Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

What would a 124,000 house look like on Long Island ? After paying it off, it costs you 600,000 and you think that's a good deal ? What happens when it come time to sell That 350,000 home might be worth 500,000 and you paid 600,000. Your 150,000 might be worth 225,000 and cost you 600,000.....who did better?

I think I made a better choice then you, sold my homes on the Island and bought elsewhere...with no mortgage, no interest or 0%. And I don't even understand finances

They don't get it Mike.

I honestly believe a lot of people here simply do not know anything about money.

They don't get it Mike.

I honestly believe a lot of people here simply do not know anything about money.

He a story, a little extreme but not that uncommon.

When I bought my first home in the early 90's and a few friends and family members also bought in that time frame, give or take a couple of years.

A lot of people got caught up in how much their homes were going up in value and made the mistake of ReFi's, remortgage, pulling equity and some extending loans.

Some people espically on L.I. ( and it happens everywhere) like to keep up with the Joneses. The want that shinny bran new SUVs, pools, expenses vacations and other luxuries they can't afford. So over the years they pull money from their biggest piggy bank their homes.

Many people on here say "plenty of people live here making half as much as......." Everybody's situation is different..... now back to the story..

My friend ( I've known since 1st grade) came down with his family to visit us last year. After knocking a few back and while the ladies were enjoying a nice bottle of wine on the porch I ask my friend how things are going. I guess the 6+ hour drive and the drinks got to him and he says things suck. He says he felt trapped, frustrated and doesn't know what he's going to do financially. I put the bottle of vodka away at this time.

I said things can't be that bad ( he brought a home for around 176,000 in 1996) and figure he was going to mention the dreaded T word Taxes but he went on a rant......I owe over 500,000 thousand on a home worth if I'm lucky 350,000 and 27 years on this current mortgage . I didn't know what to do or say...so I pulled the bottle back out and he drank until he passed out. He's far from the only one I know in this situation, most not as bad but still not that uncommon.

I was always taught get the lowest interest rate at the shortest time frame you could swing and leave it alone.

It's simple really, and i've been saying it for a long time now.

RE is not plumeting double digits. It will rise and fall the next few years in the 3-5% range. The examples being used are just plain stupid.

If people are really waiting to "Save" $10,000 on a house but pay 7% interest rate rather than 5% they aren't making a good decision.

Im just happy that 3 houses sold within 4 blocks of mine with, smaller yards, no pool and no 600 sq ft. detached garage. Homes are selling...just not for $500k for that cape or little ranch.

What would a 124,000 house look like on Long Island ? After paying it off, it costs you 600,000 and you think that's a good deal ? What happens when it come time to sell That 350,000 home might be worth 500,000 and you paid 600,000. Your 150,000 might be worth 225,000 and cost you 600,000.....who did better?

I think I made a better choice then you, sold my homes on the Island and bought elsewhere...with no mortgage, no interest or 0%. And I don't even understand finances

Live every other house on LI. Hence the arguement. Home prices are only worth what people will pay and prior to the flipping craze people bought their homes to live in, not to sell for a profit. Your also skipping that 124,000 is a heck of a lot easier to put a dent in with a downpayment. Also, if your paying that full 600K then your just like the idiot that paid 500K for a home that 5 years ago cost 350K.

Like I said, for me I'll go higher interest/lower cost any day of the week.

You'll feel really bad about what I've heard more then once: Banks willing to forgive 10-30% of principle and then reduce the interest rate to 2% to keep the homeowner paying their mortgage.

I wish I (who is years ahead on his mortgage) could get a 2%. I'd have my house paid off another 2-3 years early.

Sorry, do you want actual numbers?

Numbers caculated at Bankrate.com mortgage calculator.

Your house:

$350,000

4% interest

Payments: 1671/mo

Total house costs: $601543

Costs with addition $100/mo: $572203

My house:

$124,000

16% interest

Payments: 1668/mo

Total house costs: $600299

Costs with additional $100/mo: $365595

As you can see we don't need to find a home thats 10x less expensive, merely one thats very much within the norms for inflationary change. You can also see that for people like me who understand personal finances and can figure out how not to overspend my money, the 16% interest would be significantly better for me. My adding another $100 to my payements with the higher interest rate saves me $234704 vs your savings of $29340. We still aren't including down payments into the mix either.

I hope this helps you understand mortgage systems and accrued compounding interest.

As for your hypothesis that housing wouldn't decrease if interest went up: a product is only worth as much as people will spend. People have a set income, and they can afford a set amount per month. As such you postulate that the price of a house would stay the same and the person would accept a change of monthly payments for mortgages from $1670 to well over $4000?! I mean, even our illustrious and exhorbitantly paid public school teachers and police officers would have trouble paying off that nut.

I think you understand mortgage calculators just fine. But what you're missing is an understanding of the bond market and what really drives interest rates higher. That scenario/example up there, will never come to fruition the way you layed it out.

Think of this for a second: What happened in the RE Market the last time rates went UP 17x for 3 years straight? (from 1% to 7%)

I think you understand mortgage calculators just fine. But what you're missing is an understanding of the bond market and what really drives interest rates higher. That scenario/example up there, will never come to fruition the way you layed it out.

Think of this for a second: What happened in the RE Market the last time rates went UP 17x for 3 years straight? (from 1% to 7%)

OK - you got me... What happened in the RE Market the last time rates went UP 17x for 3 years straight?

