Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

But we can make a pretty good guess. And you already did, so your comment here is contradictory. Regardless, you were probably right about 4 out of 5 of the guesses you made. It doesn't really change the message though. So you're basically just trying to distract attention from the article - you've got a trees instead of forest kind of thing going on.

annuities are insurance and are not counted as savings. they do throw a time value on them for net worth calculations though in the census financial study. same thing with life insurance in the net worth study.

the original study posted makes no mention what it looks at to get such a low figure but regardless it is very far apart from the census data

.

Location: East of Seattle since 1992, 615' Elevation, Zone 8b - originally from SF Bay Area

44,585 posts, read 81,206,701 times

Reputation: 57821

Our family was large, born from 1951 to 1968. None of us has retired yet. The oldest is 62 and will probably retire only at maximum social social security time (67) with no pension, no savings. I am next and have a pension plan, 401K and other investments, and home equity of about $300k currently. Of the rest one is in a similar situation to me, another will have a pension but nothing else, and another 4 will be more like the oldest, with just social security. Not that we are "typical" but

it shows that there is a great variety of financial situations among boomers.

This is a heartbreaking story for sure, I often worry about people in small towns so dependent on a single plant, this is the situation in so many places.

With that said $30/hour is well over $60,000 a year. That is way over the median income which is under $40,000 annually. So that means the average SS benefit for those workers will be higher than the figures posted in this thread. And not to sound cold but if you are in your late 50's living in a very low cost of living area such as the deep south and have not saved even 5100,000 for retirement while making $60,000/year well that's kind of on you.

How can an aged widow make it on $1,214 even if she does own her own home and doesn't have debt? And those are average benefits?[/quote]

My mom would feel rich if she got that much every month. So would I! She does own her own home, outright, and her car. That's basically all she has though and she's making it okay. She does get food stamps but they recently cut that down to about $60 mo.. Every time she gets a COLA raise on SS they take more away. At least as much as the "raise". One time they lowered it because her property taxes went down. She manages to pay her car/home insurance, life insurance, property taxes and all her utilities. I pay her rent for her guest house so that helps too. Total for her to live on every month is about $970. She has everything she needs and some things she just wants and she's generous to her church. I help her out monetarily as well, other than rent. She knows if she really needs anything, I'm here.

It seems like most of the statistics are based on the financial situation of those approaching retirement ... yet, ignore an even greater future crisis. I'm speaking of retired folks who, because of significantly reduced returns on traditional 'retirement income vehicles (CD's, T-Bills, etc) -- are now 'eating their principle' in order to maintain a previously expected 4-5% retirement lifestyle.

This scenario produces a downward spiral as reduced savings produce less income than previously required to 'maintain the status quo,' further reducing one's savings. Thus, one quickly winds-up withdrawing more 'income' than they are 'earning' ... further reducing future earning potential.

Those still working say to themselves, "I will probably have to postpone my retirement." But, those already retired have no such option (except to resort to more reverse mortgages or variable annuities.)

In summary, the focus on immediate financial retirement problems, has shifted the emphasis away from the retirement landscape in 10-15 years when those who retired between 2007-2013 began to 'outlive their assets.'

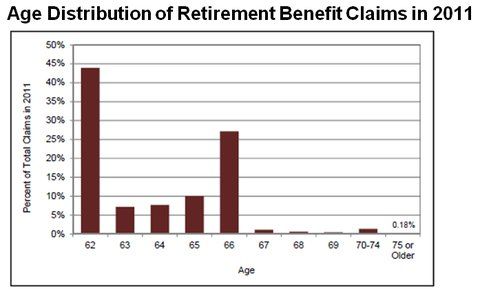

here is age age breakdown for when ss is being taken

That's shocking and explains why I always wondered why the average social security benefit of $1,200 or so was so little when compared to what I expected to receive if I collected at FRA. I have always enjoyed an income that is higher than average but not that much higher.

