Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Renters with enough cash for a down payment will continue to have that money in the bank earning .2% interest. Based on the summary of JohnG72 of his friend purchasing a bit over 2 years ago and losing 20%, not including closing costs, taxes, misc. home owner expenses and upgrades, the individual who maintained a rental actually earned a pretax annual income of about 10.2% interest on that money in the bank by not losing anything on a primary home INVESTMENT.

For those who wish to note the renter did not get the deductions on their taxes one would have to know what the last dollar of taxable income was for the individual. In today's world most folks in Nevada will only get between 15% and 25% of their mortgage interest/property tax payment back in Federal tax savings as there is no state tax savings. There is no way this will offset the losses as noted in JohnG72's analysis of his friend. Worse yet, this individual may have lost his entire life savings in one fell swoop as his entire down payment was wiped out.

Errr, it's highly unlikely he lost his entire life savings in one fell swoop because he didn't put anything down. The opportunity costs incurred by JohnG72's friend are actually quite low. As well, it doesn't make sense to focus on the opportunity costs he incurred as a buyer without looking at the additional out of pocket expenses he's incurred as a renter. On balance, I don't see him any appreciably worse off than if he had rented.

Lastly, when doing the rent vs. buy comparison there are factors that can be difficult to monetize, but they no doubt hold value. Things like, fixed payments vs. potential rent increases, the ability to personalize your living space, the knowledge that you won't have to relocate at the end of a lease, etc. People are willing to pay for those things.

Perhaps the Market is showing it wants to be in cash too. Ben's little fix is not holding well with economists. Certainly did not this week. Even with QE 3 or is it 9 by now...... There may be a short up swing in the economy but that will almost certainly cause a crash once that money is absorbed.

Cash will continue to be king. Q: How long can America keep artificial low interest rates?? A: It does not matter. We are at incredibly low interest rates now and banks are not risking a long term loan... Period. Folks are no longer driven by low interest rates as they are not working, cannot qualify or have been burnt by previous real estate purchases collapsing on them. A few folks are benefiting but certainly not the majority. This is not the last 5 decades. This is something our generations have not seen before and the world is collapsing under the economic weight. This is not Gloom and Doom this is about keeping folks afloat in this mess. Stay solvent unless you can really afford otherwise. Invest wisely but be very, very aware.

Funny but the answer is really quite simple. If the Government feels a WPA type situation is warranted then no more Government jobs. No more prevailing wage and stop catering to the unions. If the average Government employee is making over 120 thousand a year that is equivalent to 3 non union, Welfare or unemployed, being put to work and making over 40 thousand a year. that's 3 jobs for every one presently or newly created by the Government. Get rid of the ridiculous salaries plus perks the unions have forced down their throats or gave themselves in government. Sorry, but in my opinion things will get much worse before they get better at least until the so called economists run out of cards up their sleeves. Don't believe me?? go look up what your city employees are making with perks and retirement. In my city the city manager is making over 250,000 per year before perks and the rest of the bums are not paid that much less. And we are a small city.

Any debt which cannot be fully afforded should be delayed. Running cash positive is the way to survive in this economy. Purchasing a primary residence when the write off for the individual is not above the 15 - 25% deduction level is just silly. Folks in the higher income brackets need to be wary as well. Stay well below your budget and affordability factors and do not worry about a ridiculously low rate of return in the bank. Debt is the enemy for individuals as well as this government. These government guys selling short term investments and purchasing tons of low interest long term debt is going to create havoc like we have not seen even today. China slowing down and Europe in turmoil. The middle east... well we do not know where that is going but it does not look great. At the very least it is uncertain.

Sorry Tony, you and I have agreed on most things in the past but not this time. ROI is key not the so called peace of mind in owning a primary residence unless the buyer's sum total of debt payments, including taxes, insurance, car payments, credit card debt, maintenance on all assets, Utilities or any and all other monthly payouts are well under the individual's reasonable budget levels with plenty of cash in the bank to weather a strong storm. Getting rid of debt, not incurring more debt, is the key to staying alive in this crap for the below average, average and even above average wage earners.

As I keep noting, low end investment real estate is a great place to be as long as money is coming in and not going out. One must not own a depreciating asset in my opinion unless it is earning enough revenue to outlast and out perform the alternative in this economy.

Getting a good lease when renting a home for those with good credit may allow the renter to negotiate a better lease I know it works for me on my rentals and I have not had any turn over in at least 2.5 years. I still am getting great rent but I look hard at those with great credit and do give them a break. Rent until you get into the price range I have noted.... It may be coming sooner than you think.

Perhaps the Market is showing it wants to be in cash too. Ben's little fix is not holding well with economists. Certainly did not this week. Even with QE 3 or is it 9 by now...... There may be a short up swing in the economy but that will almost certainly cause a crash once that money is absorbed.

Cash will continue to be king. Q: How long can America keep artificial low interest rates?? A: It does not matter. We are at incredibly low interest rates now and banks are not risking a long term loan... Period. Folks are no longer driven by low interest rates as they are not working, cannot qualify or have been burnt by previous real estate purchases collapsing on them. A few folks are benefiting but certainly not the majority. This is not the last 5 decades. This is something our generations have not seen before and the world is collapsing under the economic weight. This is not Gloom and Doom this is about keeping folks afloat in this mess. Stay solvent unless you can really afford otherwise. Invest wisely but be very, very aware.

