Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

You are absolutely correct. It is absurd what is going on today but people like low rates because they can borrow more ... and more, and more, and more. Yep. Nothing like borrowing to make a great economy and strong country. Just look at Europe and Japan. But silliness reigns because it benefits the top 1% and the borrowers get some temporary high like they did during the housing bubble. And then things collapse and everyone looks around and wonders what happens and wants the government (the savers) to bail them out yet again. Only savings are vanishing, poverty is growing, jobs are dwindling, costs are going up and people all over who are being hurt the most are getting angrier and angrier with unknown potential consequences.

Let's just take one small part of your ideology, the bolded part "jobs are dwindling". Actually jobs are increasing, albeit with frustrating slowness. See the link below for an article from today's Los Angeles Times:

Let's just take one small part of your ideology, the bolded part "jobs are dwindling". Actually jobs are increasing, albeit with frustrating slowness. See the link below for an article from today's Los Angeles Times:

"A lot of the increase in inequality from 2010 to 2011 is driven by changes at the very top of the distribution," said David Johnson, chief of Census' social, economic, and housing statistics division.

The second and third quintile of Americans now take home only 23.8% of the nation's income, the lowest since the Johnson administration, said Tim Smeeding, the director for the Institute for Research on Poverty at the University of Wisconsin-Madison.

"The big story is the squeeze in the middle- and lower-middle classes," he said. "They got whacked." Some groups were hit harder than others. Those ages 35 to 44 and 55 to 64 had a drop in income, as did white and black Americans. Households in the West experienced a 4.1% decline in income.

Overall, median income has fallen 8.9% from its peak in 1999. And it's fallen 8.1% since 2007, just before the Great Recession began.

Since the recession, incomes continued to fall, declining 4.1%. Though incomes dipped after the two preceding downturns, this drop is far worse, said Rakesh Kochhar, associate director for research, Pew Hispanic Center.

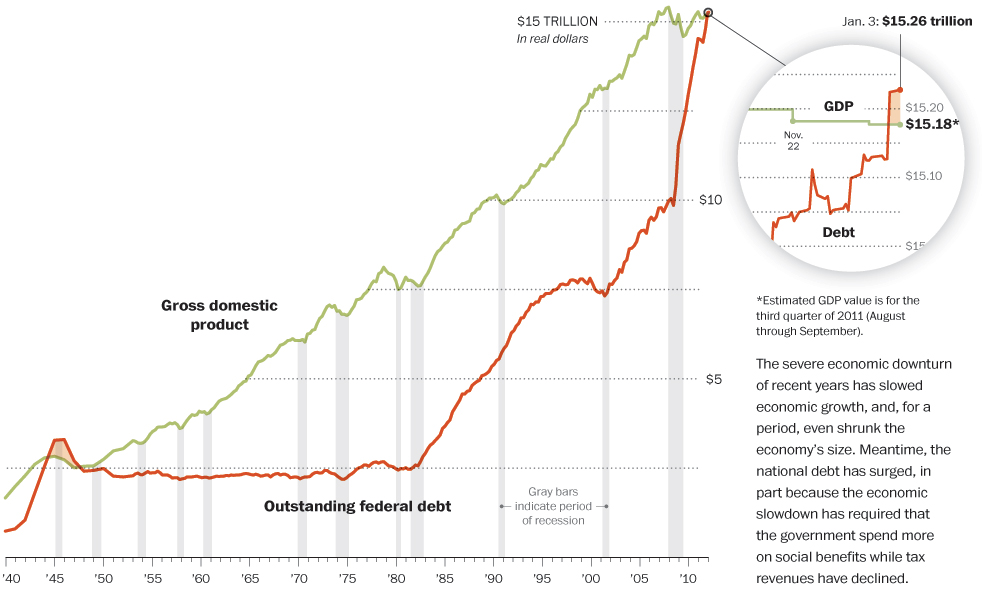

And this is after the country spent $16 trillion that it doesn't have (most of which came out of the hide of savers).

WASHINGTON — The Federal Reserve has taken many unprecedented steps in the past four years to try to boost the U.S. economy and counter the effects of a financial crisis that triggered a painful recession. It has kept the short-term interest rate it controls at a record low near zero since December 2008.

It’s bought more than $2 trillion in U.S. Treasurys and mortgage bonds to try to hold down longer-term rates. Those purchases have increased the Fed’s balance sheet to more than $2.8 trillion.

The printing press at work. The net effect is to bring interest on savings to zero (taxing interest 100%). Savers are paying for the debt run up by the debtors of this country.

Yep;no matter what one says or beleives its the FED distorting the markets.It just shows now unstable amrkets like equities are now days.One has to remember that the reaction to equities in the 70's recession was a generation that left the markets.Een now we see people who still resist what the FED policy favors and mnay experts warning of a Bond bubble.

