Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

The average Social Security benefit is $1328 per month.

Joe six pack won't get too far on that alone.

According to the Social Security snapshot it's $1,340.48 for Joe Sixpack and if married the spouse will get $688.51 for a total benefit of $2,028.99.

Not good in California or New York but in many parts of the country a married couple can do just fine on $2,028.99 as long as their home is paid for and they don't have consumer debt hanging around their necks.

If $2,028.99 is all they get it will be exempt from all federal income taxes and state income tax as well in most states. That's equivalent to $468 weekly take home or about a $14 to $15/hour job. Not pretty in my mind to be sure but doable in many parts of the country.

So for many couple the benefit is low but why is that? A little dated but it is the latest I have.

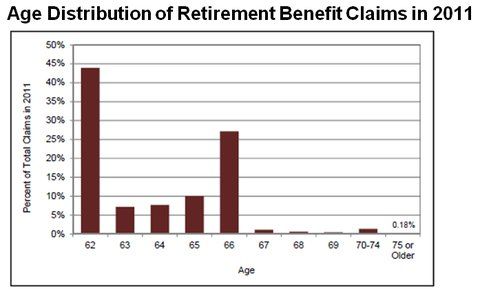

44% of social security recipients elected to receive benefits at 62 which certainly brings down the average benefit and on top of that I find it shocking to discover only 30% waited to full retirement age to start drawing benefits. You want to cut your benefits down? The answer to this is start drawing at age 62 and when social security is all you got you won't get much.

Joe Sixpack gets $1,000/month because he started drawing at 62 but if he had simply waited to 66 he'd get $1,335 and if he had worked to age 70 he'd get $1,757 and there is a lot of difference in the standard of living between $1,000 and $1,757.

If we have a retirement crisis it's educating people not to fall for the mindset "I'm gonna get mine now so I break even" or "I'm gonna collect early before they go broke..."

For MANY people social security is enough IF YOU ONLY WAIT. Husbands FRA benefit is $2,000 he'll get $2,640 if he works/waits to age 70 and if his wife receives 50% of his FRA benefit together they will receive $3,640/month free of federal and nearly all state income taxes. That is equivalent to $840/week take home pay which would be equivalent to a $25/hour job. Very doable and comfortable in 75% of the country.

So, Joe Sixpack only gets $1,000/month because he started collecting at 62. Don't want to come off as a hard ass but whose fault is that?

niceT4: There are situations when people need to take from SS at age 62. Not everyone who does that has the last name Six-pack. There are those of us who for many different reasons are forced into it by company lay-offs, shutdowns, and illness.

How do you presume that everyone who takes their SS at age 62 is some kind of loser?

According to the Social Security snapshot it's $1,340.48 for Joe Sixpack and if married the spouse will get $688.51 for a total benefit of $2,028.99.

Not good in California or New York but in many parts of the country a married couple can do just fine on $2,028.99 as long as their home is paid for and they don't have consumer debt hanging around their necks.

If $2,028.99 is all they get it will be exempt from all federal income taxes and state income tax as well in most states. That's equivalent to $468 weekly take home or about a $14 to $15/hour job. Not pretty in my mind to be sure but doable in many parts of the country.

That's also assuming they have absolutely no other income from any source at all. Most people could piddle around and make a couple hundred extra a month.

niceT4: There are situations when people need to take from SS at age 62. Not everyone who does that has the last name Six-pack. There are those of us who for many different reasons are forced into it by company lay-offs, shutdowns, and illness.

How do you presume that everyone who takes their SS at age 62 is some kind of loser?

I don't believe what nicet4 wrote is to be taken personally. Simply a statement. Again, you are taking it personally. I don't believe it had your name written with it.

you seem to be confused. Pensions ARE a saving mechanism.

As someone who has a (state) pension, about 9% of my gross income per paycheck goes toward my pension benefit. My employer also contributes.

This money goes into an actively managed fund that generates interest year over year through a variety of investments from bonds, to stocks, to commodities, to real estate.

The only difference between a 401K and my pension is that with a pension the benefit is defined. I can estimate my payout (provided my career path doesn't drastically change) fairly precisely. With a 401K you're more at the whim of the market- if the market overperforms during your investment period your payout will be higher. if it underperforms it will be lower.

There is no reason for retirement savings on top of my pension contribution. With social security (assuming its still there) I'll be well over 100% of my final average salary into retirement in perpetuity- with no kids and a paid off house. this is overkill- I can put those funds to better use in the present.

According to the Social Security snapshot it's $1,340.48 for Joe Sixpack and if married the spouse will get $688.51 for a total benefit of $2,028.99.

Not good in California or New York but in many parts of the country a married couple can do just fine on $2,028.99 as long as their home is paid for and they don't have consumer debt hanging around their necks.

