Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Only if you believe in the invisible pink unicorn of socialism.

There are less than two taxpayers per recipient. When that drops to less than one taxpayer per recipient, how "safe" will it be?

Socialist InSecurity https://www.usdebtclock.org/

US Population : 332.4 million

US Income Taxpayers : 124.8 million

US Retired : 56.1 million

Medicare : 62.7 million

Medicaid : 83.7 million

Food stamp recipients : 40.8 million

Only if you believe in the invisible pink unicorn of socialism.

There are less than two taxpayers per recipient. When that drops to less than one taxpayer per recipient, how "safe" will it be?

Socialist InSecurity https://www.usdebtclock.org/

US Population : 332.4 million

US Income Taxpayers : 124.8 million

US Retired : 56.1 million

Medicare : 62.7 million

Medicaid : 83.7 million

Food stamp recipients : 40.8 million

Only if you believe in the invisible pink unicorn of socialism.[/qute

There are less than two taxpayers per recipient. When that drops to less than one taxpayer per recipient, how "safe" will it be?

Socialist InSecurity https://www.usdebtclock.org/

US Population : 332.4 million

US Income Taxpayers : 124.8 million

US Retired : 56.1 million

Medicare : 62.7 million

Medicaid : 83.7 million

Food stamp recipients : 40.8 million

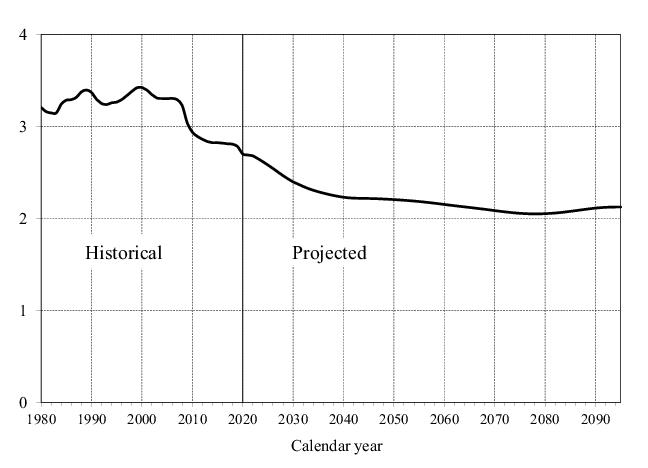

Nope. Social security is a wage tax, so you go by workforce not where ever you came up with that 124.8 million income tax payers nonsense. Someone who works might not pay any income tax (and many don't), but they will have payroll taxes taken from their check. Since you're selectively quoting from social security, here is the rest: "An estimated 176 million workers will work in OASDI-covered employment in 2021." ... "There are currently 2.7 covered workers per each Social Security beneficiary. By 2035, there will be 2.3 covered workers for each beneficiary"

Furthermore the baby boomer generation that strongly impacted the ratio or workers to retirees will be winding down, most projections show the declining worker/beneficiary ratio slowing down around 2035, which is why both GAO and SSA believe the 78(ish)% percent payable benefits will be sustainable at least to terminal on 75 year projections.

Workers per beneficiary

Barring one of your many doomsday scenarios finally coming true nobody reading these posts will see a drop to less than one worker per recipient, in fact it's possible they won't see less than 2 in their lifetime either.

The older I get, the more cynical I get. I tend to trust my "gut feeling" based on previous experience or a "common sense" built with years of been there/ done that.

For example, when I see on YouTube an investment "guru" promoting a company that plans to use genomic sequencing to identify your potential illness and promise you a greater health and longevity. A little bell in my head ranged and asked "haven't we been here before?". Sure enough, 20 years ago a similar company was marketed based on the same approach but ended up nowhere. Now a year later, this company's stock is again in the tank. Trust your gut feeling.

One common theme I've found on many of these financial books/ articles assume the INVESTOR ARE IDIOTS. They much prefer you keep put money into the account (dollar cost averaging) and let some money manager buy/sell stocks and decide what to do with your money. So you often hear the phrase "... stocks rise reliably in the long run..." Another word; don't worry about the ups & downs of the market, just keep putting money into your account.

Truth to be told, many people, including retirees don't know much about investing. They don't want to learn neither. Mentally they are much more comfortable to hand over the money to a stranger and betting he/she will make money for them.

Unfortunately for the majority of us, we were trained to be an employees. We went to school to learn a skills (accounting, engineering, law, medicine, etc.) and we spent the rest of our life time practicing that trade, to earn money for living and savings. 30-40 years later, we raised a family and looking at the sunset years of our life. Now we worry how to keep our savings, maybe grow it a bit, for our retirement years.

