Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

If we assume you put nothing down and had to finance the full $500,000, which a lot of people did during this run-up, your mortgage and property taxes will cost you $42,924 per year. You need about $129,000 in gross income for that, at a minimum. Again, you would need to be in the top 10%-15% of wage earners, in the entire country, to be able to afford it.

Good reply, and no, I don't take it personally. I've bought and sold a few houses over the years, in Europe and the US, mostly in downturns.

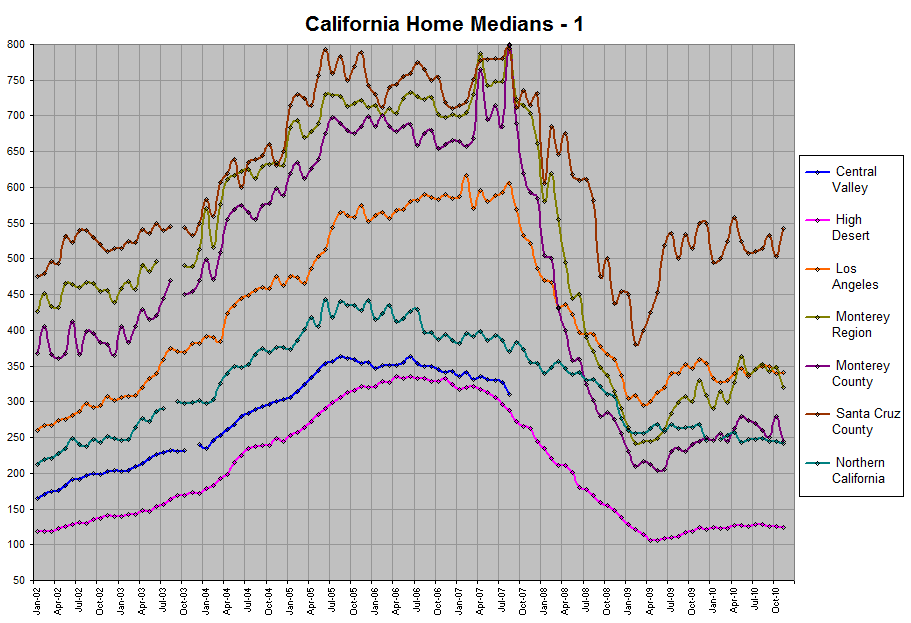

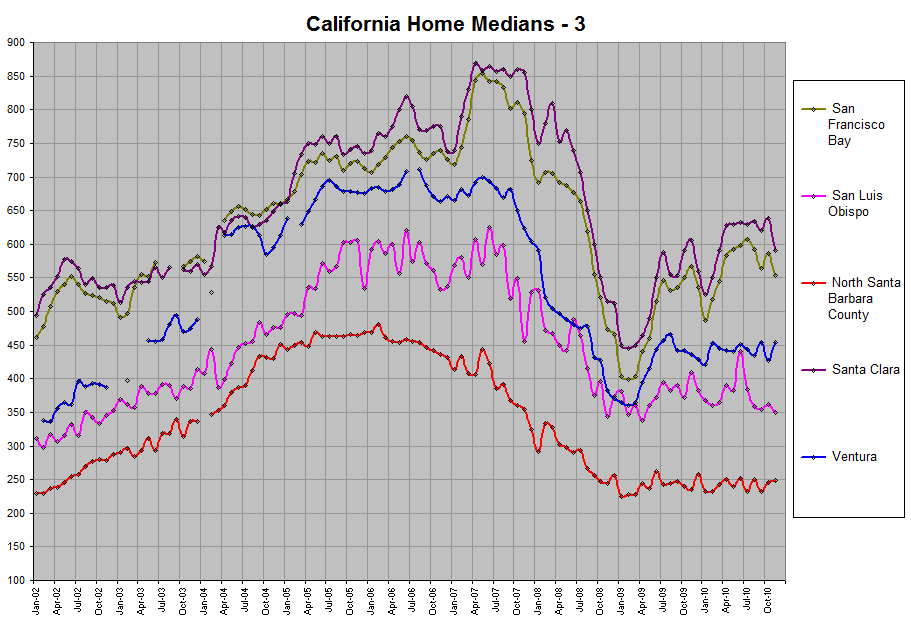

In the grand scheme of things, if you look at the nice areas in LA (Santa Monica, Malibu, Pacific Palisades, BHills, West LA/Mulholland/Sherman Oaks south of the blvd, etc), would you say this constitutes 10-15% of the available housing in the entire LA basin? If so, then there are enough people who are making good money in LA who can afford those prices - provided the credit crunch eases so that those with good credit can get a good deal. Banks are greedy: once they shake off the crud, they will go looking for people with good credit. The UK went through the "100% mortgage/no money down" crash in 1989 and a few years later they were back at it again.

