Quote:

Originally Posted by middle-aged mom

Back when Social Security was created, the average life span was about 59 years. If one was lucky enough to live 6 years longer, Social Security would kick in. Using the original logic, no one would now be entitled to Social Security until they were in their 80's.

|

That would all be very fascinating if the was even a kernel of truth in anything you said. You would do well to bow out of any future discussions of Social Security or Medicare, since you do nothing but post disinformation intent upon deceiving and misleading people.

Average life-span is not relevant. In 1935 there were 30 States in the US that had a social security-like retirement program or pension plan. Many States set retirement at age 70, but others at age 65. The Railroad Retirement Act in the early-1930s chose age 65 as well.

Why?

Because actuarial studies showed age 65 to provide a well-managed system. You cannot prove any claim you make. You cannot show through the legislative history of Social Security that life-expectancy from birth was a factor.

Quite the contrary --- as any competent person knows,

the correct and proper metric is life-expectancy from age 65.

To prove you wrong, I submit as evidence Table V.A1.—Principal Demographic Assumptions, Calendar Years 1940-2090, showing that in 1940 there were 9,569 people over age 65 for each 100,000 Americans. As of 2011, there were 4,575 persons age 65 or older per 100,000 Americans.

That's about 50%

less.

Next to prove you wrong, I give you Table V.A3.—Period Life Expectancy which demonstrates two points to debunk your very false claims.

First, the correct and proper metric is life-expectancy age 65 and older, not life-expectancy from birth.

And secondly, everyone can plainly see that in 1940 the life-expectancy over age 65 for a male was 11.9 years, and that in 2011 the life-expectancy was 17.7 years.

For those who don't get it, the metric we are examining is how long does a person live once they reach age 65: so 11.9 years means one lives until age 76.9 years and 17.7 means once lives to age 82.7 years.

What is the difference between 82.7 and 76.9 years?

5.8 years.

There you go. I just destroyed the idiotic "

raise the age" stupidity.

People want to know why I'm vehemently against raising the age, now you know why, because it is not statistically significant, not to mention the fact that you will be negatively impacted. The only thing that will happens is you will force more people into taking early retirement at age 62 with reduced benefits or going on Social Security Disability at an earlier age drawing 100% of their benefits before converting their OADI benefit into the OASI benefit.

The life-expectancy for women at age 65 was 13.4 years in 1940 (a total of 78.4 years) and 20 years in 2011 (a total of 85 years), so the life-expectancy of women has increased by 6.6 years.

By the way you can find that information on Pages 92 and 98 of the 2012 Social Security Report......which apparently very few of you have even bothered to read --- yet you all flap your lips.

Quote:

Originally Posted by middle-aged mom

Back in the early 80's Greenspan recommended substantial hikes in the Social Security tax....

|

Another lie.

The Silent Generation got buried under 520% FICA payroll tax increase --- they survived --- and they made sure Social Security will be available to them.

The Boomers and Tweeners got saddled with a 71% tax increase.

That is hardly "

substantial."

What tax increase has been levied upon Generation X and Y? None.

Quote:

Originally Posted by middle-aged mom

...., creating a necessary surplus....

|

Another lie.

The OASI Trust Fund always had a surplus since 1937.

The Trust Fund was :

1950 $1.9 Billion

1960 $20.3 Billion

1970 $32.5 Billion

1980

$22.8 Billion -- the Trust Fund was losing money 1975 $37 Billion to 1983 $19.7 Billion

1985 $35.8 Billion

1990 $214.2 Billion

2000 $931 Billion

2010 $2.42 TRILLION

Quote:

Originally Posted by middle-aged mom

Social Security taxes are invested in treasuries and create money for the government to spend as they wish. Reagan, Bush 1, Clinton, and Bush 2 spent it all and left IOUs in the box. It's a classic shell game. This is what Obama inherited from the past.

|

Another lie.

How many lies is that now?

