Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

There were signs of an AZ housing bubble in 2005. Not everyone was caught unaware. Now, in 2022 if the government is going to o.k. those with a 520 credit score to qualify for a Fannie Mae loan and interest rates stay low well... people will buy homes many can't actually afford.

They'll obtain a loan which will put them in the house and a number of years later when monthly payments start to jump they'll default. Then the person next door who can afford their mortgage sees their property value drop. They find themselves getting deeper "underwater" and say I'm out too.

I bought in an area called Sun Groves in Chandler AZ in 2010. The homes were new. The home I bought was built in 2007. By 2010 the entire area has been deiminated. The person I bought the house from paid 270 grand in 2007. When he walked away in 2010 it was worth 150.

However note AZ is a non-recourse state. You'll be out your deposit and your credit score will take a huge hit but you can walk away.

It's amazing some people will keep talking about bubbles....they'll be right, some day...maybe.

What's more likely is there may be higher inflation which will cause all assets to increase in dollars, not necessarily value.

This will cause those bubble worriers to lose even more money than they have already.

There's a reason the stock market keeps reaching new highs...it's because prices keep rising, as costs keep rising.

People kept worrying about bubbles from 2015 - 2020, and now even with no evidence of a bubble, they keep repeating the same unfounded worry.

I guess you can keep living your life based on some very unlikely / uncertain events, and cost yourself more money over time.

The Fed thought it was a bubble in 2005. There was an FOMC meeting where Greenspan had the staff economists draw up analysis and charts in a presentation to show that the housing market was not in a state of a financial/economic bubble and they couldn't do it. It was covered in the financial press where the FOMC held a series of meetings to discuss the state of the housing market because of their nervousness.

In the end, they decided that they could raise interest rates because they felt that underwater homeowners would not be able to put their homes on the market. They assumed this would limit the house price decline. They turned out to be wrong.

As a result, we seem to be repeating the government foreclosure forbearance measures for Covid.

Bubbles occurred because the central bank saw asset price inflation could be monetized to enhance household income and acted on it by purchasing financial assets to force prices higher. Stocks, bonds, and mutual funds could be sold by households to increase their income. Households could refinance their homes to extract equity.

Prices on base models at the Vicenza community in Venice FL just went up by 6-8 thousand yesterday. Now up approximately 15% in the last 12 months. Inventory of resale homes virtually nonexistent, at all time lows.

Lumber prices have doubled in the last 6 months, copper up 50%. Inflation is coming back with all this federal reserve printing and government spending. Mortgage rates are very low but will rise soon.

There is little indication what interest rates will raise soon.

While not looking to make an economic or political debate, we cannot print money 24/7/365 and expect our economy to remain the same as it is now. With inflation (which we are already experiencing), will come higher interest rates. They are just being kept artificially low at present.

Rest assured taxes are going to increase as well.

As to soaring home prices, there are a variety of reasons.

However keep in mind that while some property values are skyrocketing, others are going down in places where people no longer want to live. High taxes, increasing crime rates, reduction of social and basic services are all contributing people getting out of urban areas of places like NY, and going to places in TX, AZ, FL, etc.

Thus if the demand is high in certain states/cities, and the supply is low, price go up. The opposite is true for the places people are trying to get out of.

I know people in LA & SF that are having trouble selling their place which has dropped in value due to homeless encampments just a couple of blocks away. The city has been housing some of them in adjacent rentals in SF, and wrecking them.

These were once $800k-$1 million dollar desirable locations, but now many are fleeing, and few want to buy, hence supply is high and demand is low.

I feel sorry for them, but now they are trapped with a choice of staying and things getting worse, or taking a financial loss.

Keep in mind that these places are not McMansions, rather in some cases fairly small homes or condos. So if they can sell before the bottom falls out further, they can by a McMansion in some place in TN, GA or the like.

But if they are upside down (or soon to be) they are faced with a horrible choice.

