Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

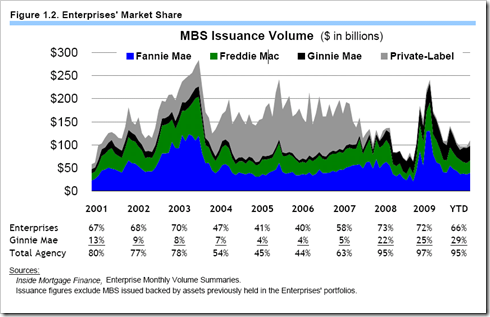

What this tells us is that during the peak years of the housing bubble, Fannie and Freddie were largely off the scene. Everything else — every complicated calculation coming out of AEI or wherever — is an attempt to obscure this simple fact.

Not exactly new, we knew this back in 2003 when Bush started to push congress to make changes.

Not sure if someone else, posted this before but its worth reminding the liberals of their mistake.

This new study examines CRA lending and not the complete financial meltdown.

From the study.

Taken together, we find evidence for elevated lending by banks in the treatment group

around the CRA exam during the 2004–2006 period. Moreover, there is concurrent evidence that

the performance of loans originated by the treatment group banks around the CRA exam are in

particular worse than those originated by the control group banks during the 2004–2006 period. This is also the period when private securitization boomed and might therefore reflect an

unexplored channel through which this market induced risky lending in the economy.

They didn't even study the affect of the private securitization which "boomed" during the study period. During this boom period the GSE were no longer the majority players in morgage market.

They did however acknowledge the change in behavior.

Our analysis here is motivated by the fact that securitization – the act of originating

loans and selling them to investors – changed dramatically during our sample period. In

particular, the private securitization market – in which loans from lenders are packaged and sold

to private investors – heated up especially between 2004 and 2006 (Keys et al. 2012). In contrast,

the period 2007–2009 saw a drastic contraction of private securitization market but a concurrent

expansion in the government-sponsored enterprise (GSE) securitization market – in which loans

from lenders are packaged and sold to GSEs in adherence with GSE underwriting standards. We

conjecture that banks are more likely to originate loans to risky borrowers around CRA

examinations when they have an avenue to securitize and pass these loans to private investors

after the exam. There are at least two reasons why banks may be less likely to originate risky

loans under the CRA when GSE securitization is the primary avenue for loan sales. First, GSEs

have stricter underwriting guidelines than private investors for lenders (Keys et al. 2012).

Second, GSEs tend to face more scrutiny from regulators and market participants given their

large role in the mortgage market (e.g., in the aftermath of the crisis). Thus, we expect banks that

are subject to CRA examination to originate more risky loans in times of examinations especially

during the 2004–2006 period.

Risker loans during the period that private securitization had become the dominate players.

Then the complete quote from the conclusion of the study.

We find that adherence to the act leads to riskier lending by banks: in the six quarters surrounding the CRA exams, lending is elevated on average by about 5 percent and these loans default about 15 percent more often. These patterns are accentuated in CRA-eligible census tracts and are concentrated among large banks. The effects are strongest during the time period when the market for private securitization was booming.

The reforms being pushed during the Bush Administration was for increased participation of the private securtization players and limiting the role of the GSEs.

OP - Those are Democratic policies. There are no such things as "Democrat" policies or anything else.

As far as the banking is concerned the bankers took ever larger risks with the assurance that they and their stockholders would never suffer losses. That makes taking risk easy.

What this tells us is that during the peak years of the housing bubble, Fannie and Freddie were largely off the scene. Everything else — every complicated calculation coming out of AEI or wherever — is an attempt to obscure this simple fact.

Not at all true. Your chart shows who issued the mortgages, not at all calculating who had guaranteed them.

This new study examines CRA lending and not the complete financial meltdown.

From the study.

Taken together, we find evidence for elevated lending by banks in the treatment group

around the CRA exam during the 2004–2006 period. Moreover, there is concurrent evidence that

the performance of loans originated by the treatment group banks around the CRA exam are in

particular worse than those originated by the control group banks during the 2004–2006 period. This is also the period when private securitization boomed and might therefore reflect an

unexplored channel through which this market induced risky lending in the economy.

They didn't even study the affect of the private securitization which "boomed" during the study period. During this boom period the GSE were no longer the majority players in morgage market.

They did however acknowledge the change in behavior.

Our analysis here is motivated by the fact that securitization – the act of originating

loans and selling them to investors – changed dramatically during our sample period. In

particular, the private securitization market – in which loans from lenders are packaged and sold

to private investors – heated up especially between 2004 and 2006 (Keys et al. 2012). In contrast,

the period 2007–2009 saw a drastic contraction of private securitization market but a concurrent

expansion in the government-sponsored enterprise (GSE) securitization market – in which loans

from lenders are packaged and sold to GSEs in adherence with GSE underwriting standards. We

conjecture that banks are more likely to originate loans to risky borrowers around CRA

examinations when they have an avenue to securitize and pass these loans to private investors

after the exam. There are at least two reasons why banks may be less likely to originate risky

loans under the CRA when GSE securitization is the primary avenue for loan sales. First, GSEs

have stricter underwriting guidelines than private investors for lenders (Keys et al. 2012).

Second, GSEs tend to face more scrutiny from regulators and market participants given their

large role in the mortgage market (e.g., in the aftermath of the crisis). Thus, we expect banks that

are subject to CRA examination to originate more risky loans in times of examinations especially

during the 2004–2006 period.

Risker loans during the period that private securitization had become the dominate players.

Then the complete quote from the conclusion of the study.

We find that adherence to the act leads to riskier lending by banks: in the six quarters surrounding the CRA exams, lending is elevated on average by about 5 percent and these loans default about 15 percent more often. These patterns are accentuated in CRA-eligible census tracts and are concentrated among large banks. The effects are strongest during the time period when the market for private securitization was booming.

The reforms being pushed during the Bush Administration was for increased participation of the private securtization players and limiting the role of the GSEs.

All a matter of record.....and they missed the mark.

Let's assume you operate a business and make a lot of money. Being a conservative investor, you limit your risks to investment grade, AAA.

Most of you capital is tied up in your investments and now those investments go south.

The issue with FNMA/FHLMC is not that they guaranteed mortgages that met their standards. The real issue is that they invested their own capital in investment grade bonds that turned out to be anything but investment grade.

They along with most other conservative investors, pension plans, mutual funds, global banks, insurance companies and so on did not perform their own due dilly and instead relied on the AAA rating of paper issued by the likes of Bear Stearns and Lehman Bros.

Riggghhht....The Bush wars and completely obsequious obediance to bankers had nothing to do with it...

Complex cause fallacy....

This was a tag team effort. The Dems were only too happy to submit to phony, short term populist platform like minorities enjoying the privalages of debt fueled boom bust cycles and the Repubs were only too happy to allow banksers to exploit the situation.

Please register to post and access all features of our very popular forum. It is free and quick. Over $68,000 in prizes has already been given out to active posters on our forum. Additional giveaways are planned.

Detailed information about all U.S. cities, counties, and zip codes on our site: City-data.com.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.

Please register to participate in our discussions with 2 million other members - it's free and quick! Some forums can only be seen by registered members. After you create your account, you'll be able to customize options and access all our 15,000 new posts/day with fewer ads.