Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

It is, I think, not uncommon to reach a phase of life, where one hasn't exactly retired, or has not retired entirely, but has essentially ceased contributing further to one's accounts. This happens to fast-starters who later slow down, or perhaps persons who sustained some impasse in their careers and thus found themselves in positions where income balances outlays, but capacity for additional savings is limited. Thus, it is incorrect to say, that there are only two phases of investment-life: accumulation and drawdown. There is a third phase, which I'll call stasis, where there is neither accumulation nor drawdown.

Likewise, when one has reached a large ratio of portfolio to annual salary, additional savings - even if entirely possible - no longer have much impact. One severe day's market-gyrations may overwhelm a year's worth of assiduous savings.

The question then becomes, what ought one to do, to maximize the portfolio's growth, while also attending to one's psyche? Perusing the various "portfolio charts", and comparing the 60/40 with the Permanent Portfolio and its ilk, I find that the main difference between the two, is scatter of outcomes. In particular, for those using the 4% drawdown rule, the 60/40 evinces quite the broad range of outcomes over 40 years, while the PP is much narrower. The PP also has the advantage, that if the aim is the portfolio's perpetual health, then in the initial years, the safe drawdown rate is still OK, while for the 60/40, the only safe drawdown rate for the first few years is zero (yes, zero!).

So, for people who aim to live off their portfolio, staring today, the PP makes eminent sense. For those who don't intend to touch it for a decade (or longer), it's hard to conceive of improvements to a portfolio with aggressive stock-allocation. That is of course as far as actual portfolio performance is concerned. Tending to one's psyche is rather an another matter.

yes , there can be a difference between the accumulation and decumulatio stages . the accumulation stage is about growing assets , i am a big believer in going 100% equities in that stage .

the decumulation stage stage stage can be about both preserving assets but still growing assets .

don't forget many retirees never enter the decumlation stage because they have pensions that they live on and in effect the pay check never did stop so the portfolio's are there as just an extra source of fun or extra money . no reason they can't be 70-100% equities . many retirees are investing for legacy money and are not investing to create a constant flow of income , the same applies to them , they can go very high in equity allocation with no ramifications if things don't go well ..

i always liken it to betting against the house . if you lose money and you have enough money you can keep doubling up and eventually win or be even , the odds say so . .

so houses usually install a house limit so you reach a point where you can no longer double up and win back your money .

as we get older , age and health is our house limit . if you have a long time before that money means anything , you effectively have no house limit

eventually we may have to wait so long for recovery that we either find we are to old to enjoy the extra spending power , not healthy enough to enjoy it ,need to cut back our lifestyle either mentally or because we have to or we just die . i know in 2008-2009 we certainly did less spending because mentally we just could not do the spending we did before things plunged and we still had pay checks coming in . but mentally we just could not do that same level of spending . retirement would be worse of a feeling .

so as i age i find my style of investing evolves with age and also balance . which is why i find buy and die totally passive investing from the womb to the tomb not appealing to me at all because life changes as we go on , priorities change and needs change , shouldn't our investment objectives change along the way at various stages ?

the last few years has added hundreds of thousands of dollars in gains and we want to preserve most of that growth at this stage of the late bull .

once the next part of the cycle comes our balances are not what we all see if your portfolio is only weighted for prosperity and you are riding the cycle . . our balances will spend the next 80% of the time somewhere between that next low and the next high so what we see ain't what this bull really gave us .

it is like looking at our balances before we paid all our bills ..it is like our bull market balances have a mortgage due only we don't know what we owe when we ride the cycle . .

while up to pre retirement i was 100% equities i entered retirement with a range of 40-50% equities weighted just for prosperity and low rates . .

my wife will be 68 in a few days and i will be 66 so once again the style is shifting again as 2/3 of the money is now bullet proofed including all those lovely gains while 1/3 has actually gotten more aggressive and is now in the insight growth model .

the whole mix still falls out in the 40-45% equity range but the assets that counted only on low rates , which were the assorted bond funds were now re-allocated . they had little lifting power and potentially those bond funds could even fall since those funds held lots of non treasury stuff which can act like stocks in a down blast .

plus where is the high inflation protection if like retirees saw in 1965 we go from 2% inflation to double digits in a few short years and are blind sided ? that buy and die portfolio actually failed for retirees in both 1965 and 1966 if you retired then .

so those are now very powerful downside performers , being diversified instead in to long term treasuries , gold and most important a cash allocation which does a dual roll . it forms a barbell with the long term treasuries so it brings duration down to the intermediate term range , but it also acts as a stock option to buy stocks at lower prices with no expiration date .

so it really is the other assets that were re-allocated and not so much the equities allocation . that is still in the 40% range

the core portfolio can never be devastated yet overall the portfolio still is weighted for prosperity .there are now asset classes that perform very powerfully covering all 4 major economic outcomes .

instead of trying to rule out depressions , recessions ,high inflation or longer lasting black swans the plan allows for them and actually plans for them .

you can actually make a dynamic plan where for every year the bull continues from here rebalance more and more of the growth portfolio in to the bullet proof one preserving more and more , like a sliding limit order protects your gains .

there is no limit to the flexibility because the ratio between the permanent portfolio and the variable portfolio is whatever one decides they want .

again , this is only food for thought and i am not advocating others to do it if they are happy with their plan .

but just be aware that conventional portfolio's are only geared for prosperity and low rates for the most part .

there are really 4 major outcomes if you are a buy and die investor .

prosperity

recession

depression

high inflation

Last edited by mathjak107; 07-29-2018 at 03:35 AM..