Yep;no matter what one says or beleives its the FED distorting the markets.It just shows now unstable amrkets like equities are now days.One has to remember that the reaction to equities in the 70's recession was a generation that left the markets.Een now we see people who still resist what the FED policy favors and mnay experts warning of a Bond bubble.

Yep. And now the pain is moving into universal life policy holders:

In the next few years, millions of savers are in for a surprise that could cost them tens of thousands of dollars now—or hundreds of thousands later.

The reason: Universal-life insurance policies bought years ago when interest rates were high will face cancellation if policyholders don't pay more.

If interest rates stay low, many policyholders will face the unhappy choice of kicking in more money, accepting a lower death benefit or walking away, possibly sacrificing years of premiums they already paid.

Many people are "sitting on a ticking time bomb," says Kenneth Himmler, president of Integrated Asset Management, an advisory firm in Los Angeles. About 70% of the new clients whose insurance coverage he reviews are facing higher out-of-pocket costs because policies aren't generating enough interest income to pay costs, he says.

This is how the Federal Reserve cleverly steals money from savers to pay for all the debt that is piling on the American balance sheet. Slowly but surely, money is being shifted from retirees and savers to the top 1% who are the primary beneficiaries of Federal Reserve policies, the only group that has seen wealth and income gains under Greenspan and Bernanke. Someone has to pay for the trillions of dollars in U.S. debt, and guess what! The Federal Reserve decided it would be the middle class. No interest for the middle class savers for years and years to come, because debts have to be paid one way or another.

Wealth redistribution can go many ways and for so many life is now about getting someone to give them their wealth.

It is true, but it is undeniable (based upon every study that has been done over the last few years) that in aggregate, the only class that has seen wealth gains is the top 1%. There is absolutely no question that this is the result of Federal Government and Federal Reserve policies (it is a worldwide phenomenon) and many, many thoughtful government officials and economic heavyweights have been speaking out forcefully against these policies because they realize that the end-game is quite disastrous.

We have evolved from egregious debt practices with severe but manageable consequences (the tech bubble) to disgraceful and unfathomable debt practices with extremely severe consequences (the housing bubble) to surreal debt practices (current Federal Reserve extraordinary money printing) that can only have much, much worse results which will be caused by the bursting of the fully formed bond bubble (it has gotten so bad that Europeans are literally paying the German Treasury money to hold their cash).

Are we past the line of no return? Possibly. So many government agencies, corporations, and individuals are now so reliant on cheap money for growth and for managing debt, that the only possible way out may be explosive. Even current debt and revenue discussions really only amount to a total reduction of debt of about $100 billion/year? What about the other $900 billion?

There may be nothing we can do about it, but it doesn't mean we have to be ignorant about it and pretend $1 trillion dollar yearly deficit is nothing. It is huge beyond belief. So big, I am almost convinced that no one really knows what to do about it and they are just going to allow the worse to happen.

thats pretty much why i stopped contributing to the thread. any suggestions for offering ideas and help for staying ahead of the curve were met with the same political rebuttals and the i got it all figured out and i know better view , so i just ended it.

there are a few here who only know what they know and then make assumptions about things they know little about based on what they think they know and not how things are or really work .

when you have people telling others they know better and only their view is the correct one the conversation is over.

Politics - and the politics of economics - are the most important things now IMO (although I don't necessarily agree with anything anyone says here in terms of those things 100%).

I am a pretty experienced investor - with more money than most people - and I don't see any way to stay ahead of the curve right now (I have some sense of what you mean - but am not absolutely sure). At least for someone who is retired who can't or doesn't care to return to work now or 3 years from now. And/or someone who can't afford to take big hits to principal (most retired people can't). Even one of the last "value bastions" in terms of fixed income - municipal bonds - isn't anywhere near as attractive now as it was a month or two ago. Because - since Obama was re-elected - yields in the muni market have fallen to all time lows. And the risks have gone up.

Which I guess - as I've said before - is one reason why you deferred your own retirement. For someone who is relatively young - it's easier to keep working than to resume working after retiring. And it's why I have more cash on hand than I perhaps have ever had. Robyn

Only reason i put off retiring is marilyn needs another 2 years of time in order to get her severance package which is 3 years pay. She had the years but they discounted any non union time.

I like what im doing and the money is good so ill wait until she pulls the plug.

So far i have no complaints about any of my returns. My portfolio is up 8.5% and is only 3% equities at this point. Its 1/4 the volatility of the s&p.

If the markets fall by about another 10% ill start to shed some of the bond portfolio and shift some into a growth and income model and run both models.

I figure ill put about 3 years withdrawals in a money market ,10 years of withdrawals in the income model and the rest in the growth and income model.

Our income mix isnt overly rate sensitive so there is no rush to shed them.

The yield is about 3% or 3.5% so i cant complain.

If the volatility of the growth and income model troubles me at any point i can always shift back fully again to the income model.

The income model has always evolved to follow the bigger trend with appropriate matching funds so even if rates rise there are income funds we can swap for.

Last edited by mathjak107; 11-17-2012 at 06:17 PM..

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.