Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Re the regulators and powers that be anticipating and preventing any market irregularities--

Read this yesterday on Dallas paper business section...Andy Fastow who was the CFO for Enron and engineered most of the schemes within schemes that caused the company to implode has been "rehabilitated" and is working as some sort of financial analyst to sniff out hidden "problems"... i.e. Borderline or all the way illegal accounting measures used in company prospectuses (?) that other companies or individuals might want to invest in or buy...

Like the great forger and scam artist Frank Abagnale Leonardo Di Caprio played in "Catch Me If You Can" who turned over a new leaf and became an FBI consultant and started his own business security system...it takes one to know one...

And from the info in the article there are plenty of questionable practices going on today that apparently are common practice and either no one cares or doesn't really do that much due diligence...

I finally got the 2nd video to play. It is still not accurate for the purpose of this discussion.

1966 failed because of high inflation. So trying to use a non inflation adjusted bond which is what an spia is would not be an accurate comparison if you are just pulling out one scenario which is a high inflation one.

First of all no one in their right mind would use a non inflation adjusted annuity alone. They need an inflation hedge. Other wise don't compare them to a stock and bond portfolio.

The proper comparison would be spia vs just a bond portfolio.

So that 28/72 portfolio failed 19 rolling 30 year time frames to date. Know how many times a 35/65 portfolio with 25% in a spia from the bond budget failed ? None

Hello! The annuity failed EVEN WORSE from 1966 onward. Do you need cliff notes?

Inflation adjusted annuities don't pay 6.5%. The insurance company does not give free lunches. And you thought that you could just turn on a rider and get free money from those generous insurance companies? LOL

No. Proper comparison is to the lowest risk allocation, which would be somewhere around 30% stocks. Just do what the insurance company does.

You're lost in the word "fail" and the strict definition that Wade Pfau uses. The 30/70 portfolio with a 4% withdrawal rate technically "failed" from 1966 onward, BUT the SPIA did even worse! And you are comparing apples to oranges. You don't have to keep taking out 4% from the 30/70 portfolio when the SPIA is paying $10,000 less than the 30/70 portfolio. You adjust withdrawals and the 30/70 portfolio doesn't fail. So simple.

FWIW--one reason to commit to a low cost annuity is that you are doing just that--

Buying a certain peace of mind. There are companies like Vanguard and TIAA-CREF that do offer annuities at lower fee schedule than other companies...and both of those companies would be considered viable, long-term risks...

Basically you are buying a form of pension--a monthly payout that works with SS and does not react to what is going on with the market (good or bad)--

you just have to avoid second-guessing yourself...

If you have an IRA is it possible to buy a life annuity w/o considering that as a distribution and thus a taxable event on the lump sum---just on the monthly amount?

Would you have peace of mind if - 10-15 years from now - you had annuities from 5 different companies and it looked like 2 might go under? My father has 5 annuities that he bought 17 years ago - and I think one has a decent chance of going under in the next 3-5 years. Its bonds are now "junk" - and its stock has gone from a high of about 36 to about 3 today. OTOH - my father is 97 and has other sources of income. So I'm not particularly worried about it.

BTW - I advised him not to buy the annuities. But said if he did - he should buy from at least 5 different companies. He didn't follow my first piece of advice - but he did follow the second.

Took a quick look. Vanguard doesn't seem to offer SPIAs - only variable and deferred annuities. Mostly through outside insurance companies. TIAA-CREF seems to offer SPIAs as well. But only through its subsidiary life insurance company. I think that low fees are important when it comes to any investment - including annuities. But the safety of one's investment comes first and foremost when you're talking about an investment like this (it's not like you're taking a flier on a fledgling biotech stock). Robyn

But the safety of one's investment comes first and foremost when you're talking about an investment like this (it's not like you're taking a flier on a fledgling biotech stock). Robyn

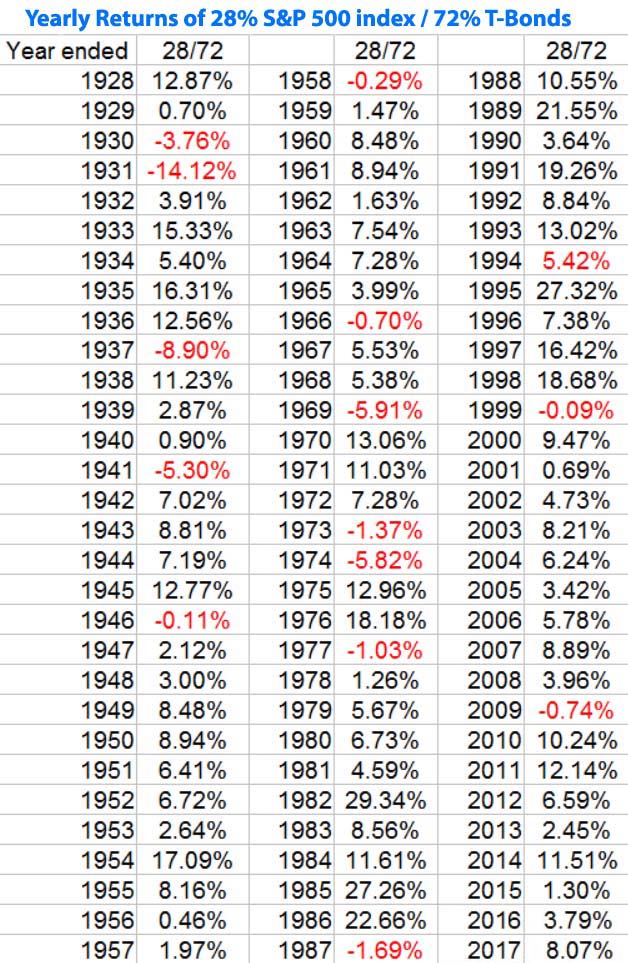

Does a mix of 28% S&P 500 index / 72% 10-year treasuries look unsafe?

