Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

People just won't save significant money. In most cases, probably 80%, it's a choice. The "Next 9%" income earners (which exclude the top 1%) only save about 12% of their income...and this income range starts at around $133K and goes up from there.

Indeed. The upper middle class needs to live like the mainline middle class. The mainline middle class needs to live like the lower middle class. People earning $100K (in the Midwest) should be driving 7-year-old cars bought for cash from Craigslist, sending their kids to public school, and doing their own basic home-repair.

There are lots of folks struggling, say in the bottom half of the earnings range. In many cases, there are entirely legitimate and understandable reasons for their inability to save. Bookstore self-help financial advice isn't really geared towards such people; often, it is condescending, preachy and irrelevant. But the real travesty isn't among that audience. It's among folks who in principle DO have disposable income, but who choose to dispose of it in unproductive ways.

Quote:

Originally Posted by CrownVic95

You're right, it is tougher today economically for young people just starting their adult lives.

It's tougher for the so-called working class. It's tougher for people from broken families, who have to unlearn deleterious habits before even beginning to save money on their own. It's tougher for people who spent exorbitant amounts on fluff degrees. But it isn't any tougher for say chemical-engineers, who graduated with a 3.5 or better, from their flagship state PUBLIC university.

America has always been a vituperatively individualistic society, with little patience for the less-fortunate. What's changed recently, is that the "less fortunate" is mainstream people... not brown people with funny names from the neighborhoods where Ryan Homes doesn't have any developments, but now the sort of people who might appear on commercials on TV. Bad luck has gone mainstream. But it was always there.

Location: Live:Downtown Phoenix, AZ/Work:Greater Los Angeles, CA

27,606 posts, read 14,623,335 times

Reputation: 9169

Quote:

Originally Posted by boneyard1962

That's fine if you trust the Fed with your future. I do not. For me SS is the maybe money. I'll count it when it's in my bank account.

Until my father died, they were going to retire with IRA's, a 401k, money saved AND SS paying the top benefit, all with no debt. They planned on living solely on the SS for day to day with all the savings to fall back on in emergencies

Im in the same boat. Grew up poor and learned to save young. I agree with your entire post. Life is about choices. When I buy something I buy quality or not at all. I never finance a toy, vacation or cellphones. I learned early, worth having worth saving for it. I always put something into savings since I was 18. Even if it was only $5.00 I made it my habit, almost an obsession.

When I built my house I owned the land for 5 years. Worked tons of OT and 2nd jobs to save. A lot of those second jobs were to learn skills. I dod my own drywall, trim carpentry, painting, landscaping and flooring. The 5 year wait bought me time to save and to learn. It also required a lot of sacrifice.

My friends laughed and said just pay someone. Just finance it all. Yeah I could have done that. Many times I almost did. Now I have close to a million in a retirement account that is doing very well. I retire this year.

Many co-workers, in fact most who make the same as I do, have less than half what I do. They trusted in tomorrow. Ill start putting more in next month. Ill start saving next month. Always next month. Odd they never waited to trade in that 3 year old car until next month.

LOL I know 1 guy financed an $18,000.00 tractor for his 1 acre yard. Needed the bucket loader for doing mulch. LOL He knows he can't retire before 65. I wonder why.

That's a great story. There are still people like you out there, I met one the other day. He is in his early 60's and works 60 to 70 hours every week. Guy came in and did my tile floor on a Sunday (I tried to do it myself but my tile saw, coupled with my lack of experience, was not up to the task) While I don't think it is necessarily healthy to work that much, this guy is a perfectionist, does great work, and pays cash for everything. It's good to hear you have accumulated that much in your savings account. While I have much less, I have enough to provide myself a comfortable retirement. I also have some long term investments that I believe will pay off handsomely in the next 5 years, when I'm ready to retire. I have always driven paid off cars, and made double payments on the mortgage to pay it off early. I just sunk a bunch more money into the house (put on an addition) and was able to borrow my own money from my 401K to finance it. Instead of paying back the bank I'm paying back myself. Yet another advantage of putting money away when you're young.

You had it easier too the people that still have 25+ years left to work before they retire have it the hardest. Wages and raises are horrible now in relation to inflation and the cost of living. The stats are all there. The country is going downhill.

Don't wanna hear it. I had my pay cut 6 years ago and just got back to my previous pay.

How much money do supposedly poor people spend on the following non necessities?

Food at restaurants

Tattoos

pot/alcohol/recreational drugs/cigarettes

overpriced groceries

$5 coffees

The country's going downhill all right. On that much we agree. That's because we have an increasing % of people who act helpless and who are looking for a savior. You don't overthrow an elite without self discipline.

Indeed. The upper middle class needs to live like the mainline middle class. The mainline middle class needs to live like the lower middle class. People earning $100K (in the Midwest) should be driving 7-year-old cars bought for cash from Craigslist, sending their kids to public school, and doing their own basic home-repair.

Correct. And if the people in the top 1/2 of the income distribution lived as such, they would have plenty of financial security and many would be able to retire before age 65.