I am 66 and my estimated benefit is $2,250 if I were to collect now and my wife, who will be 66 in a couple years, would receive 50% of that which would put us at $3,375 for social security benefits alone and we would do just fine without having to ever touch our retirement savings especially seeing how we live in a low cost part of the country. Property tax runs less than $100/month, we are in a state where up to $60k retirement income is totally exempt from income taxes and much of our ss benefits would be exempt from federal taxes as well. After paying our fixed costs consisting of property tax, auto insurance, homeowners insurance, basic utilities and our medicare/supplement costs we would still have over $2,000 for food, clothes and other things we want.

Where we live the estimated median household income in 2011 was $40,151 so with social security alone we are still doing better than that median and we're tax exempt and don't pay payroll taxes to boot.

I've heard how we're all supposed to have $500k set aside for retirement and, this may come as a shock to some of you, but a lot of us don't have that. In the form of a confession I don't have anything near that much saved. I got some but not all of it.

So, not having enough saved my only alternative was to work longer and I am doing that and if I wait to 70 to collect (just four more years) I can make up for the sin of not saving enough. In four years our combined ss benefit will be in excess of $4,000.

Obvious if we both retired at 62 with the reduced benefit we would be in total hurt city. Working that four years boosted our benefit by 33% which is very significant to us. Working another four for a 32% increase is very significant as well.

Quote:

Originally Posted by augiedogie

MathJk: Absolutely correct. 1. Anyone with a bit of common sense knows nobody can count on working full time at a high paying job till 66. Disability, weakness, a closing factory, or just getting forced out of jobs is very common for all kinds of employed folks. The reason so many collect at 62 vs.66 is they need the money.

At 60 I didn't have to worry about not having a job but I did worry about my health so I purchased a disability insurance plan. It was a scarey time.

And what would be the remedy for this situation? Something my WWII Veteran Father and his wife (my mother) taught me as a child. Pay your bills first....don't live beyond your means....save your money and if there is anything left, play with that. Oh, and the "Jones' (neighbors) aren't going to pay your bills for what you don't need". I have lived my life by those ideals. When your working is the best time to save money...obvious. Need what you buy, not just want what you buy. Live responsibly and teach those I phone, texting, twittering, facebooking kids to be responsible and perhaps we won't have rely on the ever disappointing government. How we live in retirement begins and ends with us. If we have to work until we croak...that is the path we chose.

I am sure MathJak would agree that what ever the current requirement state for people is today at age 66 is, it will probably be worse for them at age 85.

Our family was large, born from 1951 to 1968. None of us has retired yet. The oldest is 62 and will probably retire only at maximum social social security time (67) with no pension, no savings...

I'm not sure you have accurate information or you do but just typed it incorrectly. The bolded type in your quote is what leads me to believe that something is not right.

I also was born in 1951 and have been checking into this stuff because I'm nearing retirement. For those born in 1951, age 66 is our Full Retirement Date, meaning that we can earn as much as we want and the Social Security Administration will not deduct $1 from received benefits for every $2 earned in employment wages.

Starting at age 62, which your brother/sister is now, the minimum benefit can be received and that increases somewhere around 5% per year, (on a monthly basis), for every year he/she delays before starting to receive benefits. After age 66, the increase is about 8% per year, up to age 70. Then, there is no more increase in monthly benefits so one might as well start getting benefits because they won't get any more, (except for the yearly cost-of-living raises).

Thank you, Nicet4. The final link near the bottom of your post far exceeds the quality and sophistication of the average news article, as it is a 30-page academic study by a Ph.D.

Indeed, the thought of a widow existing on $1,214 a month is sobering. No room for any luxuries there, not even car ownership in many cases, I would think.

I have trouble believing that number. What happened to survivor benefits? If your spouse dies, you receive spousal benefits on their earnings as well as your own benefits, to the family maximum. She would have had to have no claim of her own, and her husband had to have been bringing home poverty wages his whole life, to have a SS claim that small.

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.