Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Right. I wasn't suggesting that prices would reach 30 cents on the dollar uniformly throughout the counry. I do anticipate with the 12K houses available in the triangle, however, that 60-80 cents on the dollar (compred to today's "comps") is probably in the cards. It'll take time for the latent effect of dwindled transplant "equity refugee" money to dry up. Coupled with increasing interest rates and higher utility bills and a reduction in RTP workforce as a latent effect on the shrinking of the finance and services sector, just about everyone will be downsizing. So, what I'm thinking is that 60 cents on the dollar for the Holly Springs/F-V/Cary/NW Raleigh McMansions as well as overpriced Glenwood South/ITB inventory and the depressed SE Raleigh/Clayton/Garner area, and 80 cents on the dollar for lower priced, high value homes in the N. Raleigh/Apex/Cary area. I'm picturing that you're up by Millbrook/Six Forks/Falls, around where I'm at. I would imagine you're in better shape than most.

I too am interested to see what happens in downtown raleigh once all these condo developments are completed by this fall. I know the cost of vertical construction is more than they typical SFH on a $/sq ft basis, but I am a little shocked at some of the prices. Only time will tell I guess.

I too am interested to see what happens in downtown raleigh once all these condo developments are completed by this fall. I know the cost of vertical construction is more than they typical SFH on a $/sq ft basis, but I am a little shocked at some of the prices. Only time will tell I guess.

I was by the Sheriff's office on Salisbury to apply for another handgun permit and noticed the condo project nearby. Do you know if they sold off many of the units? On Glenwood South they converted many to apartments due to lack of demand. At least, that's how I understood it.

When do you see bottom for Miami, Las Vegas, Phoenix?

How about nationally?

Any insights on Chicago?

I only care about price. Sales volume or inventory drives prices in my opinion.

Wish I had my crystal ball

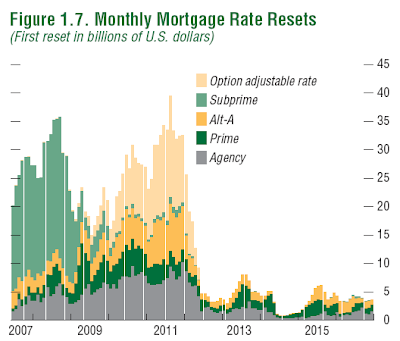

I was thinking it's going to take a while since the government seems hell bent on trying to keep nominal figures up. I'm more personally familiar with the carnage going on in FL than CA, Chicago, etc. If I HAD to throw a guess, I would think it'd take at least a year or two based on this chart. Keep in mind that it takes 6-9 months to get foreclosed on, in many cases. Things won't get better until 2012-2013 according to this either. This of course doesn't reflect double digit interest mortgage rates or the very real possibility of Fannie/Freddie going bankrupt.

Keep in mind that nominal figures might not drop a whole lot because the dollar is getting weaker over time. The one way you can truly price a house is to measure it in a commodity or a basket of commodities, like gold/oil/silver/soybeans/whatever. This drops the facade of inflation driving a bullish sentiment. It also shows that houses are in fact depreciating assets in many cases, meant to be enjoyed and lived in, not an investment.

The Federal Reserve can theoretically create so much inflation that nominal figures might actually rise, creating an illusion of wealth! BTW, that's also why I'm not big on shorting stocks but that's another matter.

Those swaths of foreclosures in Cleveland for instance are prime for a quick call of "eminent domain" and the government there FORCING the banks to take ANYTHING on the dollar from qualified owner occupiers.

Some regions have no issues. Others are at strong risk of severe urban blight unless the banks stop playing around and those homes are occupied again.

Those swaths of foreclosures in Cleveland for instance are prime for a quick call of "eminent domain" and the government there FORCING the banks to take ANYTHING on the dollar from qualified owner occupiers.

Some regions have no issues. Others are at strong risk of severe urban blight unless the banks stop playing around and those homes are occupied again.

The banks are also hoping for more government intervention to help make them whole. They don't want to take the 60% or whatever hit in their portfolio. They'd rather the taxpayer (aka renter and responsible homeowners) subsidize the cost.

