Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

In my rental neighborhood, some eastern european people have bought up the properties. Not sure if they used cash, or if they are backed by investors. One jewish guy bought property at what I'd consider double the cost last year. The EU guys may be jewish as well, since many of them seem to have settled in my area in the past maybe 10 years.

All the new people fixed up the properties FAST (6-12 mos) and they seem to be maintaining them well. Can't tell if they paid cash, but they do NOT seem to hurting for money. They did the expensive renovations in what looks like a good quality way. This is the difference as opposed to the last bubble.

Last time, tons of schmucks paid too much for the properties, and then obviously could not afford to fix them up. They started demolitions and renovations, and then apparently ran out of money. The three new guys we've had in the past 3 years fixed up fast and rented out the places fast. The other difference is that two of the properties had already had a lot of the demolition done by the previous borrowers.

No wild swings up or down here (Charlotte, NC). Zillow shows my neighborhood about 12% higher than the 2007 peak and 30% higher than the 2011 low. Since I have no intentions to sell, I'm hoping prices will drift downwards before the next property tax revaluation.

It doesn't seem bubbly since our housing prices are fairly consistent with incomes in the area (rather than financial wealth in the NY markets or Asian offshore money/tech unicorn money on the west coast markets)

I'm in Charlotte too. My area has had larger increases than where you are. We bought in Nov. 2010. Had the house appraised to refinance in Oct. 2015 and the appraised value was just a bit over a 50% increase in the price we paid. Increases in price since the bubble are, like everything in real estate, based on location, location, location.

I wonder then where all of the money is coming from to prop the prices back up. If they were inflated due to easy credit before the bubble, then collapsed, where is the wealth coming from to buy these? Foreign owners? Foreign Investors? Local Investors?

In noticed that my area has remained stagnant in the sense that there is still not much available for the lower middle class home buyers, which would be about the $200-275k price range. We're pretty much limited to shorts sales (invariably with 2 lenders involved; BTDT, lost a lot of money), foreclosures that are so wrecked that there are no COs and the contractors won't even touch them, or condos (which, by the time you factor in the common charges, end up costing more/month than a small single family home). There's really nothing we can so except continue to wait it out, pay rent, and save what we can in the meantime.

I bought my home in Feb 2015 for 150k

Sold in Feb 2016 for 160k (got tired of the neighbors across the street constantly partying out of their garage, numerous dogs barking, etc)....got a full price cash offer 2 days after putting it on the market

They wanted a quick close, cash offer on 2/13, I was closed out and in my new place 2/26

I wonder then where all of the money is coming from to prop the prices back up. If they were inflated due to easy credit before the bubble, then collapsed, where is the wealth coming from to buy these? Foreign owners? Foreign Investors? Local Investors?

When you look at the market as a whole, prices haven't been propped up across the board. For areas that inflated during the bubble, prices generally haven't recovered in nominal terms and they're still WAY DOWN in real terms (adjusted for inflation). The re-inflation you're seeing is a very local phenomenon. Look at the graph below to see what I'm talking about.

