What got into people's heads to make them think that rent is "throwing money away"? (inspection, renters)

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

This thread reminds me of threads about investing in stocks during the winter of 2008-2009. People would post saying that they were selling all their stocks and putting the proceeds into a savings account. However buying high and selling low is not a quick road to financial success.

Is this the bottom of the housing market? Maybe, maybe not. I sure don't know. Is renting more financially advantageous than buying for everyone? I haven't a clue. I think it depends on a lot of variables that are probably different for every one of us.

Personally I would not buy a house in any market if I did not intend to live in that location for at least 7 years, but that's just a rule I have for myself, to avoid excess hassles in life. I do prefer to own whether it is more expensive in the long run or not - - - money is to buy the things that I want, and I want my own house. I'm pretty sure that a lot of people differ with me and they are right, for them, but not for me. I am so happy to be living in a home that I own.

You know, while I agree on the opportunity cost factor, I would love to see stats on how many renters actually put down payment equivalent money to work, rather than pee it away on tschotkes and other disposables.

If 50% of renters are renting with the philosophy that they will be better off working their capital, and prospering, I would be surprised.

Again, I agree with the academic materiality of opportunity costs. I just wonder how many apply it.

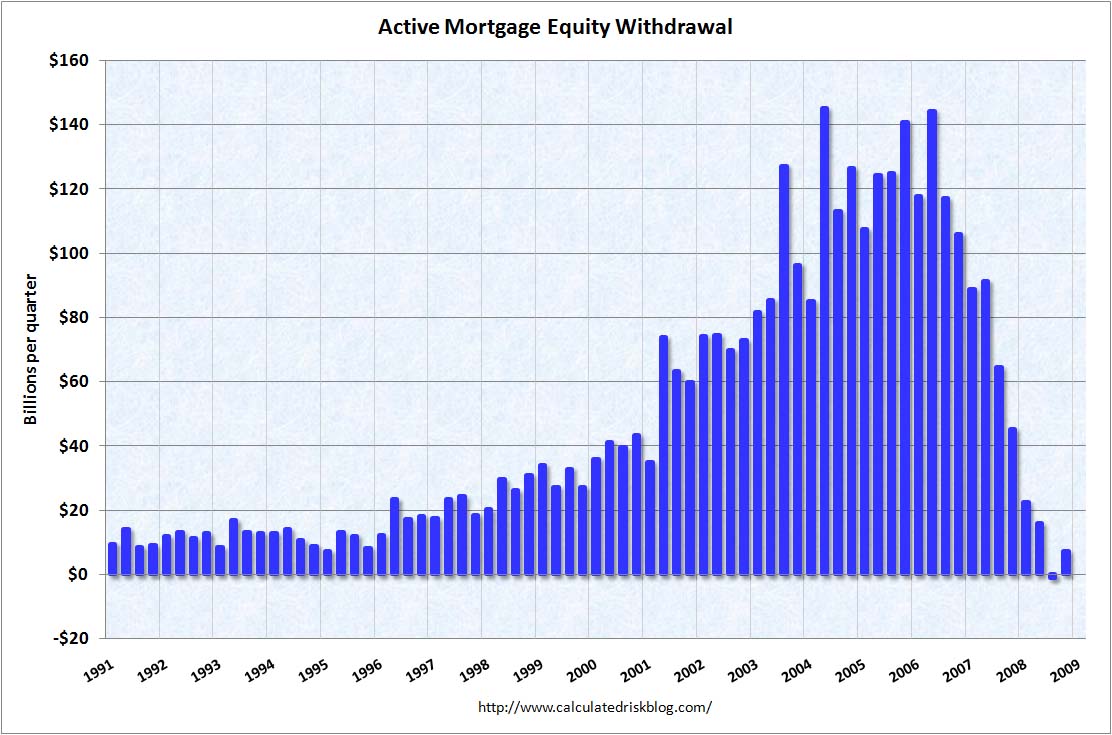

We should also look for stats on the number of buyers who take out HELOCs or HELs and spend the money. As an example, from Calculated Risk: MEW, Consumption and Personal Saving Rate. Note that this is net withdrawal, basically equity extraction minus principal payments :

Looks like the idea of building equity a benefit of ownership doesn't really happen in practice either, at least over the past few decades. Granted the debt load has gone down a bit over the past few years as people default on loans and credit cards, but that's hardly a point in favor of buying.

It's not like buying a house automatically makes you responsible. And from the responses in this thread. you're dealing with buyers who think that buying a depreciating asset on margin is better than "throwing money away on rent" so the question of applying the theory hits both sides equally hard.

We should also look for stats on the number of buyers who take out HELOCs or HELs and spend the money. As an example, from Calculated Risk: MEW, Consumption and Personal Saving Rate. Note that this is net withdrawal, basically equity extraction minus principal payments :

Looks like the idea of building equity a benefit of ownership doesn't really happen in practice either, at least over the past few decades. Granted the debt load has gone down a bit over the past few years as people default on loans and credit cards, but that's hardly a point in favor of buying.