OK - you got me... What happened in the RE Market the last time rates went UP 17x for 3 years straight?

From 2004 to 2006, home prices rose 60%+. Similar thing happened in the 70's boom when rates rose to 16%. What I'm trying to say is, Silverbulletz is putting the cart before the horse.

From 2004 to 2006, home prices rose 60%+. Similar thing happened in the 70's boom when rates rose to 16%. What I'm trying to say is, Silverbulletz is putting the cart before the horse.

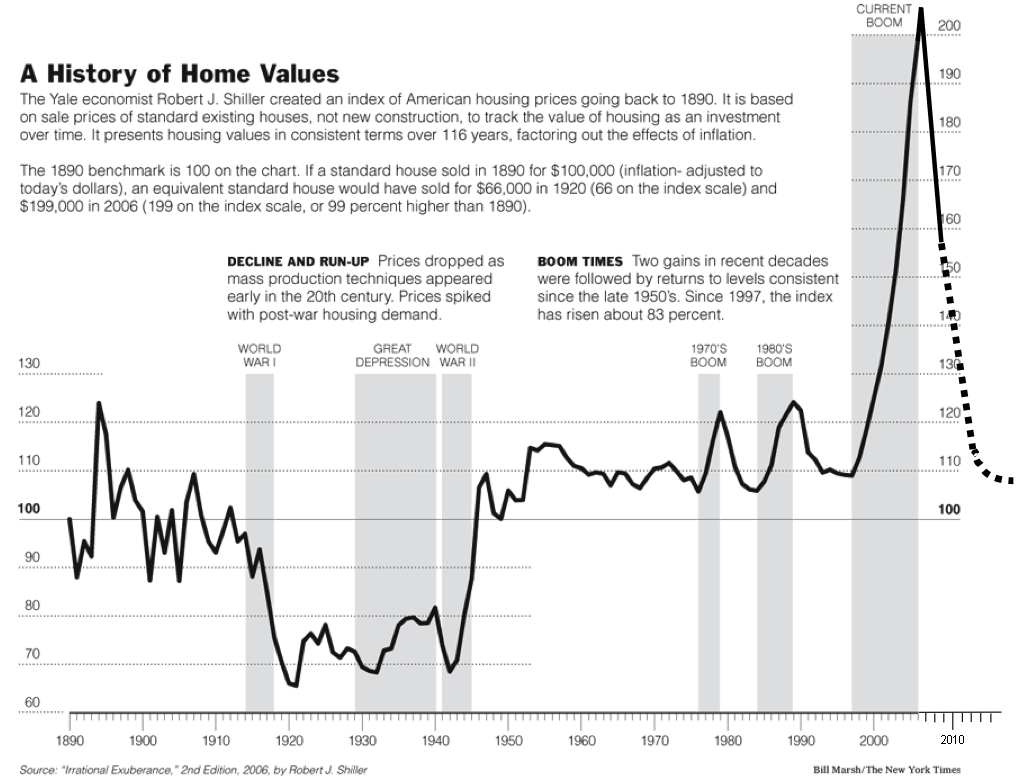

I thought as much, but wasn't sure... The numbers (values, rates) back your point, but I think you have to admit that there was so much more to the 2ks boom then the 70s boom. I'll throw a very infamous chart at you off the Shiller Index... I'm sure you've seen it before and my sole purpose of bringing it up is that I believe it prevents an accurate comparison to previous booms. It's disingenuous to say "a similar thing happened in the 70s".

I will say this... Stagflation was a term invented back in the 70s for what was happening - so many similarities to these times we're seeing today. But, it's not the S&L thing this time - it's the banks themselves that nearly ruined the economy for good and we're chasing our tails throwing bad money at bad money. Expanding the monetary base isn't quite working out the way it was intended and The Fed knows rising rates would poison the engine - which really are mortgages, credit, et al. QE forever.

Higher interest rates will not push the RE values up unless you start making some crazy inflation adjustments, we go back to the gold standard, or something drastic.

I thought as much, but wasn't sure... The numbers (values, rates) back your point, but I think you have to admit that there was so much more to the 2ks boom then the 70s boom. I'll throw a very infamous chart at you off the Shiller Index... I'm sure you've seen it before and my sole purpose of bringing it up is that I believe it prevents an accurate comparison to previous booms. It's disingenuous to say "a similar thing happened in the 70s".

Comparing inflation-adjusted charts from the 70s to now is not accurate. How CPI is calculated has changed (you know this)..it's going to skew 2000's bubble ++ plus we didn't have houses and condos in the middle of the desert quadrupling, or homes on swamp land in Florida tripling, in the 70's boom (or any other boom).

Quote:

Higher interest rates will not push the RE values up unless you start making some crazy inflation adjustments, we go back to the gold standard, or something drastic.

I agree, they won't push RE higher. Higher RE (and higher everything) will push them higher.

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

? After paying it off, it costs you 600,000 and you think that's a good deal ? What happens when it come time to sell

? After paying it off, it costs you 600,000 and you think that's a good deal ? What happens when it come time to sell

. I didn't know what to do or say...so I pulled the bottle back out and he drank until he passed out. He's far from the only one I know in this situation, most not as bad but still not that uncommon.

. I didn't know what to do or say...so I pulled the bottle back out and he drank until he passed out. He's far from the only one I know in this situation, most not as bad but still not that uncommon.