It is, I think, not uncommon to reach a phase of life, where one hasn't exactly retired, or has not retired entirely, but has essentially ceased contributing further to one's accounts. This happens to fast-starters who later slow down, or perhaps persons who sustained some impasse in their careers and thus found themselves in positions where income balances outlays, but capacity for additional savings is limited. Thus, it is incorrect to say, that there are only two phases of investment-life: accumulation and drawdown. There is a third phase, which I'll call stasis, where there is neither accumulation nor drawdown.

Likewise, when one has reached a large ratio of portfolio to annual salary, additional savings - even if entirely possible - no longer have much impact. One severe day's market-gyrations may overwhelm a year's worth of assiduous savings.

The question then becomes, what ought one to do, to maximize the portfolio's growth, while also attending to one's psyche? Perusing the various "portfolio charts", and comparing the 60/40 with the Permanent Portfolio and its ilk, I find that the main difference between the two, is scatter of outcomes. In particular, for those using the 4% drawdown rule, the 60/40 evinces quite the broad range of outcomes over 40 years, while the PP is much narrower. The PP also has the advantage, that if the aim is the portfolio's perpetual health, then in the initial years, the safe drawdown rate is still OK, while for the 60/40, the only safe drawdown rate for the first few years is zero (yes, zero!).

So, for people who aim to live off their portfolio, staring today, the PP makes eminent sense. For those who don't intend to touch it for a decade (or longer), it's hard to conceive of improvements to a portfolio with aggressive stock-allocation. That is of course as far as actual portfolio performance is concerned. Tending to one's psyche is rather an another matter.

the biggest problem i saw in the permanent portfolio concept was i never saw the logic in putting equal dollars in to outcomes that were anything but equal . the prosperity cycle is usually the longest .

using the butterfly or using a variable portfolio that you combine with the pp can weight things for prosperity ,unless you are a doom and gloomer and want to go heavier on the the gloomy side investments .

the ratio between the two is up to you . if 30% of the money is near and dear to you than save 70% for the variable model and go with your instincts .

because the dips are not nearly as steep the gains do not have to be as great so about 40% equities has been found optimum as a total over all mix .

once you go to high in equities you just seem to deepen the drops but add little to the upside returns because then you undo the pulling power of the pp..

that is why since 1970 a traditional buy and die 60/40 under performed the 40% equity butterfly concept as well as why the pp with 25% equities and its pulling power beat my 60/40 since 2007 despite a historical bull market going up 300% from the lows . results are always very different when both sides of a cycle are included.

Last edited by mathjak107; 07-29-2018 at 05:04 AM..

Ohio and Mathjak, I think your recent posts make some very valuable points about changing allocations as we age. I am thinking more and more about allocations since I have a great deal of concern about Trump. Also we will eventually reach some sort of crisis or the end of this rather strange business cycle.

There seems to be one point missing in this discussion. For me a major concern is taxes. I have had lots of capital gains growth over the past 9 years. I should have done some churning of accounts but I didn't. I will be hit with some major taxes, including substantial Medicare deductions, if I reallocate. I am not sure how to accomplish any allocation changes except gradually.

actually that is another point about buy and die investing , specially with index funds in taxable accounts .

you can end up with decades of pent up taxes that can be a huge tax torpedo . so many things are linked to retirement income as well as higher capital gains rates and surcharges that making changes can be hard . just the increases in medicare premiums can wipe out tax savings .

luckily i paid taxes on our actively managed funds all along so we made a lot of changes in 2007 and completed them . had i indexed we would have had to carry the changes over in to 2008 . that would have killed us coming from 100% equities like we did .

i kind of just kept the s&p index fund i had for quite a few years which really had no purpose other than the gains were so high the taxes would have hurt , so i just kept it as the equity holding for the pp so i could utilize it then built the portfolio around it .

so the total portfolio was completed on friday .

i now have 2/3's of the money in the pp , with :

25% in voo- s&p 500 fund

25% in gld- gold

25% in TLT- long term treasury bonds

25% IN fdlxx (treasury money market ) my money market went belly up in 2008 and we were locked out as well as lost money so i want only treasury bills in this money market since the portfolio is bullet-proofed .

the other 1/3 is invested in the 100% equity fidelity insight growth model .

it consists of all market segments plus foreign holdings . the exact holdings i am not allowed to post .

total allocation over all is 43% equities . the pp now has the ability to grow in any scenario for the most part . sure the variable portion in the insight growth model will take a hit but at least we know 2/3's of all our money can never really be devastated , not by recessions , depressions or should high inflation strike ..

Last edited by mathjak107; 07-29-2018 at 07:07 AM..

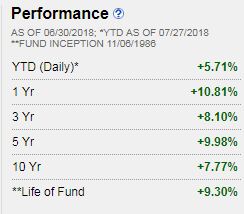

8.50% for 1 year return . not bad with 20% in each of cash , long term bonds and gold and 40% in equities . .

i would have to calculate year to date,

but keep in mind fbalx in the last recession fell 32% . so the deal ain't done until the cycle is complete . the permanent portfolio was up 3% in 2008 . the butterfly would have been down a bit .

sure you do better in a bull on the way up , but weighted only for prosperity and low rates other outcomes can cream you .

Last edited by mathjak107; 07-29-2018 at 07:33 AM..

And history tells us the most common scenario has been prosperity..by a landslide.....investing is a probabilities game.

Exactly , this is why you weight for prosperity . The equities portion does not change much ,you keep forgetting that. All you are doing is taking what you typically keep not in equities and reallocating it. 40% equities with those other asset classes have been found to be optimum but no reason you can’t weight higher.

It just negates some of the downside protection and going up to 60% has made things worse not better. To much damage ends up being done in the down cycle so over the long term it has hurt not helped performance . Once you get above 70-100% equities you. have no need for the protection , all you need is time

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.