Quote:

Originally Posted by ohio_peasant

There are lots of folks struggling, say in the bottom half of the earnings range. In many cases, there are entirely legitimate and understandable reasons for their inability to save. Bookstore self-help financial advice isn't really geared towards such people; often, it is condescending, preachy and irrelevant. But the real travesty isn't among that audience. It's among folks who in principle DO have disposable income, but who choose to dispose of it in unproductive ways.

I only half agree on this one. It is a horror to me that the "next 9%" save only 12% of their income. I certainly agree that bookstore financial advice doesn't help you if you're making minimum wage. At that point, you really do need to earn more money.

The horror I see with the poorer 1/2 of the population is the having kids outside marriage thing. That's a financial disaster and a disaster in lots of other ways, too.

Quote:

Originally Posted by ohio_peasant

It's tougher for the so-called working class. It's tougher for people from broken families, who have to unlearn deleterious habits before even beginning to save money on their own.

Correct. The hard part is you can't convince a lot of these folks that stuff like having kids outside marriage is a disaster for them and their kids. They get mad at you if you tell them that. But then they get mad and resentful that their fate is in the hands of others...yet won't admit they put themselves in that situation...so many are always looking for some kind of savior..."out there".

Quote:

Originally Posted by ohio_peasant

America has always been a vituperatively individualistic society, with little patience for the less-fortunate. What's changed recently, is that the "less fortunate" is mainstream people... not brown people with funny names from the neighborhoods where Ryan Homes doesn't have any developments, but now the sort of people who might appear on commercials on TV. Bad luck has gone mainstream. But it was always there.

Yep. I can't disagree with that. Things have gotten tougher in a lot of ways. But it seems like 2 things are happening at the same time. Things are getting tougher, while people in general are getting weaker and less disciplined. The 2 trends seem to feed on each other. Undisciplined people are easy to take advantage of and the more they get taken advantage of, the more they look for outside saviors....who either do nothing for them or take advantage of them some more....and on and on it goes.

Did I miss it or why doesn't this guy have social security? That would be a big help even if he had to work.

I am frankly tired of hearing this old lie. Elderly get social security, medicare, and discounts on things just for being old. There are reverse mortgages... over 55 housing. The whole world bends the knee to them. And as was mentioned, they had their whole lives to save for a rainy day or invest... they chose not to.

I agree that there is a horrible age discrimination problem but honestly what do they expect? Their problem is that they believed the lie that they could work forever and never looked into reality or planned for problems down the road.

The media just *loooovvvees* this kind of story as it tugs at the heart and says we need to do more. But as usual.. it is the people who have it pretty good that just keep on complaining. As recently as 1930 there was no social security or medicare. If you were old and a woman you might as well just kill yourself because life truly wasn't worth living. You had to work all day doing laundry or some back breaking work, no time off... and no sick days and you could be fired for any reason.

Why can't they do jobs like other people: Uber, Left, Safai, Task Rabbit.. and a gazillion other ways of making money.

No they have to go find the worst job they can find so they can day "oh woe is me". No you chose all of that and now you want the world to feel bad for you. Nope.

I know a few young people who are in severely dire straights. No income, no family, and no ability to get an education because of the insane tuitions. But they just do they best they can and cheerfully live in a house with 20 other people and sleep on the floor. It is all about expectations.

The biggest telltale to senior poverty is when you retire. Is it 62, 66 or 70?

I'm one of those who's 69 years old and not yet collecting social security benefits; I will start to collect when I am 70.

The problem is nearly half (44%) of people collecting collect at age 62 and it is this half that can least afford it. Take someone who's FRA benefit might be $1,800 but they opt to grab the money at 62 so they get only $1,350 which is poverty. The same person can wait to age 70 and get $2,376 which is nearly twice as much then they would have received at 62.

I am waiting, my wife started collecting 50% of my benefit at age 66 when I filed and suspended, and when I do start to collect our combined monthly social security benefit will exceed $4,300 or over $1,000 weekly.

Now here is where the real kicker comes in for those of you who don't know it.

Most social security benefits are exempt from both state and federal taxes.

Did you know that up to 85% of your Social Security Benefits may be subject to income tax? If this is the case you may want to consider repositioning some of your other income to minimize how much of your Social Security Benefit may be taxed and thereby, maximize your retirement income sources.

OK, let's assume my wife and I collect $4,300/month for $51,600. How much federal tax will we have to pay on that if we have no other income?

Yep, you read that right... our federal tax liability on that is a big fat zero and social security is exempt in most states as well. I know it is exempt in California, Ohio and Georgia. A big fat zero. That $4,300/month is exactly like take home pay or it is equivalent to a job earning $65,000 so there you go.

But people will take it early and have to continue working... what happens if a couple takes benefits early for $2,000/month and earns $2,000/month working like dogs?

That is right; they will pay $300 federal tax on the $24,000 ss benefit PLUS they will pay taxes on the $2,000 earned as well.

Taking early is dumb unless you are dying or starving.

How long have you known this guy? How do you know he didn't do the best he could. Not everyone was born into privilege and not everyone is overpaid. And if everyone " got more education" then MORE would be skilled and suddenly your overpaid job doesn't overpay you anymore. Try actually earning your pay before spouting platitudes!