Another thing you don't seem to be factoring in is that in the affluent areas ($1M+ homes), these are not first-time buyers. They have equity in existing homes and are trading up (or sometimes down if they are retired). And I'm always surprised how many people I run across who write me checks from "trust funds" and "foundations"... There is a lot of money in LA.

I totally agree that the crazy mortgages of the past few years is crippling many areas of the city, particularly with first time buyers. But I was responding to those folk who want to buy in Brentwood and Malibu and Westlake Village and so on, and may be expecting prices to fall 25%. My realtor friend tells me that those owners don't have subprime mortgages, and they just don't expect those areas to crash. (Just listen closely to Fred Sands telling realtors to move out of the valley and over the hill.) My friend says she has buyers ready to buy but they can't clear the hurdles that are being thrown up by the banks. So when you see that sales have fallen off a cliff, part of that is the credit crunch, which will ease as the banks realize they are missing out on good bets.

If you want to buy in a nice area, watch the economy (jobs and the credit crunch), not the home sales numbers for the entire LA basin. If LA goes go into a serious recession with high unemployment in high-paying jobs then the affluent areas will be affected. Maybe a long drawn out writer's strike will be the catalyst in LA, time will tell.

Another thing you don't seem to be factoring in is that in the affluent areas ($1M+ homes), these are not first-time buyers. They have equity in existing homes and are trading up (or sometimes down if they are retired). And I'm always surprised how many people I run across who write me checks from "trust funds" and "foundations"... There is a lot of money in LA.

There is a lot of money in LA indeed. Don't forget that there are cash buyers also. We will be paying all cash for our home. I know a few people that own several homes (multi million $$ homes) and probably most if not all are bought with cash (no mortgage)!

Wait until the housing market cools off alot more, then BUY!!! You would not be smart if you bought now. The real estate moochers dug their own pit, including my father even though I love him.

Wait until the housing market cools off alot more, then BUY!!! You would not be smart if you bought now.

We are hoping to be able to get back to CA by next year. So I hope it works out in our favor but like the link I provided with data shows, the market isn't really changing that much in the location I want to be in. We'll see.

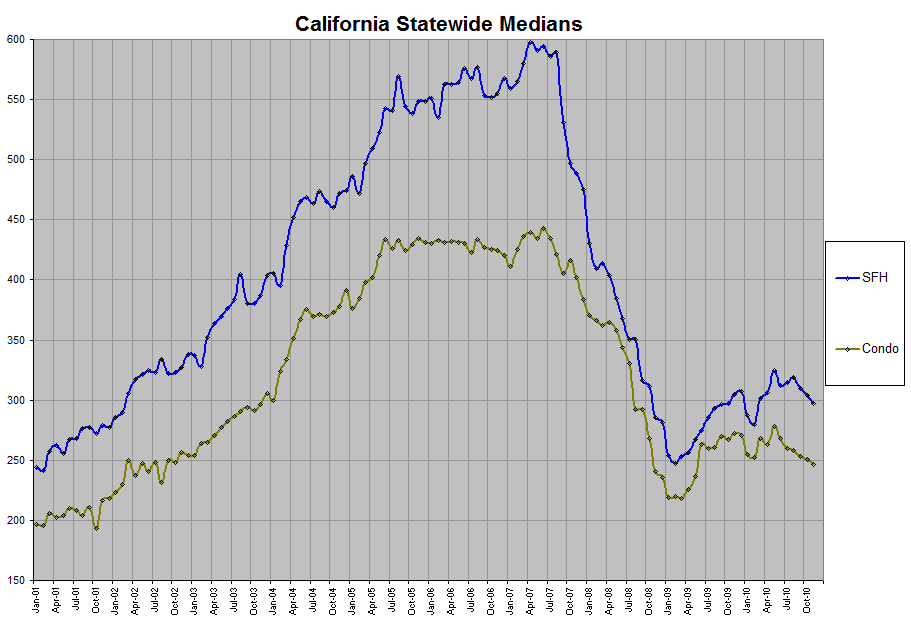

In California that number will eventually be even larger because the house prices are so significantly more inflated than average. .

