Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

I have noticed several people saying they would not do something like funding kids' college or paying debt off unless they were maxing their 401k. What is the reason for thinking you need to put in the absolute maximum allowed by law, instead of simply an amount that is appropriate for your expected expenses, age, etc.? Not all of us want to have a super-lavish retirement at the expense of a somewhat better life now.

edit: Mods can move to Personal Finance, I meant for it to go there.

Because many people know having a fixed sum at retirement may not be enough for what life may throw you.

Congrats! You've figured out why I said someone in California might not feel so safe, and maybe learned why simply stating what you did when others might not live in California doesn't make much sense.

Quote:

Originally Posted by NewbieHere

You are not living in USA, is that correct assumption.

Correct assumption, but I did live in the United States for awhile after retiring and that is what I'm basing my post-retirement spending patterns on.

Good for you. In your experience... would you describe your pattern as typical or not?

I'm not sure, as I've not compared notes with many others. I'm curious as to how you reached your conclusion to inform everyone that they would spend 33% more just because they have free time. Was that your own experience with your spending after retirement?

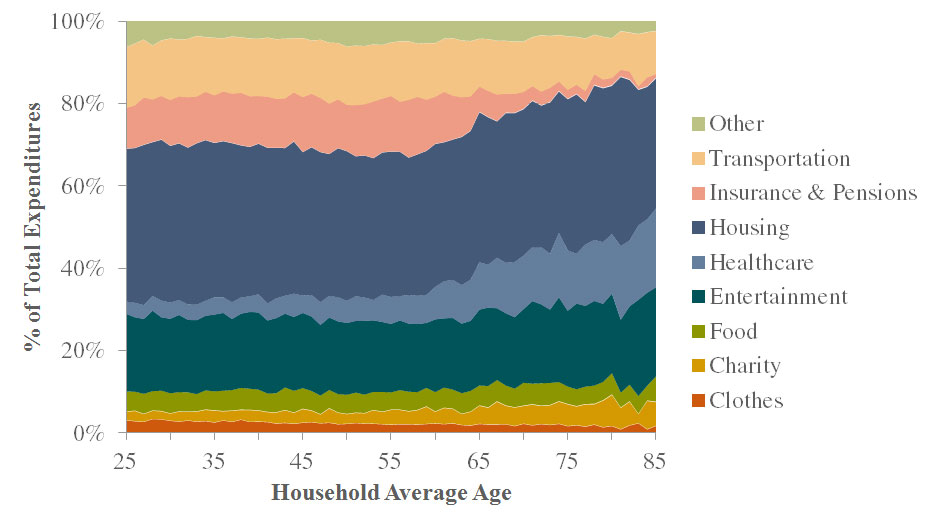

Blanchette has some fairly recent research on spending patterns through age, and he sure didn't find some gigantic jump in entertainment spending at retirement age to fill their spare time. His stuff is here: https://www.retirement-insight.com/e...st-retirement/

Is there any research that supports this massive increase in spending you have laid out as what will happen?

Quote:

Originally Posted by MrRational

But the question, the premise, is about what would likely be done if that 25% was available to be spent.

Not having it makes it easier to not spend it.

The person saving 25% has it, they choose to save it.

the study's on senior spending have had a few flaws . for one thing for many seniors spending falling off may be a function of necessity as they both spend down assets and have fear of over spending what is left that they do have .

old retirement planning was not as much a science as it was since the work of bill bengan so many before us just over spent early on ..

also different groups have different mentality's about spending . my grandfather had a great depression mentality and shuddered when he had to spend .

my dad was a great depression child , if it wasn't needed he didn't buy it .

our generation likes to do things for our grand kids or kids . spending may slow on us but if we have the money it will just shift to spending on the grand kids .

healthcare costs were not as out of control in those study's they did on past generations .

while it was believed seniors were effected less by inflation because what they stopped doing and buying helped pay for the increases of what went up ,soaring healthcare costs and long term care costs may make that not true anymore.

the trend is to try to stay home now and not go off to a home . expensive modifications may be needed , we are living longer too and we are active longer . traveling may require more comfortable first class or better hotel accommodations as you age .

there are lots of reasons how they think we spend our money as we age may not be the case anymore .

but i can tell you this , regardless of age if i gave anyone here 100k to spend as they like , and the stipulation was they had to spend it ,regardless of age they will all find a way and enjoy every penny . like i said if i did that yearly for them that would become their lifestyle yearly .

retirement is not just about paying bills for many folks , it is about having quite a bit of discretionary income to enjoy .

Last edited by mathjak107; 02-01-2017 at 03:14 AM..

