Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Insurance is NOT an investment, and should not be though of as such. The purpose of life insurance is to, in case of your death, take care of costs and expenses that money can take care of in your absence, and that is the amount you should be insured for. That amount will change over the years, so buy term, which you can adjust from year to year. For example, when your kids are out of college, you no longer need to have that coverage, so why commit to it now with whole life?

Dear me...so you think Whole Life is a good or bad product? I'm so confused. Perhaps put down the studies and read the Policy fine print regarding all the fees, surrender charges, loss of cash value upon death, and all the other insurance nonsense packaged into these subpar products. Studies can print whatever they conclude to be correct. Just because it's written, doesn't make it so.

it is an excellent product if you need coverage until death. many folks do since their spouse may have a pension that does not carry over . my wifes pension is like that and does not pass to me , they may have a mortgage or they may just want guaranteed legacy money.

it i a lousy investment so it should not be bought for the refund amount (cash value). if you are not using it for dying don't buy it .

new research is showing that when used through retirement with an immediate annuity and your own portfolio success rates are higher , income is higher and there is a pretty good chance legacy money will be higher in all but the most favorable sequences and returns .

in short you need a reason for it other than as some sort of supposed investment .

Last edited by mathjak107; 08-18-2015 at 04:36 PM..

So knowing that the cash value will be surrendered upon death, why wouldn't you just take term life and invest all the extra money you'll have from not having to make hefty WL premium payments?

if you were not aware most small investors suck at it as the data at morningstar shows.

the majority of small investors do not even get the returns the funds they were in got as the tracking of money in and out shows .

many do not have the discipline to invest the difference , they don't have the pucker factor to stay the course and most have no interest in learning to invest.

while those active on forums enjoy it or make a hobby out of it few americans do that .

if they need coverage until the end they need guarantees they will have that money not subject to their investing skills, temperment and whims of mr market . .

as far as my policy , it was a pretty small policy and it serves an important use . it was payed up a long time ago and i have not made a payment in many many years . in fact my kids are the owner at this stage and it is out of our estate .

since this is a 2nd marriage my wife and i are leaving everything to each other so my policy is a little something ear marked just for my kids so they do not have to wait for a non parent to die to see anything .

that is a very good use for small permanent insurance policys. nothing comes out of the joint portfolio or takes money away from the surviving spouse , especially at a time when not only do they lose a social security check but their tax status becomes single too. in my case if my wife dies first i lose a 20k pension she gets . luckily i don't need it but if i did i would have used insurance to guarantee that income .

the policy is not in our estate which here in ny is a big consideration since with it we would be just over the limit for the state estate tax threshold.

if you go over by more than 5% you don't just pay the tax on the difference you pay the entire tax from dollar 1. it is a horrible tax cliff as they call it.

we have until next april to go to clear it when ny raises it again to 4 million .

Last edited by mathjak107; 08-18-2015 at 05:26 PM..

You are certainly correct to assume most people don't have the self-discipline to self invest. So maybe for them, they need a product that will make them save. I still wouldn't ever recommend WL but I'm glad it worked out for you.

you don't have to like it but you do have to open your eyes up to learning that there is a whole lot more going on out there that you do not understand or know about than you were brain washed in to thinking by other short sighted people who do not understand modern day research , numbers crunching and most important the second half of the game when it comes to spending down . .

few ' if any of those misinformed talking heads ever go beyond retirement age when comparing term and investing and they certainly never integrate with an SPIA income stream that can run 30-40% more than bonds and cash can safely provide . that is why i knew you would not find one accredited study , because before the research of PFAU , KITCES , BLANCHETT , BERNSTEIN AND MILEVSKY there was no one that actually went the extra mile to see results with an integrated strategy .

it is only when you fully understand both sides well that you can draw a conclusion of your own,

Last edited by mathjak107; 08-19-2015 at 03:33 AM..

whole life can actually be one of the cheapest ways to insure if you want or need coverage until death.

it is only lousy when you try to use it as a product for living such as cancelling it and taking the refund . then it becomes the most costly way of insuring over the time frame you did since you still paid towards the fact you will keep it until death even though you do get somewhat of a refund if you cancel it in the form of that cash value .

whole life is a very misunderstood product .

