Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

It makes sense things are slowing down. In aggregate, income data simply does not justify prices going much higher. It went up so fast so much for about 5 years 2013-2018, and people are just not making enough money for it to go higher. The exceptions would be markets where inequality is high, or markets that attract equity refugees and there's a high volume of wealthy people who can drop cash.

Speaking as a buyer and seller, buyers have to prove their income to lenders three ways from Sunday to get approved for a mortgage. Banks aren't giving out easy money to unqualified buyers for houses like they were in the mid '00s.

So it makes sense that banks are trying to hustle to sell refinance loans. There are probably a lot of people out there like myself who bought in the mid 10s, and seen ther property apppreciate 30-100%, but has now cooled down. Banks would LOVE to sell me money based on that asset. Since they can't sell as much money to unqualified people as they used to, they have to try and sell it to qualified ones.

They have softened the debt to income ratio's, so what

Student loans and mandatory medical insurance are crushing financial burdens for Millennials. Today's buyers are plumbers, welders, electricians and truck drivers in their twenties. They have passed millennials and left them in their dust, leaving the millennial asking, "What happened?"

The answer is that when they graduate, they should have a salable skill on Day 1.

Speaking as a buyer and seller, buyers have to prove their income to lenders three ways from Sunday to get approved for a mortgage. Banks aren't giving out easy money to unqualified buyers for houses like they were in the mid '00s.

how about this below for a first mortgage, not a HELOC & not hard money and this exact verbiage was sent to me this week.

No ratio program for primary residence (no income requirement, no income verification, no employment required, no employment verification) No CPA letter. No bank statements to support income

o ATR (ability to repay) exempt

o 100% Gift funds allowed for closing costs and down payment

So yeah, these loans are rising up from the ashes again. Don't shake your head. At least the loan program above requires a 30-percent down payment so borrowers won't walk away from it if they can't afford it(hopefully).

BUT the down payment can be all gift which puts little incentive to remain current if values start dropping. I have seen appraisal values come in low on a couple homes in the San Francisco area.

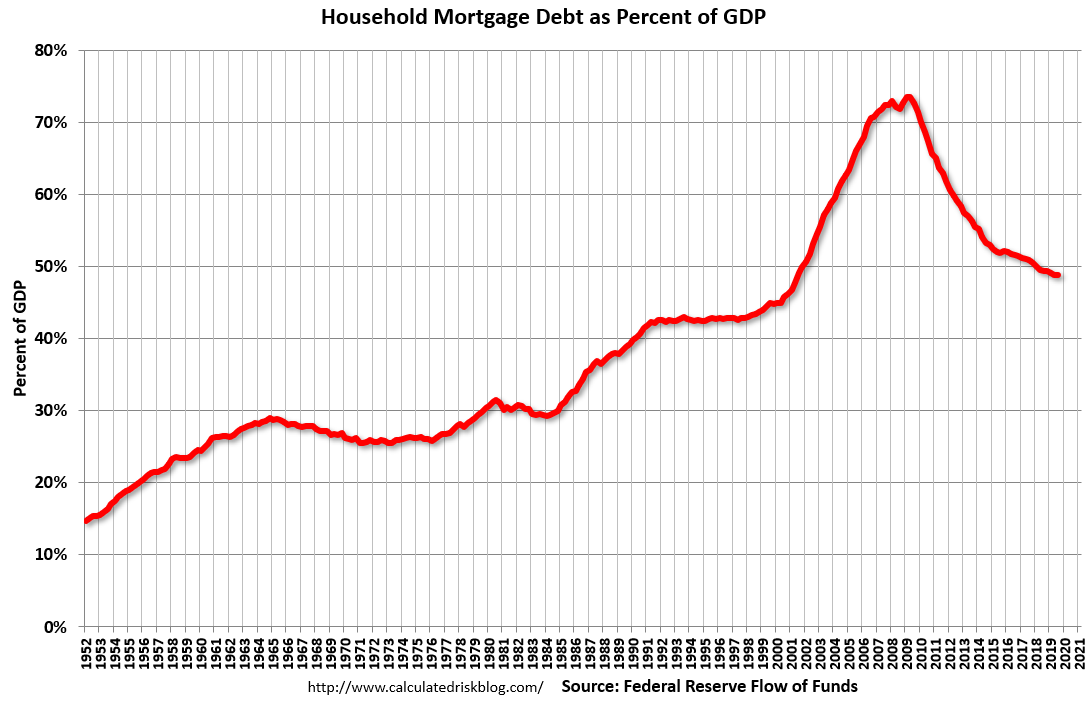

Stated income (or no income) has been around ONLY for investment properties but now it's slowly moving into primary residences which was protected by Dodd-Frank laws and income proof guidelines. I'm in the mortgage industry. The annual increases in conforming loan limits is another sign prices are moving up too fast.

how about this below for a first mortgage, not a HELOC & not hard money and this exact verbiage was sent to me this week.

No ratio program for primary residence (no income requirement, no income verification, no employment required, no employment verification) No CPA letter. No bank statements to support income

o ATR (ability to repay) exempt

o 100% Gift funds allowed for closing costs and down payment

So yeah, these loans are rising up from the ashes again. Don't shake your head. At least the loan program above requires a 30-percent down payment so borrowers won't walk away from it if they can't afford it(hopefully).

BUT the down payment can be all gift which puts little incentive to remain current if values start dropping. I have seen appraisal values come in low on a couple homes in the San Francisco area.

Stated income (or no income) has been around ONLY for investment properties but now it's slowly moving into primary residences which was protected by Dodd-Frank laws and income proof guidelines. I'm in the mortgage industry. The annual increases in conforming loan limits is another sign prices are moving up too fast.

The answer is that when they graduate, they should have a salable skill on Day 1.

Yes, of course. No one who pays the University of Northern South Iowa $200k for a degree in a "marketable" field will fail to immediately find a job.

Unless...

...they didn't win the lottery of predicting which fields will be super-hot that fall, four or five years out.

...they don't necessarily want to move to a stratospheric COL city and try to live with four other people on a starting salary.

...they don't necessarily want to move to some suckstandard city because that's where Gapple or someone is hiring that year.

...they look in the mirror at 24 and realize they let parents, counselors and idiots online push them into a career path for which they had no aptitude or interest, which gives them zero pleasure or satisfaction and means a life of chasing code-monkey jobs all over the country.

I'm starting to hear the "Interest rates are low! Property values are up! Unlock that equity to..." commercials. It's a sure sign of impending trouble.

I don't even know what means. "Unlock equity." ??? Take out a 2nd mortgage?

If you sell your house, you'd have to buy another one...in the same real estate bubble.

It may be by geographic area. Real estate is no longer hot here.

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.