Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

What has broken the chain in the real estate market is that the lenders--or the schlubs they sold their loans to--have begun to figure out that an awful lot of those borrowers are going to be unable to repay what they have borrowed.

How long will such a downward spiral go? More properly, the question should be: How long should it go? The answer is long enough that the speculative excesses are wrung out of the market, and real estate once again is priced realistically to what buyers actually can afford and money borrowed to finance such purchases can actually expect to be repaid out of the borrower's cash flow.

I sincerely never understood how this could have come about. Huge, "reputable" companies like Countrywide, which I'm sure employ a legion of PhDs surely should/could have seen this coming. They knew they were loaning money that couldn't/wouldn't be repaid. They knew that with the borrows' inability to repay would come a company implosion (like what Countrywide experienced). I just don't understand how they let this happen.

Second comment. Yes, that makes perfect sense. There is a natural ratio or relationship between median home price and median income. Colorado (maybe $300k? and $45K?) is a heck of lot closer to the relationship than SoCal (maybe $550K? and $55K?). Ultimately, the price of a loan a person can take out is around 28% to 35% of his gross. Median incomes in the middle five figures allow $200K-$250ish loans, not $400K - $500K loans.

(I apologize if I am re-posting the same graphic...I forgot, but it really is a great graphic.)

Something I've thought of, the frequent references to "housing recovery." Recover from what? A several-year, abnormal, aberrant, low-interest feeding frenzy. It's not going to be a return to that. Maybe a stabilization more in line with the rest of the economy, but not a "return" or a "recovery."

Great point. I view "recovery" as meaning a return to stable pre-bubble market conditions, where prices could be expected to appreciate at a rate close to the rate of inflation. The historic average is around a half percent above little i. Recovery means you can buy a house without worrying about being upside down to the tune of tens or hundreds of thousands of dollars after a year or two.

Housing as an investment is a relatively new, and fundamentally flawed idea. Americans do not build houses to be true long-term appreciating assets. After 15 years, the roofs and floors of wood-frame houses need replaced, plumbing starts to clog and corrode, termites and other creatures get in, etc. The idea that a 15-year old house should be worth even close to the same as a new house of the same size evades me. It's a fallacy propagated by the same marketers that tell you buying is always better than renting, and that you're a schmück if you don't send two months of your hard-earned pay to DeBeers and Co. in South Africa for a diamond to prove you really love her...

I sincerely never understood how this could have come about. Huge, "reputable" companies like Countrywide, which I'm sure employ a legion of PhDs surely should/could have seen this coming. They knew they were loaning money that couldn't/wouldn't be repaid. They knew that with the borrows' inability to repay would come a company implosion (like what Countrywide experienced). I just don't understand how they let this happen.

Second comment. Yes, that makes perfect sense. There is a natural ratio or relationship between median home price and median income. Colorado (maybe $300k? and $45K?) is a heck of lot closer to the relationship than SoCal (maybe $550K? and $55K?). Ultimately, the price of a loan a person can take out is around 28% to 35% of his gross. Median incomes in the middle five figures allow $200K-$250ish loans, not $400K - $500K loans.

(I apologize if I am re-posting the same graphic...I forgot, but it really is a great graphic.)

House price index (relative dollars in time)

One thing your graphic also illustrates is a little more elusive. Much of that speculative bubble in California is what created the "temporary" bulge in equity that many Californians tapped to buy property in Colorado--which, of course, helped fuel the bubble in Colorado and other Rocky Mountain states. Now, as that California bubble deflates, that source of "mad money" for Californians to plunk down in Colorado is also evaporating. I don't think that shockwave has really started to hit the Colorado markets just yet, but when it does, I think it will be a quite profound "downer" on the markets--and not just on the low-end stuff. It will become more of an equal-opportunity ****-storm then.

I sincerely never understood how this could have come about. Huge, "reputable" companies like Countrywide, which I'm sure employ a legion of PhDs surely should/could have seen this coming. They knew they were loaning money that couldn't/wouldn't be repaid. They knew that with the borrows' inability to repay would come a company implosion (like what Countrywide experienced). I just don't understand how they let this happen.

that's why bubbles are also called "manias," because in them normally sane and rational people do things that are crazy...one side (the home owner) is motivated by fear of not getting a home and missing out on making some quick bucks (greed) and the other side (the lender) is motivated entirely by greed...fear and greed motivated psychology is what drives manias, plus the herd instinct of humans. that's why it's so hard to sell at the top, your greed instinct is telling you to hold out for just one more dollar, your fear instinct is telling you to sell, but your herd instinct is comforting you because you're in the company of a lot of smart people doing the same thing as you.