OLD-AGE RESERVE ACCOUNT

Section 201. (a) There is hereby created an account in the Treasury of the United States to be known as the Old-Age Reserve Account hereinafter in this title called the Account. There is hereby authorized to be appropriated to the Account for each fiscal year, beginning with the fiscal year ending June 30, 1937, an amount sufficient as an annual premium to provide for the payments required under this title, such amount to be determined on a reserve basis in accordance with accepted actuarial principles, and based upon such tables of mortality as the Secretary of the Treasury shall from time to time adopt, and upon an interest rate of 3 per centum per annum compounded annually. The Secretary of the Treasury shall submit annually to the Bureau of the Budget an estimate of the appropriations to be made to the Account.

Note: This "Account" became the OASI -- Old Age and Survivor's Insurance Trust Fund

(b) It shall be the duty of the Secretary of the Treasury to invest such portion of the amounts credited to the Account as is not, in his judgment, required to meet current withdrawals. Such investment may be made only in interest-bearing obligations of the United States or in obligations guaranteed as to both principal and interest by the United States. For such purpose such obligations may be acquired

(1) on original issue at par, or

(2) by purchase of outstanding obligations at the market price. The purposes for which obligations of the United States may be issued under the Second Liberty Bond Act, as amended, are hereby extended to authorize the issuance at par of special obligations exclusively to the Account. Such special obligations shall bear interest at the rate of 3 per centum per annum. Obligations other than such special obligations may be acquired for the Account only on such terms as to provide an investment yield of not less than 3 per centum per annum.

(c) Any obligations acquired by the Account (except special obligations issued exclusively to the Account) may be sold at the market price, and such special obligations may be redeemed at par plus accrued interest.

(d) The interest on, and the proceeds from the sale or redemption of, any obligations held in the Account shall be credited to and form a part of the Account.

(e) All amounts credited to the Account shall be available for making payments required under this title.

(f) The Secretary of the Treasury shall include in his annual report the actuarial status of the Account.

Social Security Act of 1935

The Second Liberty Bond Act.....mmmhhh....how long ago was that? Oh, yeah 1937 but it was all the fault of the evil Reagan and Greenspan.

Time Machine. Yeah, that's the ticket. Reagan and Greenspan had a Time Machine and they traveled back to 457 BCE and picked up Socrates and then they went forward to 1937 and then they......

Do yourself a favor, go here...

C:\WINDOWS\SYSTEM32\DRIVERS\Host

Use NotePad to open up the Host file, then find this line...

127.0.0.1 localhost

...and then directly underneath it type...

127.0.0.1 badwebsitefilledwithlies.com

...then save the file (or add any other sites you want to permanently block).

Because where ever you're getting your information from, it's all wrong and the only thing you are doing is deluding yourself and deceiving others.

Quote:

Originally Posted by middle-aged mom

40% of government spending goes to Social Security, Medicare and Medicaid.

|

That's another lie.

First, the Trust Funds are separate and apart from the General Fund. Only a propaganda artist would lump them together with the General Fund in order to give a distorted view of the situation.

Second, regarding the Trust Funds, the government merely functions as a pass-through -- monies are collected from employers and employees and then returned to beneficiaries.

In other words, the government isn't spending squat, rather it's collecting money and then handing it back out.

You all drank the Kool-Aid and played the Stupid Game and then now you can't figure out why they're discussing Social Security. You need to be discussing shrimp on treadmills and Jell-O parties and non-essential bureaucracies like the Departments of Agriculture, Education, Labor, Transportation, HUD and others that you don't need.

Still debunking...

Mircea

Quote:

Originally Posted by NewToCA

And if the increased productivity is due to automation, then how does this assist the Social Security Trust Fund in future years?

|

You've just shown how irrelevant the nonsense about productivity really is.

Commending...

Mircea

Quote:

Originally Posted by padcrasher

The sure sign of someone exposed to right wing smears of Social Security is when they start spouting off the classic "worker to retiree ratio" scam. It's a dead give away they don't know what they are talking about.

|

So, according to you, the Social Security Trustees have been "

exposed to right wing smears" and "

they don't know what they are talking about."

Why don't you explain Table IV.B2.—Covered Workers and Beneficiaries, Calendar Years 1945-2090 to everyone?

"The cost rate then rises rapidly between 2017 and 2035, primarily because the number of beneficiaries rises much more rapidly than the number of covered workers as the baby-boom generation retires.