Not who you were talking to, but we as a society must come to grips with the fact that at least a decent part of this problem is that people are CHOOSING not to save for retirement.

It is valid to bring up other problems in society, but we can't ignore that our materialistic and impulsive culture values living for the now more than the future - this goes for more than just saving for retirement, but for the environment and other things too.

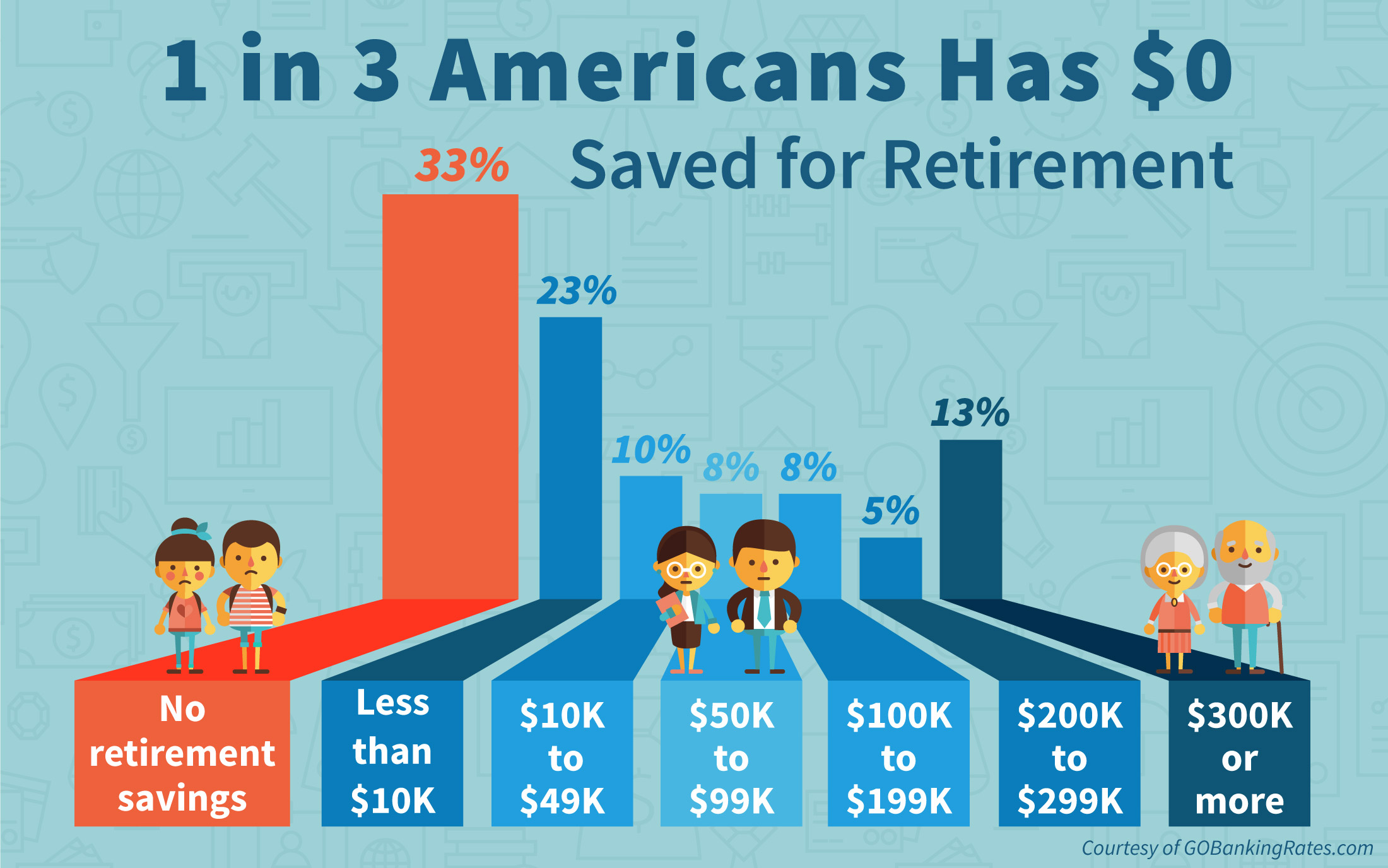

It is impossible to have these numbers if fiscal responsibility was mainstream in our culture:

I know a guy who was throwing a party, with decent food that he bought, 2 newer trucks in his driveway, and at this party he was showing my pictures on his iPhone of his recent vacation to Jamaica. Later that evening he told me that it was "impossible" to save money for retirement, because of banks, and big corporations, and bad pay. Choices. He has money for plenty of luxuries. We make bad choices in our culture and then point the finger elsewhere.

I work at a poor school district - don't even make $45K a year, am not even 40 yet, and still have more saved up for retirement than about 4 out of every 5 adults out there. Choices.

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

I had my pay cut 6 years ago and just got back to my previous pay.

I had my pay cut 6 years ago and just got back to my previous pay.