"The 4% Retirement Rule Is in Doubt. Will Your Nest Egg Last?" (financial advisor, conversation)

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

I only have two index funds, VTI at .03% ER and BND at .035%, so technically I pay .0325 in fees. Both are ETF's, which I prefer to mutual funds. I like ETFs because there is no delay in calculating the NAV on the rare occasion that I buy or sell. Mutual funds lock in the price at the close of the market.

The main point I was trying to make, which apparently either eluded some of those who responded , or more likely I didn't express it well, is that I don't pay an advisor to hold my hand.........

Thanks for your reply. Your other points were clear enough to me, and made good sense.

Location: Was Midvalley Oregon; Now Eastside Seattle area

13,078 posts, read 7,519,082 times

Reputation: 9803

I remember when we were in Fidelity: Magellan, G & I, Contra, Div & Growth, Technology, all had 3% fees. Glad to pay too.

Vanguard had Wellington, Windsor funds, which we had later in our 50's. They too had a fee. Vanguard Index was just a few 10's of millions in the mid 70's.

Today, we have a very small amount managed thru a FA. Some is managed thru annuities. Some is self managed in trading accounts. Guess which account has the most volatility but the most gains.

I remember when we were in Fidelity: Magellan, G & I, Contra, Div & Growth, Technology, all had 3% fees. ....

I have never seen any mutual funds with fees anywhere near 3%. Something seems to be wrong with your memory. I just checked the Fidelity Contrafund. Fees are 0.86%.

I have never seen any mutual funds with fees anywhere near 3%. Something seems to be wrong with your memory. I just checked the Fidelity Contrafund. Fees are 0.86%.

back in the 1980s almost all popular fidelity funds had sales loads …..3% was pretty common back in those days ..but the sales loads were a one shot deal …once you paid the 3% sales load the money was tracked separately so you didnt pay it again when you swapped funds

Just because you might withdraw 4% or 5% per year does not mean you would spend all of it. You could have a very nice savings account after a few years!

My projections given the RMDs which as I posted earlier will force a much higher withdrawal rate than 4% as shown below, indicate that one of my "problems" will be figuring out what to do with all of the after-tax cash, assuming of course I survive long enough to have that problem. Stuff it in a Money Market account the equivalent of putting it under a mattress? I don't have any high-dollar hobbies nor any desire to own more stuff.

Another consideration if you are lucky enough to be in this situation, is that leaving a remainder in the IRA will create a similar "problem" for your non-spouse heirs, who will need to cash out the IRA within 10 years. So maybe that's an argument for drawing it out faster, taking on the tax burden yourself, so that cash will pass to your heirs. Depending on how much money you are talking about, might be wise to consult a CPA to get the best strategy in place.

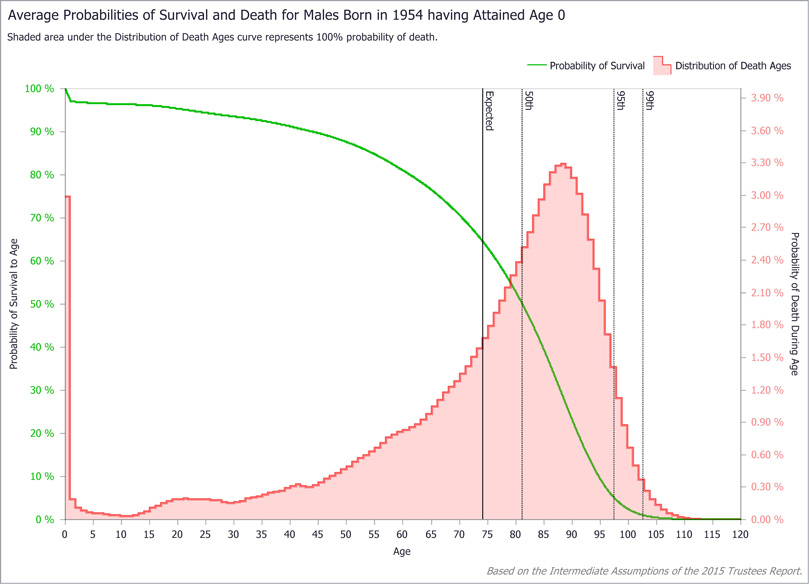

It's worth a look at the distribution of death ages to get some notion of how long you might be above ground. Chart from the SSA (2015) for males born after 1954 appears below for your enjoyment. One thing to note is the long tail on the left, many men die far younger than the "average life expectancy".

Yep, I don't get what the dilemma is with the RMD money, since you can certainly invest it back in the same asset class immediately.

Obviously there are some tax efficiency nuances in your asset allocation where you might do some shuffling to optimize across entire portfolio but generally speaking it seems like a non-issue.

Understand that the nature of consumer capitalism is to prick your anxiety so that you consume a product, service, experience or idea to *temporarily* alleviate your anxiety...

I see you never studied economics. That's OK; not everyone has had the opportunity.

There are numerous good online courses that can teach you the basics of economics and how capitalism has maximized value for society, and for most of them, you don't even need to have an understanding of calculus. Many of these online courses are free of charge.

Yep, I don't get what the dilemma is with the RMD money, since you can certainly invest it back in the same asset class immediately.

Obviously there are some tax efficiency nuances in your asset allocation where you might do some shuffling to optimize across entire portfolio but generally speaking it seems like a non-issue.

You mean to re-invest it into a taxable brokerage account? Yes that's one possibility, but now in addition to passing IRAs to your heirs, you've got to deal with more brokerage accounts and will probably need to rewrite your will to address it. Maybe that's the way to go, but it does complicate life. I am all about simplicity, don't need to strive to squeeze out every last penny until my dying day.

Here's a link that describes alternatives for RMD re-investment. Of course it's a sale pitch so use accordingly.

usually the ira funds are part of the income generating pool ….so it isnt a case of squeezing out every penny , it is a case of maintaining the swr that you are drawing based on a specific allocation

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.