Compared to the 2011 level of 35 beneficiaries per 100 covered workers, the Trustees project that this ratio will rise to 49 by 2035 under the intermediate assumptions because the growth in beneficiaries greatly exceeds the growth in workers.

For each alternative, the curve in figure IV.B2 is strikingly similar to the corresponding cost-rate curve in figure IV.B1. This similarity emphasizes the extent to which the cost rate is determined by the age distribution of the population.

The cost rate is essentially the product of the number of beneficiaries and their average benefit, divided by the product of the number of covered workers and their average taxable earnings. For this reason, the pattern of the annual cost rates is similar to that of the annual ratios of beneficiaries to workers."

[bold and underlined emphasis mine]

Pages 52-54

112th Congress, 2d Session

House Document 112-102

THE 2012 ANNUAL REPORT OF THE BOARD OF TRUSTEES OF THE FEDERAL OLD-AGE AND SURVIVORS

INSURANCE AND FEDERAL DISABILITY INSURANCE TRUST FUNDS

Wow, you are like, really, really detached from Reality™.

I never say anything that isn't backed up by documentation or which I have not personally witnessed or experienced.

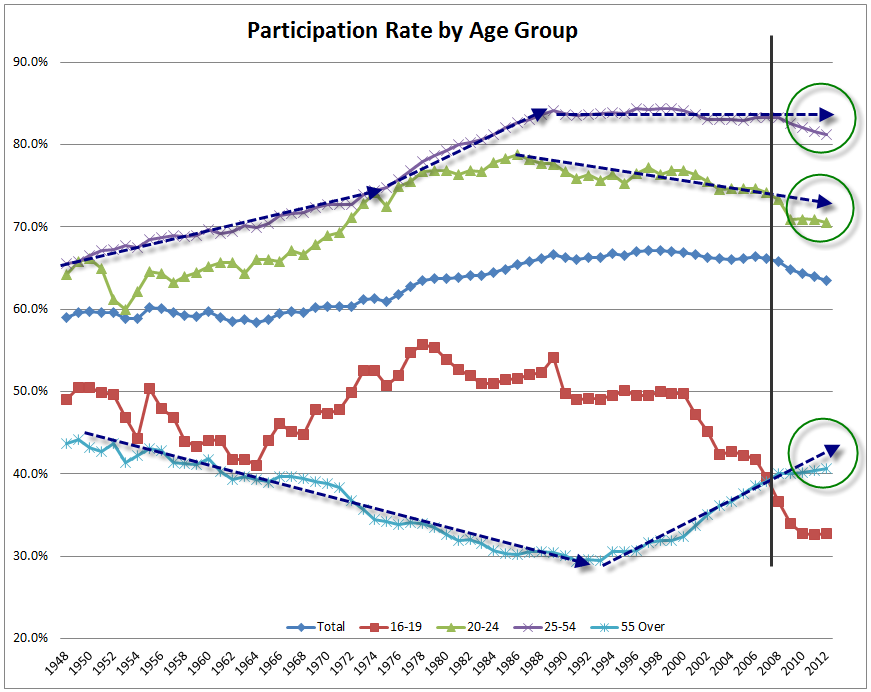

There's a reason why I continually harp on the worker to retiree ratio. Social Security explains it, but I think I explain it a little better, because I break it down into the variable components, which are:

1] the number of workers per retiree -- a function of your Labor Force Participation Rate; and

2] average wages/salaries; and

3] payroll tax levels.

You do not have a sufficient number of workers to fund each retiree, and as if that wasn't bad enough, your wages are stagnant/declining and will continue to decline for the next 50 years, and then you don't have high enough tax levels.

Why do you think FICA/SECA tax rates have increased in the past?

Does everyone understand the relationship?

Benefits per Retiree = Workers (

n) * Wage Rates * Tax Level

See how simple that is?

Average monthly Social Security benefit is $1,239/month or $14,868/year.....so....

$14,868 = Workers (3) * ($30*2,000 hours) * 12.4%

$14,868 = $22,320 so that means you can fund grandma and have money left over for the Trust Fund

$14,868 = Workers (2) * ($27*2,000 hours) * 12.4%

$14,868 = $13,392............Ooops.....you came up short and you'll suck money out of the Trust Fund.