duh!!!!!! no one ever said an spia can't be out spent . what is said is you can't outlive the income stream .

by itself an spia is like a non cola pension , if inflation climbs of course it can be out spent you just can't out live the income stream.

you are so bent on disproving something you and the video loser are making up your own terms .

with 13% inflation can't you out spend a non cola pension ? of course you will .

so you are mixing up issues .

you use a non cola adjusted spia with investments that act as an inflation hedge just as you would a pension that has no cola increases .

also your chart is useless without spending down from it in this discussion . it is meaningless i have no clue what that chart is supposed to prove .

yes it has proven over and over to be unsafe when spending down .

go run that data in firecalc with actual yearly returns and inflation . it failed to last 30 years 19x.

the latest update in the trinity study is a minimum of 35% equity's will get you a 90% success rate but little legacy money if outcomes are not above average. anything less failed to many times to be safe .

stop taking up the thread time with this trash . perhaps if you understood why you are wrong with what you keep posting you could actually add something beneficial but you are just clueless when it comes to this stuff and refuse to learn . .

no one here ever advocates using a non cola pensionized income like an spia without combining it with other investments to provide inflation protection , but you insist on making that comparison . .

Last edited by mathjak107; 05-01-2016 at 03:54 PM..

Re the regulators and powers that be anticipating and preventing any market irregularities--

Read this yesterday on Dallas paper business section...Andy Fastow who was the CFO for Enron and engineered most of the schemes within schemes that caused the company to implode has been "rehabilitated" and is working as some sort of financial analyst to sniff out hidden "problems"... i.e. Borderline or all the way illegal accounting measures used in company prospectuses (?) that other companies or individuals might want to invest in or buy...

Like the great forger and scam artist Frank Abagnale Leonardo Di Caprio played in "Catch Me If You Can" who turned over a new leaf and became an FBI consultant and started his own business security system...it takes one to know one...

And from the info in the article there are plenty of questionable practices going on today that apparently are common practice and either no one cares or doesn't really do that much due diligence...

Agreed. But even if companies are operating legally and ethically - they can get into deep doo doo as a result of situations no one could have anticipated. Like the current interest rate environment. Same with investors. And - as much as some people - especially seniors - like to think there's a "free lunch" out there somewhere - I don't think there is (except for the free lunches various financial firms invite me to all the time ).

Last time around - many seniors I know were juicing up their income with dividends from supposedly safe financial stocks - which went "poof". Next time around - who knows? Annuities are a distinct possible IMO. Just remember that there are very few investments that an insurance company can buy that you can't buy yourself. And that insurance companies can't turn straw into gold. Robyn

except insurers have a constant flow of dead body's on the annuity side contributing their money paying for those who live as well as almost 97% of term life policy's that go unpaid as well as 75-85% of whole life policy's cancelled and they make lots on them .

they also risk pool . all the riders and options they sell on policy's have the money going in to a reserve fund ..

they have a whole lot going for them that we don't .

Last edited by mathjak107; 05-01-2016 at 04:01 PM..

I would say that one reason elnrgby's attitude seems unworried is because she has a very adequate amount of resources to sustain herself in retirement...more that most people likely have...

Actualy, loves2read, my attitude was always the same, even in my 20s and 30s when I was dirt poor. I always start from what I want to do (where to travel, where to hike), and then look at how much money I have to cover it. When I was dirt poor, I would rent a VHS about the Himalayas from the library, and was enthralled thinking how great it would be to go there; when I was 52 looking at the enormous peaks all around me, I was enthralled to be there hanging off a rock, with quietly tremendous Mother of the Universe looming up above a cloud. Even if I lost everything in a highly improbable Annuity Armageddon that Robyn55 is predicting everywhere, I would still have the same attitude :-). Money is just what you get from people if you perform some useful service for them; it can give you a certain nice comfortable sensation, but it is not the reason for living. Nevertheless, I have had annuities for 14 years now, there has been no sign of any problems ever with them (including in 2008) , they continue to give me a feeling of security, and I never worry about them.

what is said is you can't outlive the income stream.

Wasn't that covered in the video? You can't outlive the income stream BUT it becomes an INSUFFICIENT income stream. It's INSUFFICIENT income that you cannot outlive. LOL

correct , it becomes insufficient . so does your pay check if inflation goes up and you get no raises . insufficient is not the same thing as not having an income base that goes on forever .

it is stupid to assume you can't out spend an income .

no one ever can claim you can't out spend an income, that is a ridiculous impossible claim , you can only not outlive an income steam . so for that guy making the video to twist a premise in to somehow you are never supposed to run out of money during the highest inflation period we had with no cola adjustments is just plain stupidity .

whether it is a non cola pension , annuity or your pay check with out raises you will always out spend it in high inflation but that income is still there as a base . .

the real premise is a portfolio with PARTIAL annuitization has had better success rates splitting the bond budget with an spia then the bonds used alone with equity's over much more outcomes .

out spending a yearly income is not the same thing as not having that income base coming in .

could you live on just your bonds paying 3 or 4% in a 13% inflation environment ? that is the comparison that moron is trying to make in the video by comparing an spia by itself and somehow coming up with the premise you are not supposed to out spend a 6.50% draw when inflation hits 13% .

an annuity is income you can't out live NOT out spend , just like your pay check if you don't get raises in soaring inflation .

the income base will always be there and require less money from your equity side , the same as if your pay check didn't pay all the bills and you lost your job and now needed even more money to close the gap without that pay check .

Last edited by mathjak107; 05-02-2016 at 02:44 AM..

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

).

).