Quote:

There is a natural ratio or relationship between median home price and median income. Colorado (maybe $300k? and $45K?) is a heck of lot closer to the relationship than SoCal (maybe $550K? and $55K?). Ultimately, the price of a loan a person can take out is around 28% to 35% of his gross. Median incomes in the middle five figures allow $200K-$250ish loans, not $400K - $500K loans.

according to the numbers:

CO

income: $45K

house price: $300K

interest rate (3yr/30yr ARM teaser): 1%

monthly house payment (P+I): $965

% of gross income: 26%

interest rate (adjustment): 8%

monthly house payment (P+I): $2201

% of gross income: 59%

CA

income: $55K

house price: $550K

interest rate (3yr/30yr ARM teaser): 1%

monthly house payment (P+I): $1769

% of gross income: 39%

interest rate (adjustment): 8%

monthly house payment (P+I): $4036

% of gross income: 88%

looking at these numbers, it is clearly insane to a sane person that these folks will/can not make the new payments after ARM readjustment (and why lenders call em "exploding ARM's"), but in manias and its associated greed/fear driven hysteria allows home buyers to rationalize almost anything to the point where it makes perfect sense.

One thing your graphic also illustrates is a little more elusive. Much of that speculative bubble in California is what created the "temporary" bulge in equity that many Californians tapped to buy property in Colorado--which, of course, helped fuel the bubble in Colorado and other Rocky Mountain states. Now, as that California bubble deflates, that source of "mad money" for Californians to plunk down in Colorado is also evaporating. I don't think that shockwave has really started to hit the Colorado markets just yet, but when it does, I think it will be a quite profound "downer" on the markets--and not just on the low-end stuff. It will become more of an equal-opportunity ****-storm then.

another thing is that many californian's who sold out in the last few years have been heading back to oklahoma to retire. i'm hoping that oklahoma avoids the bubble the CA and CO have experienced. i expect folks would sell the second vacation home before selling their primary residence, but who knows, may be they're retiring in CO in a few years. if so, then that might mitigate the crash somewhat...

another thing is that many californian's who sold out in the last few years have been heading back to oklahoma to retire. i'm hoping that oklahoma avoids the bubble the CA and CO have experienced....

FWIW: The former wife of a pal in FL sold their former home in NJ and moved to OK. Home prices and property taxes in OK are 1/3 of those in northern NJ. What we can take away from such anecdotal stories is evidence that boomers are fleeing pricey coastal areas by going to the heartland. This reverse migration has potential to re-invigorate areas that have for years seen poor growth or decline as young ones headed to the cities. We left DC for COL SPGS in 2005, on the front end of the boomer retirement tsunami.

Quote:

Originally Posted by Pettrix

....2008 is a wash. 2009 will probably have residual left-overs from 2008 but it will not be until 2010 that it finally stabilizes. With 2%-6% increase in values being seen in 2011. Unfortunately, if the values fell 20-30% from 2005 thru 2010, it will take at least 5 years to come back to the 2005 values, making it 2015.

Quote:

Originally Posted by Bob from down south

Maybe, but I still think your recovery timeline is a bit on the early side. The majority of the RE timelines I've seen don't factor in the exacerbating effects of what is shaping up to be a prolonged and deep economic recession...or worse....

The research of Harry S. Dent ( H.S. Dent Foundation -- click on VIDEO ) is that boomer spending begins a long decline @2011, with nothing to replace it until "echo boom" generation spending cranks up @2023. His research seems sound and worth listening to. Dent's view of a long recession or depression match well with those of Denver stock market technical analyst Vitaliy Katsenelson.

Katsenelson (author of Active Value Investing) says that in 2000 we entered a long period where the DJIA will trade in a narrow range between upper & lower boundaries, i.e., a long Range-Bound (RB) market. His research goes back 100 years. Long lasting RB periods in the 20th century were 1906-24 (18 years); 1937-50 (13 years); 1966-82 (16 years). In his opinion, buy & hold investing is out, that people must actively buy & sell stocks based on P/E ratio's to make money in RB markets.

When I compare the timelines of Dent (Geo-Political cycles lasting 34-36 years each) and Katsenelson (RB markets occuring with regularity) the cycles line up quite well....and put any sort of housing recovery well into the future.

Last edited by Mike from back east; 02-07-2008 at 01:59 PM..

Add to all of it the strong likelihood of petroleum shortages and permanent price run-ups from "peak oil," and you have the ingredients for a real mess.

I ran across this letter from South Africa, dated 2/4/08 on Kunstler's web site. It illustrates pretty well how quickly things could unravel:

Common theme? Energy. Oil. Sprawl. Roads. Auto-dependency.

An ex-Marine friend of mine made this analogy about our lack of motivation to address our sprawl/energy/economic mess. "If you're walking through a sniper-infested jungle and you wait to hear a gun go off before taking action, you're already dead."