We're not all in the same boat and that is for sure.

I'm 67 and I have some health issues. At 67 who out there doesn't have at least one medical issue to deal with? Long story short I have Type 2 diabetes that is linked to my service in Vietnam and agent orange. The area I was in was the most heavily sprayed area and from what I have read I could end up with a host of other issues but time will tell.

When I had the chance to purchase the whole life without a premium hike I jumped at it because I doubt the opportunity will come around again.

As I said some of us have issues and some of us don't.

Know that I am married and if I wasn't I would immediately drop all life insurance like a hot rock and I fully recognize insurance, especially whole life, isn't just a terrible investment but no investment at all. What I am doing here is buying protection for the one I love. That's it, it makes me sleep better at night. That is it, that is the only reason I have any life insurance at all.

I have three life insurance policies with two of them term and one whole life which I purchased about a year ago.

Insurance #1 is a large term policy with relatively cheap premiums and the only problem with this is expires April, 2017.

Insurance #2 is a large term policy with somewhat higher premiums and the only problem with this is expires December, 2025. In three years I will most likely drop this policy because I will have worked to age 70 and my wife will be able to collect social security benefits in excess of $3,000/month.

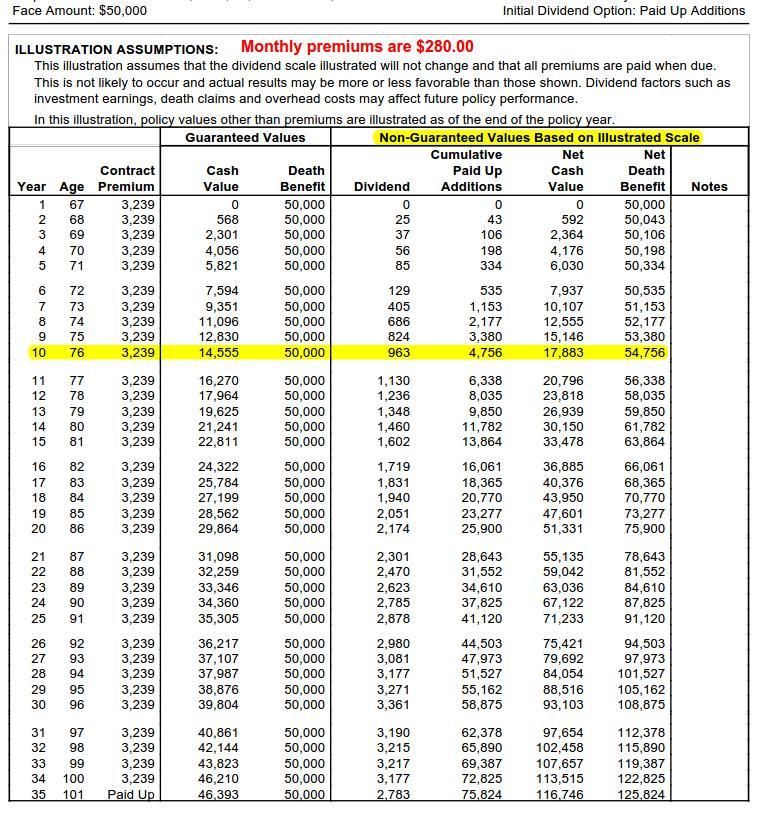

Here's what I have in the whole life

The way I approached the purchase was to recognize this is probably the last insurance I will ever be able to purchase.

As to the non-guaranteed values this company has been around for over 125 years and has never failed to pay the non-guaranteed value even during the great depression. For what it is worth A.M. Best gave the company a rating of A++ (Superior) for financial strength.