Tax advantages, because you can't take loans to fund your retirement, the ability to retire early if one so chooses, the fact that many people will spend equal or more years in retirement than the did working (adult jobs)....or simply, because they can.

We are entering our highest taxed years of our adult lives, you BET we are going to sink even more money into our retirement accounts to offset some of those taxes. Our house is almost paid off, we lose our last "kid" deductions and sinking more money into 401K's is really the only tax shelter we have. We make too much to get any tax benefit from IRS's, our accounts took a huge hit in 2008-2010 and while they are looking nice again, we want to have enough set aside that a huge drop in the market doesn't mean we have to work for 5 or 10 more years like many, many people found that were nearing retirement because they had only put in enough to match....

the study's on senior spending have had a few flaws . for one thing for many seniors spending falling off may be a function of necessity as they both spend down assets and have fear of over spending what is left that they do have .

old retirement planning was not as much a science as it was since the work of bill bengan so many before us just over spent early on ..

also different groups have different mentality's about spending . my grandfather had a great depression mentality and shuddered when he had to spend .

my dad was a great depression child , if it wasn't needed he didn't buy it .

our generation likes to do things for our grand kids or kids . spending may slow on us but if we have the money it will just shift to spending on the grand kids .

healthcare costs were not as out of control in those study's they did on past generations .

while it was believed seniors were effected less by inflation because what they stopped doing and buying helped pay for the increases of what went up ,soaring healthcare costs and long term care costs may make that not true anymore.

the trend is to try to stay home now and not go off to a home . expensive modifications may be needed , we are living longer too and we are active longer . traveling may require more comfortable first class or better hotel accommodations as you age .

there are lots of reasons how they think we spend our money as we age may not be the case anymore .

but i can tell you this , regardless of age if i gave anyone here 100k to spend as they like , and the stipulation was they had to spend it ,regardless of age they will all find a way and enjoy every penny . like i said if i did that yearly for them that would become their lifestyle yearly .

retirement is not just about paying bills for many folks , it is about having quite a bit of discretionary income to enjoy .

I agree. I'd have to do some digging for the exact numbers but at one time it was said that during the first 10 years of retirement, people spent more money than they did during their most expensive working years--they finally had time to take long vacations, they had grand kids to travel to see and spoil, maybe they bought a lake home or RV, etc. In generations past, kids rarely moved more than 30 miles away from where they grew up and people lived in the same home, worked for the same company most, if not all of their adult life. That just isn't the case any longer. You don't see elderly that need assistance moving in with children any longer, they want to stay in their own home or move to assisted living--so the end years are much more expensive. Then factor in that people would work until they were 65 and die within 10 years of retiring most often and hearing someone living until 90-100 was a rare event. Now, actuarial tables have people living to 120 in the not to distant future. Given most people enter the adult workforce around age 22, retire at 65-67, giving them 45ish years to work, and 35ish years of retirement, people are going to outlive their savings if they are only putting in the minimum.

Congrats! You've figured out why I said someone in California might not feel so safe, and maybe learned why simply stating what you did when others might not live in California doesn't make much sense.

Correct assumption, but I did live in the United States for awhile after retiring and that is what I'm basing my post-retirement spending patterns on.

It's true, I'm only aware of laws in California. Why would I know any other state? But then your statement about what you need to retire is also less accurate. You live overseas, not in USA. Pot's calling kettle black?

Last edited by NewbieHere; 02-01-2017 at 08:41 AM..

in fact , while we would not do it again we went for the farm experience at the stone barn at blue hill on the old Rockefeller estate recently .

we got selected to eat a few dishes at the chef's table in the kitchen . they had 25 master chefs from all over the world , each one specializing at something else . there were only 25 tables in the restaurant .

we took photo's in the kitchen that were pretty cool . if anyone is interested i can post some .[/quote]

MJ, Would like to see photos. I read about this in a publication the title of which escapes my memory. I would try it once as well. Personally, I love golf. One of the things I would like to do in retirement is play the world's best courses, including Pebble Beach, Sawgrass, Bay Hill, etc. One round could cost several hundred bucks. If I could play Augusta I would pay thousands. I would also like to play the old courses of the R&A, in Scotland.

Other than a few indulgences we are naturally conservative folks. My present goal for the next handful of years before retirement is to fully fund a Roth before putting whatever else I can afford into my 403b. We are planning on maxing our last couple years, with catch-ups included. That's a good amount of money, 61k each year, if we can pull it off.

To the OP, that being said, not all folks will be able to do it. We have maxed only a few years, and then have had to back it off. But we consistently make efforts to get as much as we can into our retirement savings. There are too many costs that could arise and we are trying to be as prepared as possible without living in stark or meager conditions. I guess it's a balance based on priorities, in the end.

DC

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.