Unlike the stock market, Mr. Troll and others like him can spin their pressure on government intervention as for the "greater community good", when in fact they could care less.

Current time to get a foreclosure filing in Dade/Broward County courts located in South Florida ? 9 months...JUST to get the filing. Time you get to live payment free ? Probably 13 months before they kick you out.

I read so much about the numbers are down...In my neighborhood 2 foreclosures have sold to young people who are fixing up the mess. But I saw the list of delinquet property tax payers and home owners with mortgage (lis pendens) issues, Hoa liens...so IMO there are many more homes coming on the market. My neighbors home was on the market for over 2 years..he had 2 on realtor.com, these 2 are off the list for quit some time but that is because the owner gave the keys to the mortgage company and walked away and they mrotgage comapny started the foreclosure procedure which takes longer than I expected....so the numbers can show off the market....but not sold, just waiting a couple of months to .....So if I take a look at my small neighborhood...1 bankrupt (still living in the home...?), at least 6 having lis pendens and/or Hoa liens and property taxes delinquet, and a couple with "only" Hoa liens". That is for 40 homes and ARM's have to be reset, soon...

Location: Upstate NY native, now living in Houston

663 posts, read 2,262,756 times

Reputation: 216

Quote:

Originally Posted by bentlebee

I read so much about the numbers are down...In my neighborhood 2 foreclosures have sold to young people who are fixing up the mess. But I saw the list of delinquet property tax payers and home owners with mortgage (lis pendens) issues, Hoa liens...so IMO there are many more homes coming on the market. My neighbors home was on the market for over 2 years..he had 2 on realtor.com, these 2 are off the list for quit some time but that is because the owner gave the keys to the mortgage company and walked away and they mrotgage comapny started the foreclosure procedure which takes longer than I expected....so the numbers can show off the market....but not sold, just waiting a couple of months to .....So if I take a look at my small neighborhood...1 bankrupt (still living in the home...?), at least 6 having lis pendens and/or Hoa liens and property taxes delinquet, and a couple with "only" Hoa liens". That is for 40 homes and ARM's have to be reset, soon...

All told, about 8.8 percent of home loans were past due or in foreclosure, or about 4.8 million loans.

Take out the 1 million or so in foreclosure, and you have 3.8 million past due. From stats I've seen, about half of past due loans get brought back up to date while the other half gets foreclosed on. That means that about 2 million of these loans are going to go bad, or twice the current level.

Quote:

Economists worry that a big loss of jobs in the coming months could drive default rates much higher.

The unemployment rate rose from 5.0 to 5.5 percent in May

Keep in mind that the troubles in housing so far have been against a backdrop of a relatively strong economy. There's lots more potential downside as employment and the economy in general gets weaker.

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

. But I saw the list of delinquet property tax payers and home owners with mortgage (lis pendens) issues, Hoa liens...so IMO there are many more homes coming on the market. My neighbors home was on the market for over 2 years..he had 2 on realtor.com, these 2 are off the list for quit some time but that is because the owner gave the keys to the mortgage company and walked away and they mrotgage comapny started the foreclosure procedure which takes longer than I expected....so the numbers can show off the market....but not sold, just waiting a couple of months to .....So if I take a look at my small neighborhood...1 bankrupt (still living in the home...?), at least 6 having lis pendens and/or Hoa liens and property taxes delinquet, and a couple with "only" Hoa liens". That is for 40 homes and ARM's have to be reset, soon...

. But I saw the list of delinquet property tax payers and home owners with mortgage (lis pendens) issues, Hoa liens...so IMO there are many more homes coming on the market. My neighbors home was on the market for over 2 years..he had 2 on realtor.com, these 2 are off the list for quit some time but that is because the owner gave the keys to the mortgage company and walked away and they mrotgage comapny started the foreclosure procedure which takes longer than I expected....so the numbers can show off the market....but not sold, just waiting a couple of months to .....So if I take a look at my small neighborhood...1 bankrupt (still living in the home...?), at least 6 having lis pendens and/or Hoa liens and property taxes delinquet, and a couple with "only" Hoa liens". That is for 40 homes and ARM's have to be reset, soon...