So.....want to tell everyone again about "

the classic 'worker to retiree ratio' scam?"

To resolve the short-fall, there's three things you can do: increase the number of workers, increase the wages or increase the payroll tax.

Increasing the number of workers fails, because to fund Social Security through 2035 at least 12.7 Million workers have to fall out of the sky, uh, like yesterday and start working.

That's not gonna happen. All of you drank the Housing Bubble Kool-Aid, so you don't understand that you've been bleeding jobs since the Clinton Administration and it was the loss of jobs, in combination with lower wages/salaries that led to the economic crisis that busted the Housing Bubble that Paul Krugman said would save your butts.

You're losing jobs because you cannot compete globally and will never be able to compete globally for about 50 more years.

Raising wages isn't gonna happen either. Your wages have been steadily declining or completely stagnant since the Clinton Administration, and that, in combination with a loss of jobs is what led to the crisis that resulted in the Housing Bubble that Krugman said would save your butts.

Wages will continue to stagnate/decline because the US cannot compete globally, and because of your high unemployment rate and a few other factors --- like automation.

National Average Wage Index

1951-1960: 4.09%

1961-1970: 4.45%

1971-1980: 7.31%

1981-1990: 5.34%

1991-2000: 4.35%

2001-2010: 2.64%

Year/Wages per Return/Pct Change

1995 $38,259

..... 0.88%

1996 $38,503

..... 0.64%

1997 $39,600

..... 2.85%

1998 $41,073

..... 3.72%

1999 $42,027

..... 2.32%

2000 $43,066

..... 2.47%

2001 $42,609

..... -1.06%

2002 $41,952

..... -1.54%

2003 $41,718

..... -0.56%

2004 $42,425

..... 1.70%

2005 $42,296

..... -0.31%

2006 $42,206

..... -0.21%

2007 $42,430

..... 0.53%

2008 $41,773

..... -1.55%

Since you will never have enough workers, and wages will not rise, then you have no choice but to raise the FICA tax rate.

Quote:

Originally Posted by padcrasher

You can't see jack coming because you're too lazy to learn the facts. This thread is about Social Security and you're too brainwashed to realize you're parroting those who hope to destroy the program by associating it with medicare's problems.

|

Too lazy to learn the facts?

What would you call someone who is too lazy to read the report?

Quote:

Originally Posted by padcrasher

Another poster too cowardly to use real words. This time they want SS "modified", meaning "cut".

How about lifting the tax cap on high incomes and have workers pay slightly higher pay roll tax rates to keep the program benefits the same?

|

Quote:

Originally Posted by padcrasher

You think your fatalism is some sign of wisdom. In fact, you have no idea what you are talking about. SS has a manageable, long term deficit that could be remedied by lifting the income tax cap, along with a minor increase in the tax cap.

|

Quote:

Originally Posted by gwennie

The age of eligibility doesn't have to be raised. Eliminate the income cap for SS/Medicare taxes and enact legislation so that politicians CANNOT touch taxed dollars that belong to SS/Medicare. Those two things alone will keep those programs more than flush with enough cash. What do you want to do? Raise the retirement eligibility age to 80+ so pretty much nobody can collect their retirement pay?

|

Tax cap stupidity.

For this exercise, we will use....

Individual Income Tax Returns, Preliminary Data, 2010 by Adrian Dungan and Michael Parisi, from

Statistics of Income Bulletin | Winter 2012

Adrian Dungan and Michael Parisi are economists with the Individual Returns Analysis Section. This article was prepared under the direction of Michael Strudler, Chief, Individual Returns Research Section, Internal Revenue Service.

Referring to Page 12

Table 1. Individual Income Tax Returns, Tax Year 2010 Preliminary Data: Selected Income and Tax Items, by Size of Adjusted Gross Income

We are examining

Column 1 Items, specifically lines

#7 Salaries and wages: Number of returns

#8 Amount

For AGI (Adjusted Gross Income) Number of Returns Filed

$100,000 under $200,000 = 2,793,003

$200,000 under $250,000 = 1,401,593

$250,000 or more = 2,435,348

The total number of returns filed for those groups is 16,629,944 returns.