What one thing schools didn't teach us was on how to create wealth. Instead we traded our productive time with money (often in the form of $/hour). I often wonder what if I learned on how to create wealth in my younger years, rather than focusing all my effort to be the best engineer I could, how my life would've turned out differently.

I don't have a solution to offer you.

[/END OF RANT]

I was not trained to be an employee, but to be a certain type of skilled professional. I was self-employed for the major part of my career. I worked because I valued work more than I valued "creating wealth", and a good income was an adequate reward for my work. I stopped working because the work was very stressful, and I had worked for quite a long time, so nothing obliged me to work longer.

As everyone knows, I don't have a majorly favorable opinion about investing, but I do have Roth in a growth fund, sort of out of curiosity. I do not support myself with investment. If the stocks take a major beating this year, I think it would be a good time for Roth conversions (I don't have anything left to convert, since I did it all during the most recent crash in March 2020, and it worked out fabulously) - that is my only contribution to the discussion.

Quite unnecessary. Don’t recall asking for a solution - from you or any other. This economist has a perspective that I found worth sharing. Read it if you like, ignore if you don’t. I don’t care one way or the other…

I see endless threads on the safe withdrawal rates without a lot of content. So, thought this might be of interest to someone.

It's of interest to me. I was a broke person most of my life, lived without savings, know nothing about investing, but with a pension and FINALLY no debt except for my mortgage, I have some spare money. After some people here pointed me to a few sites where I could learn the basics, I've started reading things most investors learned at 25.

No scenario on any of those sites fits my situation. I know I am willing to take a little more risk than is normal for people who are counting on their investments to survive. So, thanks.

The older I get, the more cynical I get. I tend to trust my "gut feeling" based on previous experience or a "common sense" built with years of been there/ done that.

For example, when I see on YouTube an investment "guru" promoting a company that plans to use genomic sequencing to identify your potential illness and promise you a greater health and longevity. A little bell in my head ranged and asked "haven't we been here before?". Sure enough, 20 years ago a similar company was marketed based on the same approach but ended up nowhere. Now a year later, this company's stock is again in the tank. Trust your gut feeling.

One common theme I've found on many of these financial books/ articles assume the INVESTOR ARE IDIOTS. They much prefer you keep put money into the account (dollar cost averaging) and let some money manager buy/sell stocks and decide what to do with your money. So you often hear the phrase "... stocks rise reliably in the long run..." Another word; don't worry about the ups & downs of the market, just keep putting money into your account.

Truth to be told, many people, including retirees don't know much about investing. They don't want to learn neither. Mentally they are much more comfortable to hand over the money to a stranger and betting he/she will make money for them.

Unfortunately for the majority of us, we were trained to be an employees. We went to school to learn a skills (accounting, engineering, law, medicine, etc.) and we spent the rest of our life time practicing that trade, to earn money for living and savings. 30-40 years later, we raised a family and looking at the sunset years of our life. Now we worry how to keep our savings, maybe grow it a bit, for our retirement years.

What one thing schools didn't teach us was on how to create wealth. Instead we traded our productive time with money (often in the form of $/hour). I often wonder what if I learned on how to create wealth in my younger years, rather than focusing all my effort to be the best engineer I could, how my life would've turned out differently.

I don't have a solution to offer you.

[/END OF RANT]

We appear to have solved it by paying off assets - the home we live in and 2 that we rent out, and the cars and everything else. It created cash flow that serves our needs, and THAT freed up investment money.

If the stock market crashed tomorrow it would not effect our cash flow one bit; if things continue along we will be fine.

Never as no one cares about your money like you do ….I would never let anyone make my money decisions..there are enough do it yourself portfolios out there for anyone to do it .

The only time I recommend a third party to handle your money is when you are prone to poor investor behavior mentally

I think he means if he has some memory or cognitive issues and is not able to manage his money, I have the same fear.

It's of interest to me. I was a broke person most of my life, lived without savings, know nothing about investing, but with a pension and FINALLY no debt except for my mortgage, I have some spare money. After some people here pointed me to a few sites where I could learn the basics, I've started reading things most investors learned at 25.

No scenario on any of those sites fits my situation. I know I am willing to take a little more risk than is normal for people who are counting on their investments to survive. So, thanks.

Thank you! Indeed - one has to consume good quality information from a variety of credible sources to build a perspective. The perspective lets you make better decisions that are applicable to your situation. Just as it is good to diversity the investments, it is also good to diversify the sources you get the information on. I think Kotlikoff is a high quality source whose perspective might or might not be applicable or best for you.

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.