Funny but the answer is really quite simple. If the Government feels a WPA type situation is warranted then no more Government jobs. No more prevailing wage and stop catering to the unions. If the average Government employee is making over 120 thousand a year that is equivalent to 3 non union, Welfare or unemployed, being put to work and making over 40 thousand a year. that's 3 jobs for every one presently or newly created by the Government. Get rid of the ridiculous salaries plus perks the unions have forced down their throats or gave themselves in government. Sorry, but in my opinion things will get much worse before they get better at least until the so called economists run out of cards up their sleeves. Don't believe me?? go look up what your city employees are making with perks and retirement. In my city the city manager is making over 250,000 per year before perks and the rest of the bums are not paid that much less. And we are a small city.

Any debt which cannot be fully afforded should be delayed. Running cash positive is the way to survive in this economy. Purchasing a primary residence when the write off for the individual is not above the 15 - 25% deduction level is just silly. Folks in the higher income brackets need to be wary as well. Stay well below your budget and affordability factors and do not worry about a ridiculously low rate of return in the bank. Debt is the enemy for individuals as well as this government. These government guys selling short term investments and purchasing tons of low interest long term debt is going to create havoc like we have not seen even today. China slowing down and Europe in turmoil. The middle east... well we do not know where that is going but it does not look great. At the very least it is uncertain.

Sorry Tony, you and I have agreed on most things in the past but not this time. ROI is key not the so called peace of mind in owning a primary residence unless the buyer's sum total of debt payments, including taxes, insurance, car payments, credit card debt, maintenance on all assets, Utilities or any and all other monthly payouts are well under the individual's reasonable budget levels with plenty of cash in the bank to weather a strong storm. Getting rid of debt, not incurring more debt, is the key to staying alive in this crap for the below average, average and even above average wage earners.

As I keep noting, low end investment real estate is a great place to be as long as money is coming in and not going out. One must not own a depreciating asset in my opinion unless it is earning enough revenue to outlast and out perform the alternative in this economy.

Getting a good lease when renting a home for those with good credit may allow the renter to negotiate a better lease I know it works for me on my rentals and I have not had any turn over in at least 2.5 years. I still am getting great rent but I look hard at those with great credit and do give them a break. Rent until you get into the price range I have noted.... It may be coming sooner than you think.

You make a valid point regarding risk, but let me remind you that you don't get hurt on a rollercoaster until you jump off.

Sure you can.....it may not be an immediate death that would occur with the fall, it's just a slow, torturous agonizing pain as your head bounces back and forth and you feel like you want to puke......that's how the housing market makes me feel at least. I'm ready for the ride to stop.

I agree with FOD about the lower tier properties. I'll also add that older properties (20+) are languishing on the MLS. I see 80's homes listed for 200-300 days that are not getting any action. I may start concentrating on these as they are for the most part in older established neighborhoods free from the dreaded stalin-esque HOA. My target price is $50 per sq/ft, still a ways to go but getting closer every day, perhaps by the end of the year...

Sorry Tony, you and I have agreed on most things in the past but not this time. ROI is key not the so called peace of mind in owning a primary residence unless the buyer's sum total of debt payments, including taxes, insurance, car payments, credit card debt, maintenance on all assets, Utilities or any and all other monthly payouts are well under the individual's reasonable budget levels with plenty of cash in the bank to weather a strong storm. Getting rid of debt, not incurring more debt, is the key to staying alive in this crap for the below average, average and even above average wage earners.

Reasonable minds can disagree. That said, no one's been able to demonstrate to me yet how JohnG72's friend is appreciably worse off having bought vs. rented.

And it appears we disagree on another point - I'm certainly not a believer in taking on debt just for debt's sake, but at current interest rates I wouldn't put a single dollar down more than I had to on a property. With 30 year fixed mortgages at 4% I'd finance every last dollar that I could. YMMV.

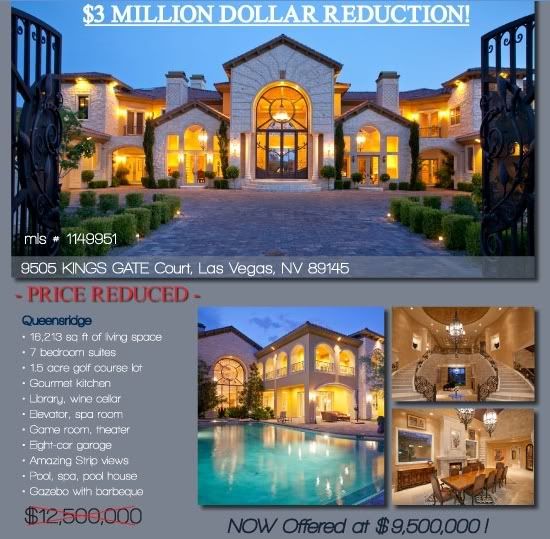

This house sold for $2,000,000 on 1/18/2011. The current value is $1,800,000. I have no idea what kind of crack this guy is smoking if he thinks his house went up 5 times in value during the last 9 months.

This house sold for $2,000,000 on 1/18/2011. The current value is $1,800,000. I have no idea what kind of crack this guy is smoking if he thinks his house went up 5 times in value during the last 9 months.

The lot alone sold for 2M in 2004 and it appears they established a trust in Jan 2011. Those numbers reflect the lot only.

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.