The Fed thought it was a bubble in 2005. There was an FOMC meeting where Greenspan had the staff economists draw up analysis and charts in a presentation to show that the housing market was not in a state of a financial/economic bubble and they couldn't do it. It was covered in the financial press where the FOMC held a series of meetings to discuss the state of the housing market because of their nervousness.

In the end, they decided that they could raise interest rates because they felt that underwater homeowners would not be able to put their homes on the market. They assumed this would limit the house price decline. They turned out to be wrong.

As a result, we seem to be repeating the government foreclosure forbearance measures for Covid.

Bubbles occurred because the central bank saw asset price inflation could be monetized to enhance household income and acted on it by purchasing financial assets to force prices higher. Stocks, bonds, and mutual funds could be sold by households to increase their income. Households could refinance their homes to extract equity.

I don't think we can compare what happened in 2005 to today. We are in a global pandemic that has changed behaviors across the board, making the SFH the most central asset to own during this shift in lifestyle.

Rising rates scarec those who are on the fence as they start to feel if they wait they can afford even less house .. so you have buyers and either short or undesirable supply

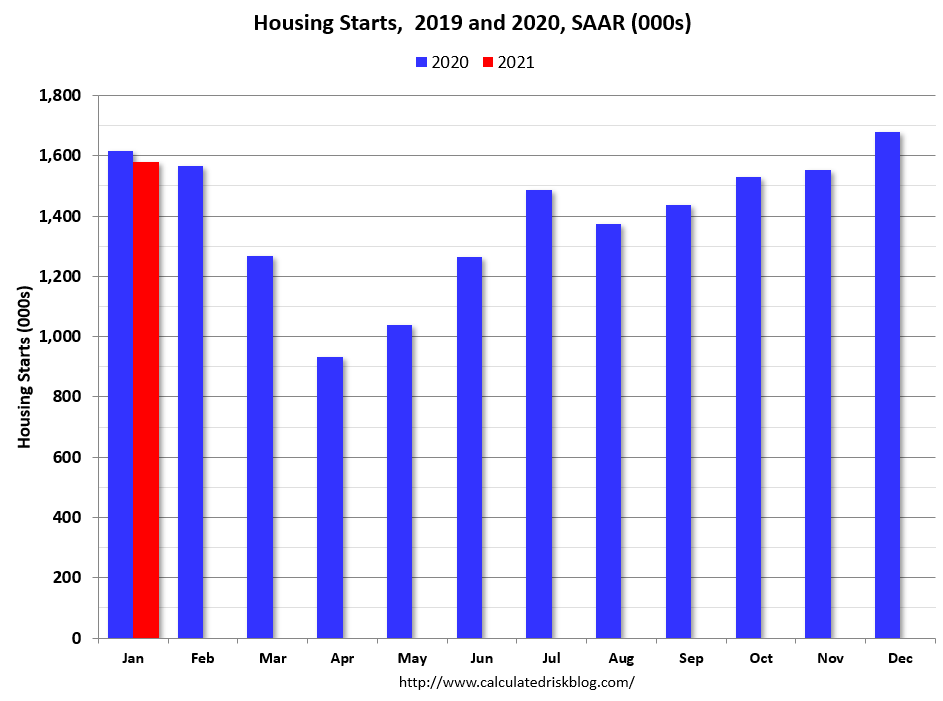

Those are starts. Permits are up sharply. Starts and completions are down because of the seasonality. Permits lead starts by a couple of months, and exceed starts by nearly 20 percent and completions by nearly 40 percent. The inventory picture will change.

Location: East of Seattle since 1992, 615' Elevation, Zone 8b - originally from SF Bay Area

44,551 posts, read 81,085,957 times

Reputation: 57728

Our median home here in Sammamish WA just went over a million, now at $1,055,726. When a house becomes available it's sold in 2-3 days with multiple offers over asking, and most go to a cash offer. As long as Amazon, Microsoft and other tech companies are paying $200k and more, there are buyers that can afford them. The majority of people with reduced hours or layoffs due to Covid are renters, so unlike the 2008 recession, there are no foreclosures do drive down prices.

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.