For AGI (Adjusted Gross Income) Salaries and Wages

$100,000 under $200,000 = $1,454,682,235,000

$200,000 under $250,000 = $251,279,279,000

$250,000 or more = $982,361,511,000

The total salaries and wages are $2,688,323,025,000 ($2.688 TRILLION)

Eliminating the cap and taxing 100% of all wages/salaries would yield....

$2,688,323,025,000 * 6.2% = $166,676,027,550 ($166 Billion)

However, a portion of those wages/salaries are already taxed. For simple math, and to give you every possible benefit of doubt, we'll use $100,000 as the "cap." The total amount under the "cap" is....

16,629,944 * $100,000 = $1,662,994,400,000

The amount FICA payroll taxes already collected is...

$1,662,994,400,000 * 6.2% = $103,105,652,800 ($103 Billion)

$166,676,027,550 ($166 Billion)

$103,105,652,800 ($103 Billion) less

-----------------------

$63,570,374,750

So $63.5 Billion is the amount of additional FICA tax revenues raised by eliminating the cap.....

in theory, because....

In particular, the calculation of the necessary tax rate assumes that an increase in payroll taxes results in a small shift of wages and salaries to forms of employee compensation that are not subject to the payroll tax.

...so say the Social Security Trustees (and they are correct).

As you can all see, eliminating the cap will not solve the problem. You will need to raise the FICA tax rate.

I guess I should point out that in November 2012, Social Security paid out $64.98 Billion in benefits.

Does that add a little perspective?

Who wants to continue drinking the Wage Cap Kool-Aid?

Understand that I am not in any way advocating any position -- increase/not increase wage cap --- I'm just saying that eliminating the wage cap will not solve the problem alone.

You live in Bergen, NJ and earn $150,000/year. You're offered a job in Covington, Kentucky that pays $105,500/year. Should you take the job?

Why wouldn't you?

"It's a pay cut." Wrong answer. $105,500 (KY) = $150,000 (NJ).

You live in Manhattan, New York earning $150,000/year and you're offered a job in Harrison, Ohio for $60,265....should you take it?

Again, why wouldn't you?

"It's a pay cut." Wrong freaking answer. $60,265 (OH) = $150,000 (NYC).

It's called the cost-of-living. Seriously, I'm still shocked that people don't get it.

I have to attribute it to Liberal propaganda and disinformation. The person in Ohio earning $60K and the one in Manhattan earning $150K both have the exact same life-style: they drive the exact same car; have the exact same auto insurance company; wear the exact same name-brand clothes; eat at the same restaurants; they each squirrel away $100/month in savings; they each have the exact same credit cards; go on holiday to the same places; stay at the same hotels....there is no difference whatsoever in their lives, except that one lives in a place where it costs more.

But $150,000 is hardly rich, and eliminating the wage cap will have a net negative affect. It will reduce income by $2,411 or about $201/month and it would affect 12+ Million filers.

Note that will be $28.9 Billion in annually that will be removed from the economy, resulting in loss of potential sales tax revenues for cities/States. And then, too, employers will have to cough up $28.9 Billion.

The point is there is no such thing as an easy fix for Social Security. You will have to raise taxes, no doubt about it, and it will cost your economy in terms of jobs, which will exacerbate the problems you already have.

You already means test Social Security beneficiaries. Single filers who earn more than $25,000 and married couples with more than $32,000 and separate filers earning more than $0 (no I didn't stutter) put 85% of their income subject to the tax --- which goes straight to the Social Security and HI Trust Funds, not to the General Fund.

You all need to get it together, and soon. The longer you wait, the worse off you'll be.

Expediently...

Mircea

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

") If today's 40 somethings are successful with their bitching and moaning, and the retirement age is raised to 70 or more, the 40 somethings of the future will curse them and beg for the retirement age to be lowered.

If today's 40 somethings are successful with their bitching and moaning, and the retirement age is raised to 70 or more, the 40 somethings of the future will curse them and beg for the retirement age to be lowered.