This is the part I don't understand. The loan issues described in your big post pretty much affected the entire country. Therefore the same drivers apply to all regions' housing prices. So why did SoCal house prices rise so much higher than middle America? For example (and I am making up numbers) why did Houston prices go up say 30% or 40% from 2000 to 2005 and LA went up like 150% (again, I am just assuming these numbers..but they are probably good enough for illustration.)

Why did California prices inflate so much more than just about everywhere else? That's essentially my question.

This is the part I don't understand. The loan issues described in your big post pretty much affected the entire country. Therefore the same drivers apply to all regions' housing prices. So why did SoCal house prices rise so much higher than middle America? For example (and I am making up numbers) why did Houston prices go up say 30% or 40% from 2000 to 2005 and LA went up like 150% (again, I am just assuming these numbers..but they are probably good enough for illustration.)

Why did California prices inflate so much more than just about everywhere else? That's essentially my question.

Perceived market value? Marketing? Who knows...

I don't think the numbers are as exaggerated as the previous poster mentioned. If they were the LA market would be number 1 on the "places-set-to-go-boom" lists. Consider that other places have the same scenario that you mention. SEE: Previous links.

This is the part I don't understand. The loan issues described in your big post pretty much affected the entire country. Therefore the same drivers apply to all regions' housing prices. So why did SoCal house prices rise so much higher than middle America? For example (and I am making up numbers) why did Houston prices go up say 30% or 40% from 2000 to 2005 and LA went up like 150% (again, I am just assuming these numbers..but they are probably good enough for illustration.)

Why did California prices inflate so much more than just about everywhere else? That's essentially my question.

The only way prices can inflate so high is demand outpaced what was available so sellers could practically name their price a few years ago. I think a lot of this was investors buying up a ton of properties and of course, low interest rates and relaxed lending helped them as well first time home buyers who thought they better buy now while they can. If you ever watch any of those flip shows, the homes are largely located in Southern Cal.

The only way prices can inflate so high is demand outpaced what was available so sellers could practically name their price a few years ago. I think a lot of this was investors buying up a ton of properties and of course, low interest rates and relaxed lending helped them as well first time home buyers who thought they better buy now while they can. If you ever watch any of those flip shows, the homes are largely located in Southern Cal.

I understand what you wrote but it still doesn't explain why California appreciated so much more than most other places (unless you are trying to say that the "flipping" shows are the reason California's appreciation is excessive - but I don't think that is what you are saying...)

