Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

The CRA forces banks to make loans in poor communities, loans that banks may otherwise reject as financially unsound. Under the CRA, banks must convince a set of bureaucracies that they are not engaging in discrimination, a charge that the act encourages any CRA-recognized community group to bring forward. Otherwise, any merger or expansion the banks attempt will likely be denied.*

Of course, lenders not only sold billions of dollars in suspect loans to Fannie Mae and Freddie Mac, contributing to their present debacle, they also retained some subprime loans themselves and sold others to Wall Street–leading to the huge banking losses we have been witnessing for months. Is this, then, a free market failure? Again, no.

* I didn't see it in this article but I've read lenders received lower interest rates from the Fed when they made more "CRA type" loans.

You are skirting the issue and my question. That law didn't FORCE financial institutions to offer little or no money down on mortgages. Those institutions could have required more collateral if they wanted to.

The whole notion that the powerful banking and financial industry was pushed around, when they have strong allies in Congress and armies of lobbyists, really does defy common sense.

Those mortgages were offered that way because the banks and financial industry were making huge profits selling those mortgages as AAA bond instruments.

You are skirting the issue and my question. That law didn't FORCE financial institutions to offer little or no money down on mortgages. Those institutions could have required more collateral if they wanted to.

READ MY POST BEFORE YOU COMMENT

Again The CRA forces banks to make loans in poor communities, loans that banks may otherwise reject as financially unsound. Under the CRA, banks must convince a set of bureaucracies that they are not engaging in discrimination, a charge that the act encourages any CRA-recognized community group to bring forward. Otherwise, any merger or expansion the banks attempt will likely be denied.*

Quote:

Originally Posted by MTAtech

The whole notion that the powerful banking and financial industry was pushed around, when they have strong allies in Congress and armies of lobbyists, really does defy common sense.

You don't have much common sense. You are skirting the issue and my question. Why did lenders lower standards?

Quote:

Originally Posted by MTAtech

Those mortgages were offered that way because the banks and financial industry were making huge profits selling those mortgages as AAA bond instruments.

You are skirting the issue and my question. Why did lenders lower standards?

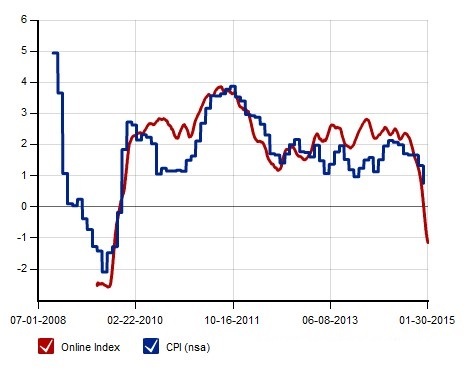

Yes, exactly like CPI. The Billion Price Index computes inflation completely differently than the CPI is calculated.

Yet, pretty much parallel.

So although CPI is a known fraud because BPI mirrors it means it has substance? LMAO What an idiotic thing to say. You can't even describe BPI and why it has merit. All because someone said so.

Compare income and the price of goods from the year 2000 to current levels for your answer on that definition of inflation.

READ MY POST BEFORE YOU COMMENT

Again The CRA forces banks to make loans in poor communities, loans that banks may otherwise reject as financially unsound. Under the CRA, banks must convince a set of bureaucracies that they are not engaging in discrimination, a charge that the act encourages any CRA-recognized community group to bring forward. Otherwise, any merger or expansion the banks attempt will likely be denied.*

You don't have much common sense. You are skirting the issue and my question. Why did lenders lower standards?

You are skirting the issue and my question. Why did lenders lower standards?

You read the book about how red lining wasn't nearly as big as reported?

Do you understand that the lowering of standards was lowered for EVERYONE? If it wasn't that would be discriminatory. It's not about CRA loans only, it's about loans that would have never been made if we had adhered to the normal standards.

And the answer to my question, Why did lenders lower standards?

Government told them to.

Cost of college may be rising because demand is rising.

There are more students attending college and we haven't been growing the number of good universities. Moreover, public colleges used to subsidize college tuition more than they do now.

Of course, none of this has anything to do with the fact that the UE rate is 5.1% and before you knee-jerk respond with the falling labor participation rate, I'll preempt it with this: Declining Labor Participation Rates

Sorry that excuse doesnt fly, if there is room for them in a college class room, then there is room and thus demand is sustainable.

I think its weird though that you do a 180 in regards to things like minimum wage, where government should determine it, despite the demand not rising.

Whats next, government limiting the rise in the cost of education?

from 2001 through 2006, the share of all mortgage originations that were made up of conventional mortgages (that is, the 30-year fixed-rate mortgage that had always been the mainstay of the U.S. mortgage market) fell from 57.1 percent in 2001 to 33.1 percent in the fourth quarter of 2006. Correspondingly, sub-prime loans (those made to borrowers with blemished credit) rose from 7.2 percent to 18.8 percent, and Alt-A loans (those made to speculative buyers or without the usual underwriting standards) rose from 2.5 percent to 13.9 percent.

The FACT is a much higher percentage of horrible loans were made under Bush.

In 2006 1 out of every 3 mortgages were 3 percent down or less. By then almost half, 45 percent, of all first time mortgages were no money down.

What was the percentage of the horrible little to no down payment loans came under Clinton?

Again I'm not blaming the president, I'm blaming Congress. I was pointing out the tipping point.

Don't bypass the free market in housing and we don't have a crash. Don't make those loans. Everything besides that isn't the cause. Treat the cause.

The no money down loans were coming from the "free market." Where was the money coming from to fund the no money down loans? From the selling of unregulated, nontransparent OTC derivatives. Congress had specifically excluded derivatives from being regulated in favor of a free market approach.

You read the book about how red lining wasn't nearly as big as reported?

Do you understand that the lowering of standards was lowered for EVERYONE? If it wasn't that would be discriminatory. It's not about CRA loans only, it's about loans that would have never been made if we had adhered to the normal standards.

And the answer to my question, Why did lenders lower standards?

Government told them to.

Nope. Nope and Nope. There are many, many ways that financial institutions can comply with the CRA. This can be investments within the communities where they are doing business; purchasing federal tax credits to finance housing; financial education in communities; and simply showing that they offer loans to people that meet the minimum standards. Any bank that offered subprime loans to people despite their creditworthiness did so on their own volition.

But hey, why blame the mess on greed and avarice when you can blame poor people!

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.