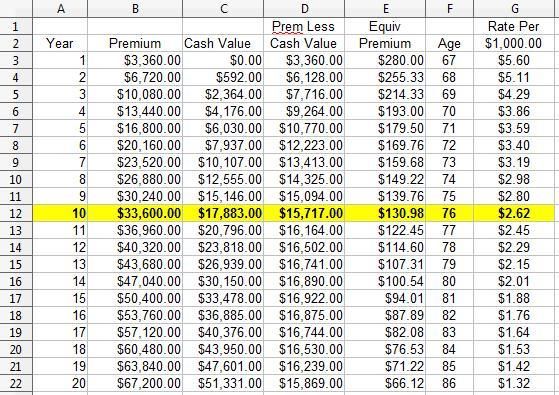

So I have these premiums going out every month and what I really wanted to see was what they were costing me so...

If something happens to my wife, in say 8 years. I'd immediately terminate the policy and collect the cash value of $12,555 which will reflect that I purchased life insurance for $2.62/$1,000 over the eight year period. At age 67 a rate of $2.62 is pretty cheap.

many times that need does not end just because you think the kids will be out or the mortgage paid .

it all depends how long and why you want coverage .

if it is to replace a spouse's pension you don't get it could be needed forever .

We're not all in the same boat and that is for sure.

I'm 67 and I have some health issues. At 67 who out there doesn't have at least one medical issue to deal with? Long story short I have Type 2 diabetes that is linked to my service in Vietnam and agent orange. The area I was in was the most heavily sprayed area and from what I have read I could end up with a host of other issues but time will tell.

When I had the chance to purchase the whole life without a premium hike I jumped at it because I doubt the opportunity will come around again.

As I said some of us have issues and some of us don't.

Know that I am married and if I wasn't I would immediately drop all life insurance like a hot rock and I fully recognize insurance, especially whole life, isn't just a terrible investment but no investment at all. What I am doing here is buying protection for the one I love. That's it, it makes me sleep better at night. That is it, that is the only reason I have any life insurance at all.

I have three life insurance policies with two of them term and one whole life which I purchased about a year ago.

Insurance #1 is a large term policy with relatively cheap premiums and the only problem with this is expires April, 2017.

Insurance #2 is a large term policy with somewhat higher premiums and the only problem with this is expires December, 2025. In three years I will most likely drop this policy because I will have worked to age 70 and my wife will be able to collect social security benefits in excess of $3,000/month.

Here's what I have in the whole life

The way I approached the purchase was to recognize this is probably the last insurance I will ever be able to purchase.

As to the non-guaranteed values this company has been around for over 125 years and has never failed to pay the non-guaranteed value even during the great depression. For what it is worth A.M. Best gave the company a rating of A++ (Superior) for financial strength.

So I have these premiums going out every month and what I really wanted to see was what they were costing me so...

If something happens to my wife, in say 8 years. I'd immediately terminate the policy and collect the cash value of $12,555 which will reflect that I purchased life insurance for $2.62/$1,000 over the eight year period. At age 67 a rate of $2.62 is pretty cheap.

Oh to be healthy and 30 again!

don't forget what they call a cash value is really an agreed upon refund like a gym membership you don't use .

that refund can be as little as they like . it isn't only premiums you pay in but all your interest and dividends too over decades . that can eventually cost you more than the premiums .

the whole idea s basically you end up being self insured by the time the policy endows and you paid in as much as you got less the fees ,commissions and expenses they took .

looking at what your premium is will be only part of the cost , the rest is the interest you reinvested back in to the policy which was your money too . .

whole life is not as cheap as the policy data shows when they only count premiums .

modern day policy's are priced pretty low considering unlike term where there is very few pay offs , whole life is based on a 100% pay off . the company covers you on their dime until you have enough to self insure and they get paid to do that.

the fact is most whole life policy's either get cancelled or folks take that reduced refund amount and so very few actually use it for what it is intended for which is 100% chance of pay off at death .

that can be a very costly way to insure if you are not going full term to death since you are paying for it . don't think for one moment that the cash value is acting as some sort of investment . it is not and in the scheme of things if that is why you are using the policy you got a poor deal . it is only when used for its intended purpose that you get maximum value out of what it cost

Last edited by mathjak107; 08-23-2015 at 03:37 AM..

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.