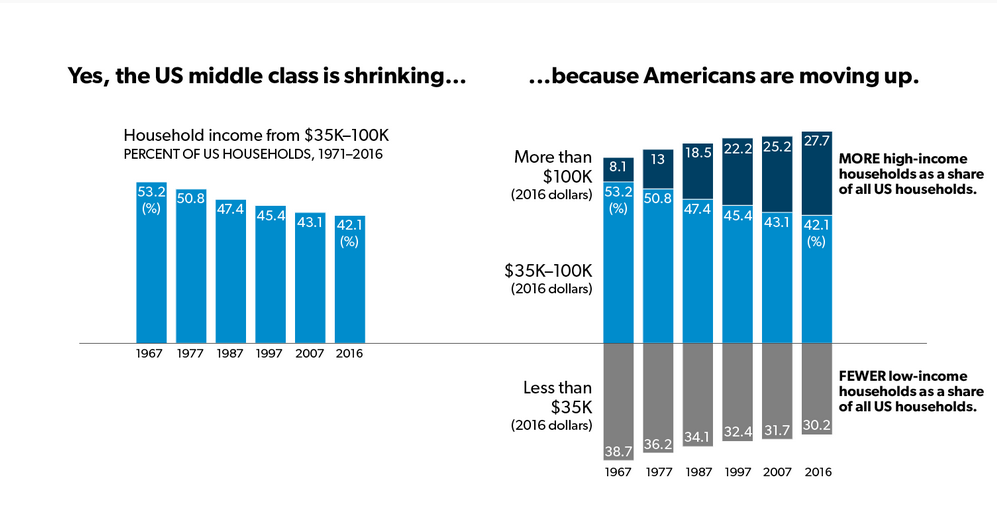

Still, the economy is in great shape and people are doing very, very well. One thing people focus on is the shrinking middle class -- indeed, the middle class IS shrinking, and for the best of all possible reasons:

And the largest common denominator among the various divisions of that 69%

is paying far too much of their income on their housing expenses (rent or buy).

As shown earlier in the thread... the old 3:1 (or less) ratio has been allowed to increase

and both incomes have become required to still pay too much of their total.

This has all occurred at the same time that first and second income gaps have eroded:

Ward and June are putting in far more hours than ever and getting less for them than ever.

I don't know too many mortgage companies or property management companies that would settle for any lower than 3:1 when approving an applicant. I think the issue is that there is an event where OTHER expenses rise, or income drops. (Funny how they don't just let you sign your house over if you no longer "qualify" for your PITI amount 2-3 years into your mortgage, at least not without all sorts of disaster on your credit report).

I don't know too many mortgage companies or property management companies

that would settle for any lower than 3:1 when approving an applicant.

1) Do not confuse what a LL or broker will sign you up for with anything in your best interest.

2) That's still not the question. 3:1 is about the income to price ratios (data posted twice in this thread already)

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.