Are you referring to Harry Dent, the author who predicted a dow of 40,000 in one of his books? If so, I personally have little faith in his predictions. I'd rather spend my money on an astrologer. At least I'd get some entertainment value for my money.

Jazzlover wrote:

"If you're walking through a sniper-infested jungle and you wait to hear a gun go off before taking action, you're already dead.""If you're walking through a sniper-infested jungle and you wait to hear a gun go off before taking action, you're already dead."

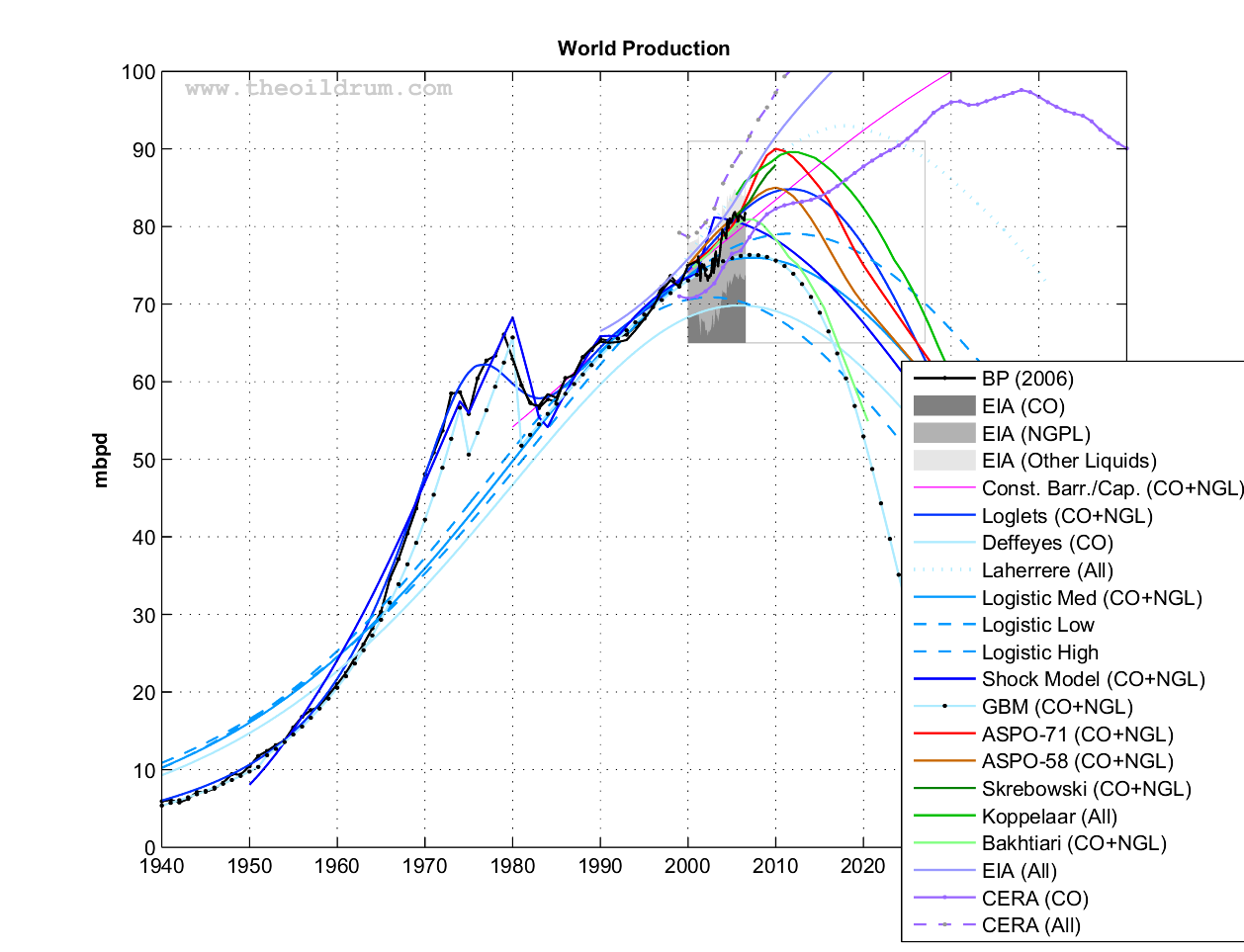

which "peak(s)" are you referring to? forecasting a peak in any thing is part science and mostly art, but it's especially daunting when predicting oil reserves that have not been found yet. one man's shortage is another man's surplus! the eia oil report out next week should prove enlightening...

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

forecasting a peak in any thing is part science and mostly art, but it's especially daunting when predicting oil reserves that have not been found yet. one man's shortage is another man's surplus!

forecasting a peak in any thing is part science and mostly art, but it's especially daunting when predicting oil reserves that have not been found yet. one man's shortage is another man's surplus!