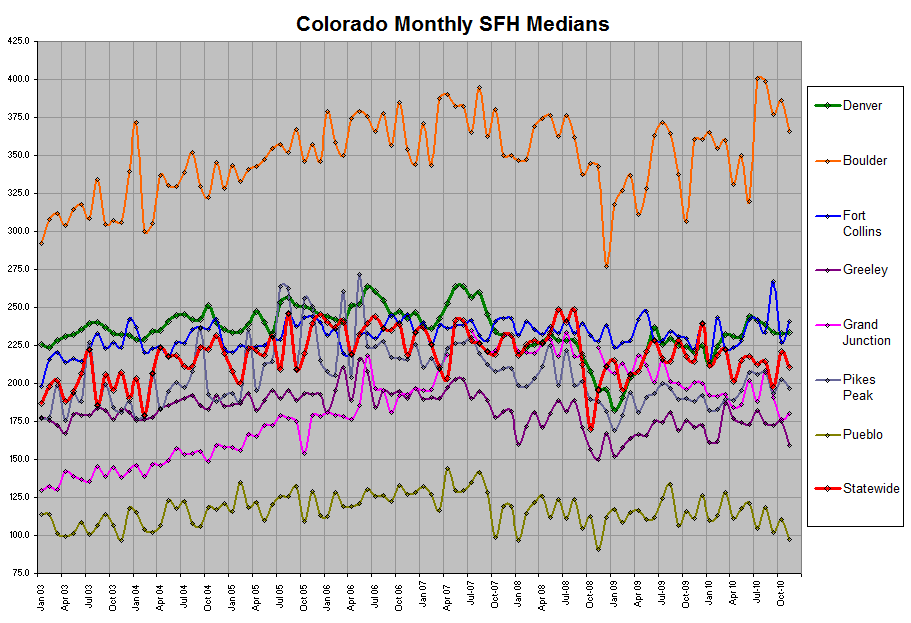

California has 36 mil people (not counting undocumented) while Colorado has less than 5 mil. You get 3-5% of this group looking to buy into a home, you can fuel a pretty good housing boom and a demand that outstrips supply. I think developers/investors bought up land and tried to capitalize (by manipulating supply) as much as possible and buyers unfortunately didn't comprehend that they set the prices so if they didn't pay for the homes at those high prices, they would come down just like we're seeing now with buyers delaying their purchase decisions. We all now know this dynamic was due to high consumer optimism, low interest rates, laxed lending standards (in some cases predatory lending), and aggressive marketing by NAR and brokers. Maybe more of these factors were evident in California than other states.

Good reply, and no, I don't take it personally. I've bought and sold a few houses over the years, in Europe and the US, mostly in downturns.

In the grand scheme of things, if you look at the nice areas in LA (Santa Monica, Malibu, Pacific Palisades, BHills, West LA/Mulholland/Sherman Oaks south of the blvd, etc), would you say this constitutes 10-15% of the available housing in the entire LA basin? If so, then there are enough people who are making good money in LA who can afford those prices - provided the credit crunch eases so that those with good credit can get a good deal. Banks are greedy: once they shake off the crud, they will go looking for people with good credit. The UK went through the "100% mortgage/no money down" crash in 1989 and a few years later they were back at it again.

Another thing you don't seem to be factoring in is that in the affluent areas ($1M+ homes), these are not first-time buyers. They have equity in existing homes and are trading up (or sometimes down if they are retired). And I'm always surprised how many people I run across who write me checks from "trust funds" and "foundations"... There is a lot of money in LA.

I totally agree that the crazy mortgages of the past few years is crippling many areas of the city, particularly with first time buyers. But I was responding to those folk who want to buy in Brentwood and Malibu and Westlake Village and so on, and may be expecting prices to fall 25%. My realtor friend tells me that those owners don't have subprime mortgages, and they just don't expect those areas to crash. (Just listen closely to Fred Sands telling realtors to move out of the valley and over the hill.) My friend says she has buyers ready to buy but they can't clear the hurdles that are being thrown up by the banks. So when you see that sales have fallen off a cliff, part of that is the credit crunch, which will ease as the banks realize they are missing out on good bets.

If you want to buy in a nice area, watch the economy (jobs and the credit crunch), not the home sales numbers for the entire LA basin. If LA goes go into a serious recession with high unemployment in high-paying jobs then the affluent areas will be affected. Maybe a long drawn out writer's strike will be the catalyst in LA, time will tell.

It is true that the wealthy areas may not be as greatly impacted as other areas because the people buying there are not as price sensitive. But rich people like a good deal and are looking for a good investment like the next person. To think they can and will forever pay up for a house is crazy think. Prices in those areas may not come down at the same time or the same rate as other areas, but they will come down at some point. Not everyone in Brentwood paid cash for their homes and are immune to market movements.

Yes, there are a lot of rich people in LA, but proportionately they are still a small percent of the population. As such, houses at those price points are also a small percent of the housing stock. Yes, it's still a big number, but you have to look at things relatively.

Also, going back to the 10%-15% of wage earners, you have to be in that range to buy the MEDIAN priced house in LA. Homes in Malibu, Brentwood, etc., are FAR above the median. Therefore buyers in those areas have incomes far above the median. You're talking in the top 5% of wage earners. The number of people making that kind of money gets slim real quick.

For example, the average mortgage size at my bank is about $1 million. The mortgage will run you about $76,000 per year. Then you have $10,000 in property taxes or more, etc. So you're at $86,000+ in housing costs. You'll need a minimum annual income of about $260,000 to cover that.

As of 2006, the Census Bureau says the average income of the top 5% in the country is $297,000. The bottom end of the top 5% is $174,000. So if you're making $260,000, you're well into the top 5%.

I can't find the number of households in the top 5%. It has to be out there somewhere. Although it may look like a big number, it's not large relatively speaking. Maybe we can back into it.

36 million people. Average household size of about 2.6 I think. That's 13.8 million households. The top 5% would be 690,000 households statewide that might fit into those income brackets. And then let's say there is a disproportionate number of people making that kind of money and round up to 1 million.

Anyone know what the housing stock is in California? If we have that we should be able to back into some numbers.

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.