If $2,028.99 is all they get it will be exempt from all federal income taxes and state income tax as well in most states. That's equivalent to $468 weekly take home or about a $14 to $15/hour job. Not pretty in my mind to be sure but doable in many parts of the country.

One thing I find irksome is how folks constantly refer to high COLAs and that if Soc. Sec. benefits can't provide a top-notch lifestyle THERE then it's not enough. Well, just like kids who go to NYC and seek their fortune while complaining they need 3 roommates to afford an apartment - YOU DON"T HAVE TO LIVE IN A HIGH COLA!

If you have the money, by all means, go ahead. But you could probably save a lot by only moving a few miles or an hour away...more by living in a rural southern or midwestern locale. You get to choose - live "poor" in the big city or live richer elsewhere.

However, pensions are a means of preparing for retirement. The pension is the guaranteed part of the retirement equation that you can't outlive. Generally, employers who offer defined benefit pension plans offer less current compensation.

There is also that small print on the retirement paperwork showing a disclaimer, of sorts, that a defined pension amount listed for an individual may, under given circumstances, be less than the currently stated amount in the future. That same statement shows on the Social Security retirement sent to upcoming recipients as well.

That provided both my husband and myself with motivation to save for our retirements when we were working even though we have defined pensions and currently get SS.

However, pensions are a means of preparing for retirement. The pension is the guaranteed part of the retirement equation that you can't outlive. Generally, employers who offer defined benefit pension plans offer less current compensation.

The combination of these two factors – earning less throughout one's working years, and having a larger portion of this income continuing beyond one's working years – legitimately calls into question the whole idea of saving for retirement. Rather, the idea is to live frugally, not incurring stupid or outlandish expenses; to set aside funds for emergencies or occasional treats; but otherwise to not fret over investment or accumulation of sizeable capital.

The concept of average people of necessity becoming investors, is recent; it might only be say 40 years old. The concept of overall frugality has been operative since the Neolithic revolution, but the need for becoming an investor for funding one's retirement, is a novelty.

So what's the point? The point is that persons who've had steady lifetime employment and who have recently retired at full retirement age (so, not early-retirees) have largely had the good fortune of not being dependent on individual investments for covering the bulk of their costs in retirement. For them, there is no crisis. For younger people, there is no "crisis" either, in the sense of dire urgency. But there is a slow decline in certainty and concomitant slow uptick in risk.

A crisis would eventually mount – say, in 30 years – if it remains imperative to become a successful private investor for funding a decent retirement.

Quote:

Originally Posted by Burger Fan

The only difference between a 401K and my pension is that with a pension the benefit is defined.

And this is an absolutely staggering difference!

With a defined-benefit pension, there is no palpable risk to the recipient, of market-crashes, bond defaults, interest rate fluctuations, currency fluctuations and so forth. Greece in crisis? Puerto Rico defaulted? China's economy on a downslope? Who cares. Unless the pension itself fails, none of these factors affect the defined-benefit pensioner. But if you have a 401K, all of these factors obtrude. Got a 7-figure retirement portfolio? Congratulations! Now consider the fact, that one single day's fluctuation in the market, could be larger than one entire year of your expenses! Comforting, isn't it?

With a defined-benefit pension, there is no palpable risk to the recipient, of market-crashes, bond defaults, interest rate fluctuations, currency fluctuations and so forth. Greece in crisis? Puerto Rico defaulted? China's economy on a downslope? Who cares. Unless the pension itself fails, none of these factors affect the defined-benefit pensioner. But if you have a 401K, all of these factors obtrude. Got a 7-figure retirement portfolio? Congratulations! Now consider the fact, that one single day's fluctuation in the market, could be larger than one entire year of your expenses! Comforting, isn't it?

Yes, it is! the defined benefit pension was one of the draws of going into state employment.

But to be fair, if you're diversified enough none of these things should really matter all that much to your 401K in the long run. In the short run yes, absolutely- this year was a bad year for a lot of funds, they're either negative or just breaking even due to the market going nowhere and oil being a bust. But if you're close to retirement your investment should be almost entirely in bonds and other "safe" investments to prevent market meltdowns from wiping you out in the first place.

I don't believe what nicet4 wrote is to be taken personally. Simply a statement. Again, you are taking it personally. I don't believe it had your name written with it.

Let me make it clear that I was not aiming at, or attacking, anybody.

I fully understand some people have been forced to take it to survive and had I contracted severe rheumatoid arthritis, to where I was unable to work, I could have been on of them. But with 44% taking it at age 62 something tells me not everyone that took it early had to.

But at age 62 I wouldn't have collected social security retirement benefits but disability because disability pays more. That chart clearly shows that at age 62 44% were collecting retirement benefits and not disability.

Many widows are forced to take it early to survive because their husbands didn't, or perhaps couldn't, obtain life insurance to "tide them over" to their full retirement age.

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.