It's not like buying a house automatically makes you responsible. And from the responses in this thread. you're dealing with buyers who think that buying a depreciating asset on margin is better than "throwing money away on rent" so the question of applying the theory hits both sides equally hard.

How is irresponsible buying and ownership by an unknown number of homeowners applicable to renting to avoid opportunity costs? (PLEASE don't tell me that 28% of homeowners are under water... )

And it hardly relates to the question I raised, which was:

What percentage of renters choose to rent to utilize capital "wisely?"

I recognize that is a rhetorical question which cannot be reasonably addressed, other than anecdotally. But I thought it worth pondering, in light of the common crowing about "opportunity costs" in ownership.

I'm not pushing buying or renting. I'm also not attacking either approach.

Personally I would not buy a house in any market if I did not intend to live in that location for at least 7 years, but that's just a rule I have for myself, to avoid excess hassles in life. I do prefer to own whether it is more expensive in the long run or not - - - money is to buy the things that I want, and I want my own house. I'm pretty sure that a lot of people differ with me and they are right, for them, but not for me. I am so happy to be living in a home that I own.

You do realize that the reason there are so many people almost venemously posting against ownership...a great deal of backlash, really..... is because of the recent past overwhelming societal and cultural pressure that pushed home ownership, correct?

Many people tend to take the wrong view when it comes to rent vs buy. The first assumption many make is that you will be renting an identical or nearly identical property. Not necessarily the case, but let's say it is.

Assume that you are renting a property for $1,700 a month, on a year to year lease.

Given the math, let's assume that, at today's rates, that same house will cost you $400 a month less if you put down 20%. This is roughly the same spread as a house I recently compared against a very equivalent rental property.

Two things that are primary financial benefits of the home ownership equation.

1) Tax advantages

2) Hedge against inflation.

I know how to calculate reserves for maintenance/replacement items such as furnace/ac/roof and the rest will be, adjusted with an estimate for increased property taxes. We've seen a fairly sudden, but consistent rise in rental rates, primarily due to rising property taxes and rising demand.

You're in a much better position locking in housing costs rather than risking uncertainty, if your plan is to be in an area for awhile.

I didn't mention equity, because in reality, you have a long-term mortgage pay-down that becomes essentially, a bank. Some people choose to pay down the principal with the savings from the rental difference. Buying a house should be a longer term decision, which is why people get confused in short-term markets like this one.

I bought a house in mid-2006 which has just appraised for 5% more than I paid for it. Obviously, not a great return, and not even a profit given the interest used for the finance. However, the monthly outlays are still $400 a month less than renting one in this market.

Think of it as a long term hedge, not an investment decision. It will take years of re-education to get people away from the stale thinking that realtors and tax advisors have been giving out for decades.

How is irresponsible buying and ownership by an unknown number of homeowners applicable to renting to avoid opportunity costs?

You were talking about the connection between theory and practice breaking down on the rental side. I was just showing that it happens on the buying side, too. With actual data, instead of unanswerable off-topic rhetorical questions even.

Many people tend to take the wrong view when it comes to rent vs buy. The first assumption many make is that you will be renting an identical or nearly identical property. Not necessarily the case, but let's say it is.

Assume that you are renting a property for $1,700 a month, on a year to year lease.

Given the math, let's assume that, at today's rates, that same house will cost you $400 a month less if you put down 20%. This is roughly the same spread as a house I recently compared against a very equivalent rental property.

Two things that are primary financial benefits of the home ownership equation.

1) Tax advantages

2) Hedge against inflation.

I know how to calculate reserves for maintenance/replacement items such as furnace/ac/roof and the rest will be, adjusted with an estimate for increased property taxes. We've seen a fairly sudden, but consistent rise in rental rates, primarily due to rising property taxes and rising demand.

You're in a much better position locking in housing costs rather than risking uncertainty, if your plan is to be in an area for awhile.

I didn't mention equity, because in reality, you have a long-term mortgage pay-down that becomes essentially, a bank. Some people choose to pay down the principal with the savings from the rental difference. Buying a house should be a longer term decision, which is why people get confused in short-term markets like this one.

I bought a house in mid-2006 which has just appraised for 5% more than I paid for it. Obviously, not a great return, and not even a profit given the interest used for the finance. However, the monthly outlays are still $400 a month less than renting one in this market.

Think of it as a long term hedge, not an investment decision. It will take years of re-education to get people away from the stale thinking that realtors and tax advisors have been giving out for decades.

Nice assumptions. I only wish I could find a rent vs own ratio even remotely close to that in my area. I guarantee the premium for any semi-decent SFR in my area is tilted the opposite of your example above, and decidedly so.

Nice assumptions. I only wish I could find a rent vs own ratio even remotely close to that in my area. I guarantee the premium for any semi-decent SFR in my area is tilted the opposite of your example above, and decidedly so.

So, in your area (which is?..), monthly rent payment is lower then mortgage payment+taxes would be?

in any area...

monthly rent payments are not based on mortgages or any other LL costs

I don't think that was the point. It appeared to me the question was more along the lines "If a person wanted to rent or buy and looked at similar properties does the rental or the purchase have the lower monthly price tag in your area?"

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

)

)