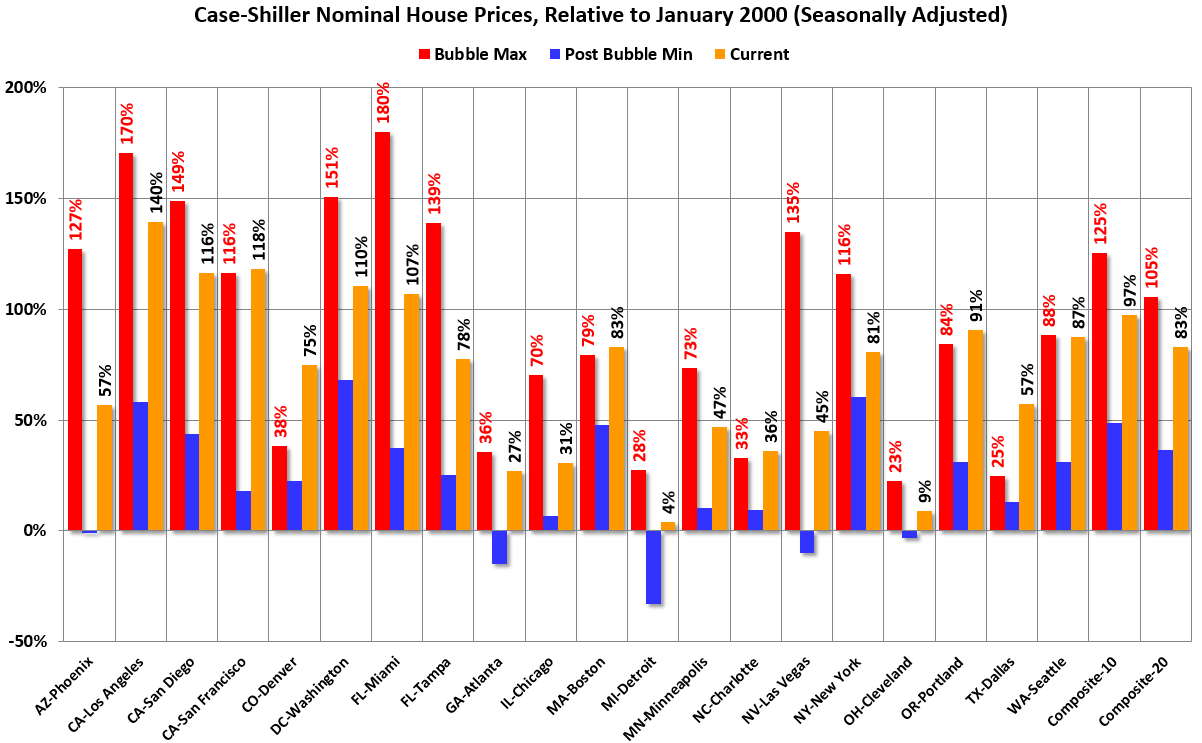

In my city (Seattle) the graph shows that prices have, on average, reached the 2007 peak. However when you look at the individual neighborhoods it's very uneven. The outlying areas and lower priced areas are not keeping up, whereas the more expensive areas are the ones where you typically see prices well in excess of the previous peak. IE: the money is mostly flowing into certain segments of the market while others remain depressed.

What this graph doesn't show is that it's far cheaper now to own a house (and keep it) than it was the last time prices were this high. 30 year fixed rate mortgage payments are 30% lower now, so these prices aren't nearly as un-affordable as they were 10 years ago.

I can't even fathom where most of the C-D posters live. I had my 1,800 square foot ranch house with 1,800 square foot unfinished basement built in 1992 for $120,000, in a nice new allotment on the good side of town. At one time it had increased to a staggering $155,000 in value, but now has settled to a more reasonable $135,000 value. The idea that a home could triple or quadruple in price due to "market forces" in a few years, then collapse because of a few changes in employement or banking rules is just crazy to me. And then it repeats.

What makes someone willing to pay $500,000 for a house that sold for $175,000 a few years earlier, in a neighborhood of $175,000 houses? Is it because people only look at the payment, or is it because of the 'greater fool' mindset that tells you to buy at whatever the price is because a greater fool will show up and pay more when you want to sell?

I can't even fathom where most of the C-D posters live. I had my 1,800 square foot ranch house with 1,800 square foot unfinished basement built in 1992 for $120,000, in a nice new allotment on the good side of town. At one time it had increased to a staggering $155,000 in value, but now has settled to a more reasonable $135,000 value. The idea that a home could triple or quadruple in price due to "market forces" in a few years, then collapse because of a few changes in employement or banking rules is just crazy to me. And then it repeats.

What makes someone willing to pay $500,000 for a house that sold for $175,000 a few years earlier, in a neighborhood of $175,000 houses? Is it because people only look at the payment, or is it because of the 'greater fool' mindset that tells you to buy at whatever the price is because a greater fool will show up and pay more when you want to sell?

Usually it doesn't repeat. The last downturn convinced a lot of people that huge fluctuations in house prices is 'normal' but before that it was fairly uncommon.

As for the scenario of buying a $500K house in a neighborhood of $175K homes - that is somewhat of an outlier. People do it, but by and large people buying $500K houses are in neighborhoods where that's the average price, not triple the average. Whether the houses were less expensive a few years prior doesn't matter so much if there are never any houses for sale at the prices from a few years prior. Here's an example of a relatively modest house near me that is now over $500K:

Mar 1, 2016

Sold (MLS) (Sold)

$520,000 —

NWMLS #885139

Feb 4, 2016

Pending

NWMLS #885139

Jan 15, 2016

Listed (Active)

$520,000 —

NWMLS #885139

Oct 31, 2001

Sold (Public Records)

$250,000 8.3%/yr

Public Records

Jan 3, 1995

Sold (Public Records)

$145,000 4.6%/yr

Public Records

Nov 27, 1989

Sold (Public Records)

$115,000 —

Public Records

You can see from the price history it was worth $145K 20 years ago. Now there aren't any $145K houses in the neighborhood, period. So anyone looking to buy a house at that price point isn't going to end up living anywhere nearby. Instead, the only buyers moving in are the ones paying at minimum $500K.

I can't even fathom where most of the C-D posters live. I had my 1,800 square foot ranch house with 1,800 square foot unfinished basement built in 1992 for $120,000, in a nice new allotment on the good side of town. At one time it had increased to a staggering $155,000 in value, but now has settled to a more reasonable $135,000 value. The idea that a home could triple or quadruple in price due to "market forces" in a few years, then collapse because of a few changes in employement or banking rules is just crazy to me. And then it repeats.

What makes someone willing to pay $500,000 for a house that sold for $175,000 a few years earlier, in a neighborhood of $175,000 houses? Is it because people only look at the payment, or is it because of the 'greater fool' mindset that tells you to buy at whatever the price is because a greater fool will show up and pay more when you want to sell?

If there is a mortgage a home can only be sold for the appraised price unless the buyer wants to pay the difference it it comes in low. Appraisals have a few variables but the main component is the selling price os similar homes in the area.

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.